Why Warren Buffett Never Bought Bitcoin: Fundamental Value of Cryptocurrency

spawns

Overview

Legendary value investor Warren Buffett has been outspoken about his distaste for Bitcoin. Telling investors nearly a decade ago that he does not believe it is a “store of value” or a “reliable medium of exchange,” he has made it clear that it does not even meet the definition of a currency. This year he referred to it as a “gambling token” unworthy of serious fundamental investors.

Nevertheless, time has proven the value of these digital currencies. Although highly volatile, Bitcoin and Ethereum have maintained threshold values while continuing to function as a medium of exchange. At this point, it’s fair to argue that Buffett may not be entirely right about these instruments.

While I agree with Buffett that Bitcoin and digital currencies in general cannot be viewed through a traditional value lens, I think it’s clear at this point that they have some level of fundamental value if we’re going to consider them currencies.

I want to note that it is important for us to consider cryptocurrencies specifically as currencies. They are definitely not like owning stocks; Owning cryptocurrencies does not represent a fractional claim on a company’s cash flows like owning stocks does.

Rather, cryptocurrencies should be assessed on the basis of their value as currency: the extent to which they provide, and are used for, the exchange of value. Since we have readily available calculations for this, we can work to establish a basic valuation methodology for cryptocurrencies.

This article will outline these metrics and compare Bitcoin and Ethereum on this basis.

Basic currency for cryptocurrencies

A currency’s value is established from the set of transactions it supports. In macroeconomics, there is an established theory around this. The more “demand” (total transactions) for a currency, the higher its value. At constant levels of currency supply, more transaction volume implies a higher value for a given currency. A second-order demand effect would be countries holding certain currencies in reserve so that they can trade in those currencies in the future.

The value of fiat currencies is then derived from both the size of a country’s economy as well as the international transaction volume of its respective currency. The sum of national and international transaction volume constitutes the total demand for a given currency. A good example of this in the real world would be the large global levels of dollar-denominated debt as well as dollar-denominated energy trade; these are well understood to represent fundamental foundations for the dollar’s uniquely high value.

That being said, we can establish a basic supply and demand value, along with a relative valuation, for Bitcoin and Ethereum.

The demand here is the level of transactions that occur “on the chain”, as in the direct use of the blockchain network for similar exchanges. This calculation does not take into account the secondary market demand for these two cryptocurrencies, namely crypto-to-fiat conversions. While these secondary market forces are undoubtedly a material price driver, this goes beyond the scope of functioning as a currency per se and will not play into our fundamental analysis this time.

The supply here is of course the actual amount of cryptocurrency outstanding.

|

Date |

BTC volume |

ETH volume |

|

4/11/23 |

.385 M |

1,085 m |

|

4/12/23 |

.338 M |

1,022 m |

|

13.04.23 |

.332 M |

1,095 m |

|

14.04.23 |

.316 M |

1,166 m |

|

15.04.23 |

.276 M |

1,056 m |

|

16.04.23 |

.232 M |

.854 M |

|

17.4.23 |

.316 M |

1,012 m |

|

18.4.23 |

.313 M |

1,070 m |

|

19.4.23 |

.302 M |

1,085 m |

|

20.4.23 |

.297 M |

1,074 m |

|

21.4.23 |

.352 M |

1,010 m |

|

22.4.23 |

.355 M |

.862 M |

|

23.4.23 |

.433 M |

.868 M |

|

24/4/23 |

.360M |

.941 M |

|

25.4.23 |

.370M |

.976 M |

|

26.4.23 |

.436 M |

.978 M |

|

27.4.23 |

.419 M |

.939 M |

|

28.4.23 |

.484 M |

.988 M |

|

29.4.23 |

.486 M |

.887 M |

|

30.4.23 |

.569 M |

.975M |

|

5/1/23 |

.682 M |

1,102 m |

|

5/2/23 |

.458 M |

1,128 m |

|

5/3/23 |

.490 M |

1,117 m |

|

5/4/23 |

.491 M |

1,110 m |

|

5/5/23 |

.411 M |

1,209 m |

|

5/6/23 |

.601 M |

1,146 m |

|

5/7/23 |

.608 M |

1,101 m |

|

5/8/23 |

.575M |

1,146 m |

|

5/9/23 |

.598 M |

1,127 m |

|

5/10/23 |

.672 M |

1,086 m |

|

5/11/23 |

.547 M |

1,100 m |

Source: Excel, YCharts

|

BTC price |

$26,808 |

|

ETH price |

$1,808.39 |

|

BTC average daily volume (30 days) |

.450 M |

|

BTC average daily volume in $ |

$12.07 B |

|

ETH average daily volume (30 days) |

1,077 m |

|

ETH average daily volume in $ |

$1.95 B |

Source: Excel, YCharts

We can see that over the past 30 days, the Bitcoin network has processed 6.2 times the number of transactions that the Ethereum network has on a dollar basis.

|

BTC circulating supply |

19,370 M |

|

ETH circulating supply |

121,340 M |

Source: Excel, YCharts

We can now divide the average transaction volume (in dollars) by the total supply to arrive at a “total transaction value per unit” calculation:

|

Transaction value per supply unit BTC |

$622.91 |

|

Transaction value per supply unit ETH |

$16.05 |

Source: Excel, YCharts

This paints a strong picture. On a pure supply/demand basis for the last month, Bitcoin is currently 38.8 times more valuable than Ethereum – even though its price is only 14.82 times that of Ethereum.

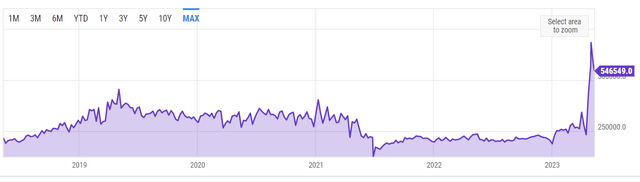

However, we need to contextualize this further. Worth noting is that there has been a very significant increase in Bitcoin network volume over the past month; it is currently far outside historical norms. It seems that this wave is about to subside, but it is uncertain which way it will go. Furthermore, the average network activity for Bitcoin appears to have settled below historical norms during 2022 and the first 2 months of 2023. This long-term, structural trend may well continue as the short-term upswing subsides.

YCharts

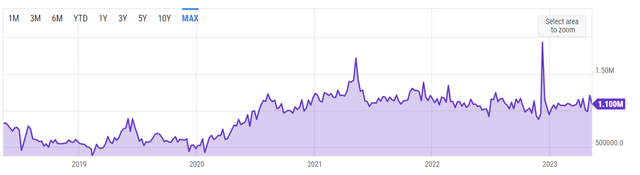

As for Ethereum, the recent trendline also saw volatility, but delayed by 3 months. The structural trend here appears to be the opposite of Bitcoin; Ethereum utilization has fluctuated at a higher level than previously.

YCharts

While the data is strong on a 30-day trailing basis, a review of the longer-term technical picture here indicates that Bitcoin’s network leverage trend is too short-term and high-variance to constitute a reliable buy signal.

The other thing to consider is the significant multiples that each of these cryptocurrencies trade at relative to the amount of daily transaction volume they support.

However, for a monthly utilization level, prices appear to be more anchored to market prices:

| Monthly transaction volume per supply unit BTC | $18,687.41 |

| Monthly transaction volume per supply unit ETH | $481.61 |

As such, I would venture that this is the metric that is best used now and going forward.

On this measure, BTC also appears to be relatively cheap:

| BTC price / monthly transaction volume per unit | 1,435 |

| ETH price / monthly transaction volume per unit | 3,755 |

Conclusion

While we have established a reasonable way to relatively value these two cryptocurrencies, the current fluctuations in Bitcoin’s network utilization are too variable to make the numbers reliable for an investment decision. If Bitcoin’s massive surge in usage proves to be consistent for another 3 months, I’d feel comfortable calling it a buy on a relative basis.

Alternatively, if the BTC trend normalizes and Ethereum’s structural trend continues to accelerate towards higher leverage, I would call Ethereum a buy.

For the time being, I would be cautious and consider Bitcoin a hold while network utilization levels off to something more in line with historical norms.