The FTX case does not define the future of crypto markets – GIS reports

The sages risk their money on innovative products and build market knowledge. The charlatans take advantage of crypto’s inevitable unknowns. The case of FTX shows everything.

In a nutshell

- All true inventions are first misunderstood, and investors make mistakes

- Cryptocurrencies are at the forefront of financial innovation

- The FTX collapse is not a judgment on crypto’s usefulness and future

In November 2022, FTX Cryptocurrency Derivatives Exchange, commonly known as FTX, filed for Chapter 11 bankruptcy. The company was founded in 2019 and soon became the third largest cryptocurrency exchange in the world. What also set FTX apart was that it ran a cryptocurrency hedge fund and actively sought a high public profile – for example by sponsoring race car teams and donating to US political candidates. Generally, exchanges seek a much lower profile. And they distinguish between facilitating transactions and investment vehicles.

In mid-2022, reports of FTX began to pour into the market. They claimed that the exchange may have sponsored many financial research reports about itself. Alameda, the main market maker for FTX, was significantly involved in the exchange and its products – for example, by being the most significant known depositor of stablecoins on FTX. In addition, reports claimed that FTX’s data on performance, transparency and transactions were unreliable.

Unpleasant findings

Other irregularities came to light. For example, FTX appears to have systematically used the Environmental, Social, and Governance (ESG) framework to exploit unsophisticated investors. The company also made false and misleading representations that the deposits are covered by the Federal Deposit Insurance Corporation (FDIC).

What followed is well known. Investors took their capital and let FTX fall, which rippled through the entire crypto sector. Sam Bankman-Fried, the founder of FTX, is under house arrest. The valuation of crypto assets fell, even though they were not involved in FTX. Predictably, decision-makers and other players in the financial sector began to call for government intervention.

The media portrayed the collapse of FTX as a case study for all alleged problems in the crypto sector. For some, the very idea of generating private money out of an algorithm is a scam. For others, the lack of regulation in the crypto sector is the problem. Without regulation, critics surmise, there is no transparency or investor and consumer protection. And yet this criticism is wrong.

Innovation is new by definition

The value of something comes from its relative scarcity and from how it is traded between interested individuals, and it does not form an inherent mystical quality. Cryptocurrencies can be as valuable as Pokemon Go, a loaf of bread or a handful of rubies, depending on how much people are willing to pay. This also applies to money. Most of today’s currencies are fiat money. They lack intrinsic value, hence the Latin word “fiat,” meaning “to believe.”

Read more about technology and economics

The more important point in the media after FTX’s collapse has to do with regulation and transparency. Here’s the clue: Many of FTX’s products were already regulated. And most of the irregularities that led to the collapse at the end of 2022 were widely and transparently known as early as the company was founded. For example, Alameda, the research company, was co-founded by Sam Bankman-Fried of FTX. He also pushed for regulations personally by supporting the proposed Digital Commodities Consumer Protection Act (DCCPA) in the US Congress.

What disappeared in the public discourse was a completely different phenomenon. Cryptocurrencies are still a new brainchild, and the financial sector and their products are innovation-driven. Novelties and new sectors attract special groups of people: sages who invest, innovate and take risks and charlatans who see only an opportunity for personal gain.

Learning through doing

In any economic field, innovation is by definition little understood. Since it is new, the market players have not yet figured out what it is, how to use it, what results you can expect and what risks are associated with it. As these market players increasingly experiment with the innovation, they are on a learning curve and the results are becoming more and more publicly known. Transparency increases the more an innovative product is used in the market.

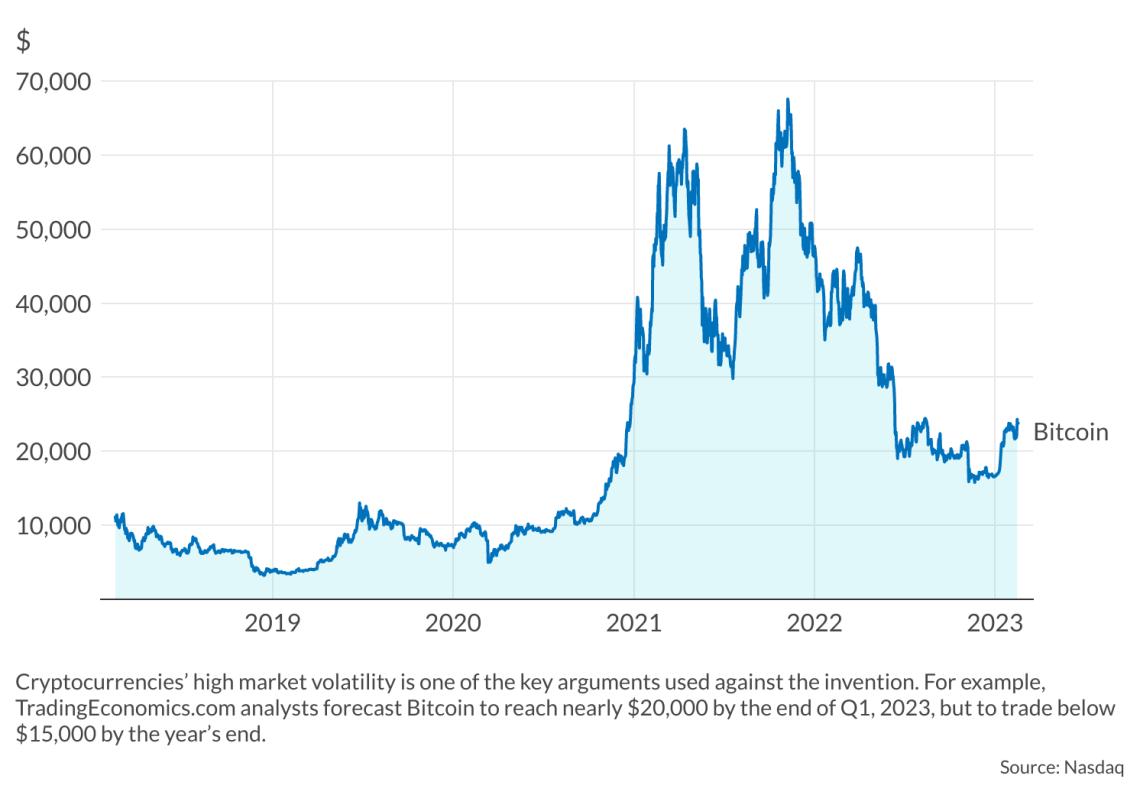

Facts and figures

Volatile cryptos

It often takes a long time before the innovation’s value proposition is sufficiently understood, and it can take even longer before the market learns to deal with it. There are bumps along this road. Consider electricity, for example: It took around 100 years before it was understood as an economic good and at least as long to find out how to use it as a value driver.

The same applies to financial innovation. As structured products and hedge funds entered the market, only a few “quants” (qualitative analysts) fully understood them. The market players learned how to use them step by step. These products too went through phases of spectacular performances, gigantic collapses, consolidation and repositioning. But the further they went through them, the better they were understood. The learning curve was also crucial in identifying the fraudsters who tried to take advantage of the innovation’s initial transparency deficit.

Innovations like crypto are difficult to exploit, as their properties are opaque by nature. The process by which market participants adopt it is similarly unpredictable. This ambiguity makes innovation interesting for investors and risk takers. But it also attracts rip-off artists who figured out how to ride a bike. In the margin of innovation, patterns of market behavior continue to form. Therefore, many of the usual markers of deception and clues to sort out the fraudsters are still missing or poorly functioning – a fact known to the pretenders.

Choose to ignore warnings

Nevertheless, even in the innovative environment, control signals can be detected, which indicate whether a business proposal belongs to the creative margin or just runs along it as a fake. Interestingly, most of the red flags applied to FTX – and regulators, professionals and occasional investors continued to ignore them.

The most glaring red flag was the institutional merger of FTX and Alameda Research. It is a well-established practice in the financial markets to separate proprietary research from market creation and implementation of products. And proprietary research itself must be conducted independently. FTX obviously broke this rule.

In addition, a stock exchange launching its own hedge funds should have set off some alarms. Another well-established practice in the financial markets is that infrastructure providers such as exchanges should not sell financial instruments that are locked into their infrastructure.

Mr. Bankman-Fried should have issued some of the usual warnings himself. An entrepreneur innovates and spends his money on people who develop products and applications. Using it for lobbying is suspect at an early stage of the company’s development. Whenever a company owner embarks on the business of regulation, he aims to redistribute benefits to himself and not create them—which is unfortunate with innovation. FTX’s founder’s entanglements with politics and a push for regulations should have been enough to question his entrepreneurial spirit.

These warnings are not specific to the financial sector. They apply to any investment and economic activity. They relate to management, the product and the people behind a business model. Note also that all these aspects were transparent before FTX’s collapse and that no regulation could have made them more transparent. In this case, people would just follow Mr. Bankman-Fried.

Scenarios

What scenarios follow for the crypto sector after the FTX fall? Here are the leading opportunities.

Organic development and market growth

In the most likely scenario, cryptocurrencies will continue to grow as a market and in scale. However, this will be accompanied by a two-part consolidation. Firstly, the infrastructure of the market, the stock exchanges, will consolidate. Second, the cryptotypes used will be paired. These types will form the short head, while the others will end up somewhere in the long tail.

Strong candidates for the short head are cryptos with well-established rules and transparent transactions – such as bitcoin – or those that operate on or as a base technology for other applications, such as Ether. In this scenario, increased regulation, higher operating costs and government cooperation (at least of the infrastructure) are likely. On the other hand, the learning curve of the market, increased transparency and differentiation of products will allow for a mainstreaming of crypto.

The best-case scenario is similar to the most likely, but it establishes itself much faster and without (much) government intervention. In the most likely case, the market will need another decade to make its learning curve, and at best it may do so in the next five years. As the crypto sector consolidates, the exponential increase in information slows, allowing for more transparency and the establishment of recognizable patterns in crypto markets and products.

Two drivers provide the speed in this scenario. The first is the innovation in the crypto sector itself. Entrepreneurs continue to be interested in innovation, especially in streamlining their products, which increases quality. The second is the absence of regulation and government cooperation, which means that innovation, information and risk-appropriate behavior can be synchronized with less friction. The probability of this scenario is medium-low.

The demise of cryptocurrencies

The worst case scenario is to die out of the crypto sector altogether. On the one hand, investors and innovators may be disappointed and decide that the potential for using cryptocurrencies is limited. In that case, cryptos do not compensate for the higher risk, making them unattractive. On the other hand, governments can either ban crypto or regulate the sector in a way that drives costs up and investors out of the market. In this scenario, the crypto market contracts, leaving a niche application on the fringes of the markets. The probability of this scenario is low because there is a strong buy-in sentiment in the crypto sector. While FTX’s fall rippled through the market, there was a recovery afterward. In addition, the pace of innovation in this sector appears to be independent of FTX.

FTX’s meteoric rise and collapse is not surprising. The crypto sector is at the forefront of financial market innovation. It attracts sages and charlatans alike. The sages are the entrepreneurs who invest their money, take risks and try to learn from the market. The charlatans play on the new market’s lack of transparency, sending money into their pockets. As the market develops, innovation calms down, increasing transparency and allowing market players to catch up on the learning curve. The more freely they can do it, the faster the invention enters the mainstream and becomes more stable and accessible.

, Ethereum (ETH/USD), Dogecoin (DOGE/USD)")