Time to invest in the growth of FinTech?

Defined as new technology that seeks to improve and automate the delivery and use of financial services, the financial technology (fintech) market is estimated to be valued at around $700 billion by 2030 with a compound annual growth rate (CAGR) of over 20%.

Currently valued at over $200 billion, it would be no surprise if the fintech market becomes a trillion-dollar industry in the distant future as innovation continues among financial services. This makes many high-tech stocks exciting investments, especially for long-term investors.

PayPal’s revolution

As a brief overview, fintech companies strive to simplify and digitize banking, payment processing, peer-to-peer lending and payments, financial software and other financial services.

PayPal (PYPL) is a good example of such digitization and how fintech companies make financial services much more convenient for consumers. Landing a Zacks Rank #3 (Hold) there may still be better buying opportunities ahead, but last year’s selloff in PayPal stock has made the financial payments innovator more attractive from a valuation standpoint.

Formerly owned by eBay (EBAY) before its spinoff in 2015, the growth of electronic e-commerce payments is some attributed to PayPal. As the internal catalyst for eBay’s online payments growth, Amazon (AMZN) and others followed.

Despite giving back some of the gains since its 2015 IPO, PayPal stock is still up +94%. This has trailed the Nasdaq but is close to the S&P 500’s performance and outperformed its former parent eBay.

Image source: Zacks Investment Research

PayPal has become one of the largest providers of online payment solutions and is responsible for making the process much easier for consumers during the early days of eBay and the rise of the internet. Prior to this, the frequent use of mailed checks to pay for items purchased on the Internet became time-insensitive, outdated and incompatible with online purchases.

Although there is increasing competition, PayPal’s growth story is far from over. Based on Zacks Estimates, PayPal’s earnings are forecast to jump 18% in FY23 and rise another 16% in FY24 to $5.69 per share.

Image source: Zacks Investment Research

More impressively, fiscal 2024 will represent a stunning 132% EPS growth since the pandemic with 2019 earnings of $2.45 per share. PayPal’s top line expansion also supports its earnings potential with sales projected to increase 6% this year and jump another 9% in FY24 to $31.85 billion.

Trading at $72 a share and 14.5X forward earnings, Wall Street’s concerns about a high premium being paid for PayPal stock have faded. Even better, PayPal now offers a 45% discount to the industry average of 41.1X forward earnings and trades well below the S&P 500’s 18.8X.

Image source: Zacks Investment Research

Assuaging premium fears of recent years, PayPal now trades 83% below its decade-long high of 87.8X and at a 67% discount to the median of 43.7X.

PayPal’s ability to confirm its expected annual growth in its upcoming first quarter report on May 8 will be the key to more upside in PYPL stock. That said, holding on to shares at current levels seems like an eager way to get in on fintech expansion.

Visa & Mastercard’s transformation

Worth considering for exposure to the growth of fintech is Visa (V) & Mastercard MA which both have a Zacks Rank #2 (Buy) and their top and bottom lines are naturally light years ahead of newer and smaller fintech competitors.

Newer startups are often thought of in relation to fintech more than these payment card giants, but their impact on financial technology services should not be overlooked. This is especially true when considering Visa & Mastercard’s trustworthiness with consumers and their very strong stock performance over the past decade.

Image source: Zacks Investment Research

Furthermore, innovation and expansion in the fintech area is a way for Visa and Mastercard to continue their growth as larger mature companies.

Specifically, Visa and Mastercard must be recognized since their digital wallet solutions are as widely accepted for online shopping as their debit and credit cards are globally. Through Visa Checkout and MasterCard’s MasterPass, both companies have transformed beyond plastic and evolved with the trend and the digital age of consumer commerce.

This should help preserve and grow their top and bottom line numbers for years to come. Trading at $354 a share, Mastercard sales are expected to rise 13% this year to $25.16 billion, with earnings expected to rise 15% to $12.26 a share. Sales and earnings in the financial year 2024 are expected to increase by a further 12% and 17%.

Image source: Zacks Investment Research

Swinging to Visa which trades at $225 a share, earnings are expected to rise 14% in FY23 to $8.57 a share and sales to rise 11% this year to $32.47 billion. Sales and earnings for fiscal year 2024 are projected to increase by a further 11% and 13%.

Image source: Zacks Investment Research

Block and Bitcoin

Along with PayPal, one of the more popular names in the fintech space is Block (SQ), formerly Square. Founded in 2009 and listed since 2015, Block’s notoriety came with Square Reader, the company’s first product that simplifies point-of-sale transactions by connecting to a mobile device’s autocontact.

Block’s Square Reader has been instrumental in smoother person-to-person transactions and has helped small business owners simplify the payment process alongside the larger Square Register.

Outside of hardware products, Block’s cash app has been innovative when it comes to money transfers, and the company has also implemented banking, lending and bitcoin trading to its online platform.

Image source: Zacks Investment Research

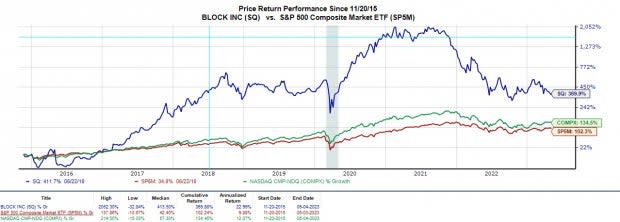

Trading at $60 per share and still up +370% since its IPO, Block’s performance has easily topped the broader indices over this period. Block has intentionally stuck to exclusively offering Bitcoin services on its platform, while other fintech companies such as PayPal include trading for a variety of cryptocurrencies.

Block’s only emphasis on Bitcoin is that it remains the most traded cryptocurrency, and the company’s concentration could bring greater returns rather than diversifying at the moment. To that point, along with offering bitcoin trading, Block has entered the crypto mining space as a producer of bitcoin chips.

Image source: Refinitiv

In particular, bitcoin prices have stabilized in recent months, and Block could be a more affordable way to gain concentrated exposure while offering diversification to its other financial services.

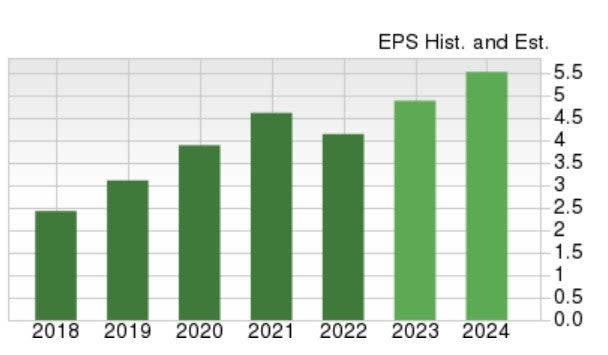

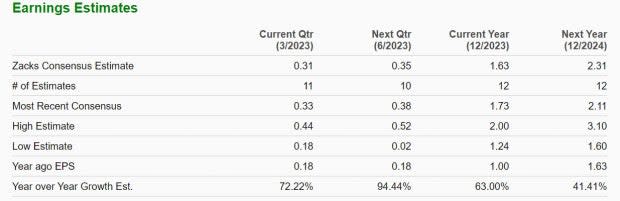

Bitcoin pulls in about 50% of Block’s revenue with SQ stock currently landing a Zacks Rank #3 (Hold). As Block continues its course of increased profitability, there could be more upside ahead with earnings projected to rise 63% in FY23 to $1.63 per share compared to EPS of $1.00 in 2022. Additionally, EPS for the fiscal year 2024 to rise a further 41%.

Image source: Zacks Investment Research

Remove

These companies are good illustrations of how the growth in financial technology services should fascinate investors. Considering the fintech market CAGR is +20%, there should be a lot of upside and growth for PayPal, Visa, Mastercard and Block stocks.

Want the latest recommendations from Zacks Investment Research? Today you can download 7 best stocks for the next 30 days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V) : Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Block, Inc. (SQ): Free Stock Analysis Report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

eBay Inc. (EBAY): Free Inventory Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research