Tanzania and its Fintech ecosystem in 2022

What have been some of the developments in fintech and broader digital ecosystems in the East African nation of Tanzania?

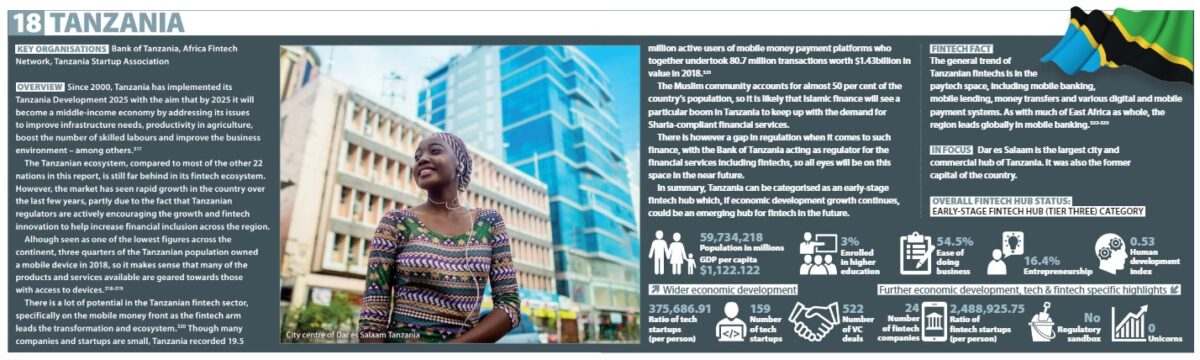

As highlighted in my previous Fintech Times Fintech: Middle East and Africa 2021 ReportTanzania has implemented its economic development strategy, Tanzania development 2025since the beginning of the new millennium in 2000. The goal is for Tanzania to become a middle-income economy by 2025: address the issues of improving infrastructure needs, productivity in agriculture, increasing the number of skilled workers and improving the business environment – to name a few.

According to a study from UN Capital Development Fund (UNCDF) Last year, Tanzania’s fintech landscape has grown and changed positively due to regulatory reforms in the payments sector launching government policies and initiatives focusing on information and communication technologies (ICT). This was evident in 2015, when the Tanzanian government established Information and Communication Technology Commission (ICT Commission), which has the mandate to coordinate and facilitate the implementation of national ICT initiatives. The government also has a MoU with an ecosystem facilitator Financial Sector Deeeping Trust (FSDT), where FSDT can provide financial and technical support to the financial sector, while the state provides support to the sector with legal and regulatory frameworks.

This has helped Tanzania to catch up and advance digitally as fintech services at the time were mainly limited to the purchase of airtime, cash deposits and money transfers and withdrawals. To note, when it comes to the fintech sub-sectors, of the 33 estimated fintechs in Tanzania, lending / financing and payments / remittances were the two most popular with 14 and 10 fintechs, respectively. In third place came savings with five; fourth place, insurance with four fintechs; enables processes and technologies in fifth with three fintechs, and finally personal finance with two fintechs.

Like the rest of its other East African peers, Tanzania has seen mobile money contribute to the economic inclusion of large sections of the population. The proportion of Tanzanian citizens using formal financial services grew from just 16 percent in 2009 to 65 percent in 2017. Since June 2021, Tanzania has had over 33 million (33.2) mobile money accounts opened – all according to Global Mobile Communication System (GSMA).

As of last year, there are currently six mobile network operators (MNOs) in Tanzania, with many partners with financial service providers enabling peer-to-peer (P2P) payments via mobile wallets and digital banking services. Some of these players include M-Pesa from Safaricom, Tigo Pesa from Tigoand Airtel money.

In July last year, the country introduced a new tax on mobile money transfer and withdrawal transactions (minus merchants, companies and public payment transactions). This tax is in addition to their VAT of 18 percent and excise tax on mobile money transfer and withdrawal fees of 10 percent.

From a report from GSMA that analyzed the effect of this, it stated that until June 2021, taxes on mobile phone fees were 23 percent of total transfer costs, but in July and August last year it was 60 percent. To put this in perspective, from July last year with the tax, Tanzania’s average transaction was three times higher than the average tax in East Africa (previously the country had been in line with the average for the region). This saw dramatic declines in transactions from June to September last year, for example with P2P transactions falling by 38 percent. Towards the end of the year, however, it seemed that mobile money has slowly recovered and increased again after the “shock” in the fee. Nevertheless, it is estimated that the market fell by 12 percent as a result, and the future growth of it will be less than the pre-tax.

It can present a problem, if it is too expensive, as people in Tanzania can resort to cash again, which will ruin any digital gain mobile money has had in the country.

Another problem has been the lack of regulations, including the lack of a regulatory sandbox, since they have been unclear to many of fintechs and broader technology companies in the country.

An additional challenge for startups and fintechs has been the lack of funding and / or mentorship. For the estimated 33 fintechs in the country, only 36 per cent of them have managed to secure seed financing or growth financing, while 35 per cent start up via friends and family members.

Nevertheless, it seems that more is happening and that the ecosystem is moving forward. At the end of last year, for example Bank of Tanzania announced that they were in the process of developing a central bank’s digital currency (CBDC) – assuming it would be the digital version of the current currency Tanzanian Shilling or e-Shilling.

Despite the fact that the fintech ecosystem is more infant than its other peers in the Middle East and Africa (MEA), there have been organic successes. Earlier this year, it became known that Tanzanian fintech NALAa cross-border payment company, was able to collect $ 10 million in seeds.

Tanzania has been one of the African continent’s fastest growing economies, with seven percent average annual growth in national gross domestic product (GDP) since 2000. It is also one of the 10 largest countries in Africa by population, showing that the transition from a low medium to a middle-income economy (and beyond) will offer opportunities and inclusion for all its inhabitants.

The country compared to the others is still lagging behind in terms of fintech and broader technology ecosystem. Nevertheless, it has played catch-up and has achieved what it could so far. It will be important for the growth of the ecosystem that further incentives and initiatives for fintech take place, as well as partnerships and further cooperation and expansion of the ecosystem – education and training, accelerators / incubators, to name a few.

Finally, in the broader technology ecosystem, there are organic examples. One of them is Silicon Dar, an initiative to promote the new technology district Dar es Salaam, which according to their website is home to several innovation hubs, telecom companies, colleges for ICT. University of Dar es Salaamdata centers, Commission on Science and Technologytechnology start-ups and business incubators.

Tanzania’s growing economy could make fintech play a strong role in the future, as it has already made an impact on the lives of many Tanzanians.