Sea Limited: Performing Well Against Profitable Growth (NYSE:SE)

cook

This article was first published in Outperforming the Market on May 16, 2023.

Sea Limited (NYSE:SE) just reported its earnings on May 16, and I’ll delve deeper into its 1Q23 results to provide insight into the company, its fundamentals and where it is going next.

I continue to believe that Sea Limited is working well to grow profitably and sustainably, while investing in the business to continue to maintain and grow its leadership position in multiple markets.

A brief introduction

For readers unfamiliar with Sea Limited, I have shared with members of Outperforming the Market a deep dive into Sea Limited, which, among other things, delves deep into the company’s three business segments, competitive landscape and valuation.

Sea Limited has three main businesses. First, it has a gaming business, the Digital Entertainment business, and its revenue is largely contributed of Garena’s top game, Free Fire. Second, it has an e-commerce business, Shopee, which is a leader in Southeast Asia and Taiwan and growing rapidly in Brazil. Finally, it has the digital financial services business, called SeaMoney, which provides users with fintech solutions.

Summary of Sea Limited’s 1Q23

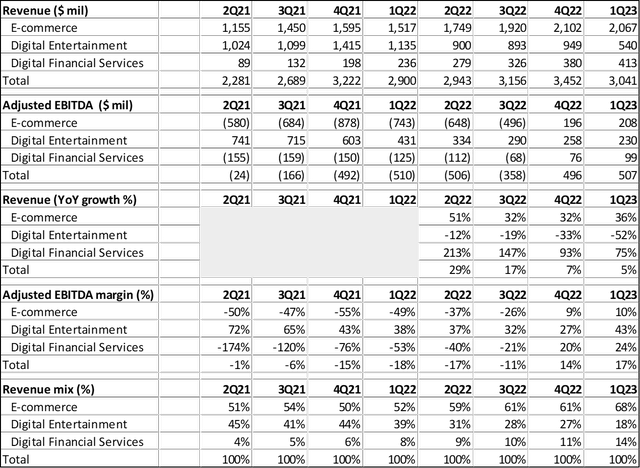

During the first quarter of 2023, Sea Limited generated $3.04 billion in revenue, which was equal to the $3 billion market expected.

However, the EPS figure disappointed as Sea Limited generated 15 cents per share, lower than the 73 cents per share expected by the market.

I have created the table below to show some important things:

- As of 1Q23, e-commerce revenue growth accelerated to 36% while adjusted EBITDA margin improved from -49% a year earlier to 10% in 1Q23. This means that Sea Limited’s e-commerce segment can continue to grow despite the focus on profitability.

- The Digital Financial Services revenue mix has increased dramatically from 4% of revenue in 2Q21 to 14% of revenue in 1Q23, almost catching up to the revenue contribution of the Digital Entertainment segment.

- The Digital Entertainment segment continued to experience weak growth, but adjusted EBITDA margins remain high at 43%. In addition, we can see that the valuation of Sea Limited is increasingly driven by the e-commerce segment given the increasing revenue and adjusted EBITDA contribution it will make.

Sea Limited financial summary (author generated)

The e-commerce segment continues to grow more profitably

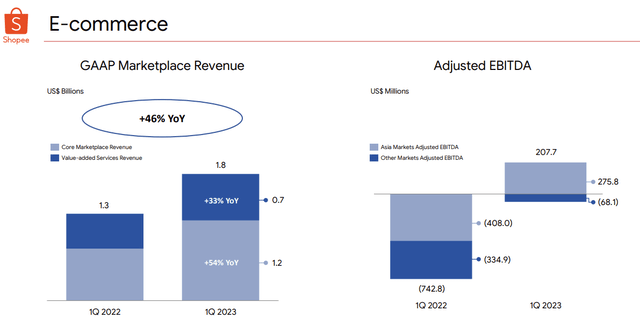

In the first quarter of 2023, Shopee revenue grew to $2.1 billion, up 36% from the previous year. This comes as the company increases revenue generation. Core market revenue grew to $1.2 billion, up 54% from the prior year as a result of higher advertising revenue and transaction-based fees.

Adjusted EBITDA improved to $208 million in the first quarter of 2023, compared to the loss of $743 million from the prior year. This is a huge improvement, in my view, and is the result of monetization efforts and continuous improvements in operational efficiency

E-commerce segment (Sea Limited IR)

In particular, Adjusted EBITDA for Shopee’s Asia markets improved from a loss of $408 million in the prior year to a positive Adjusted EBITDA of $276 million in the current quarter. In the other markets, adjusted EBITDA loss continues to narrow significantly, in my view, from last year’s adjusted EBITDA loss of $335 million to this quarter’s adjusted EBITDA loss of $68 million. In particular, the contribution loss per order in Brazil improved by 77% compared to the previous year and reached $0.34 per order. This was a result of more efficient sales and marketing costs and also improved revenue generation.

I am of the opinion that revenue growth for the e-commerce segment remains surprisingly robust despite a decline in sales and labeling spend. Additionally, the continued improvement in profitability is encouraging, and underlines to me that this improvement is sustainable in the longer term.

Focus for Shopee in the quarter

One aspect that Shopee has focused on this quarter is improving its logistics cost management and delivery experience. It is looking to improve its logistics capacity and increase the integration of its internal logistics arm and its third-party logistics partners. As a result of using more automation in the delivery process, this has seen Shopee reduce its average delivery time by more than half a day across its markets in the first quarter.

In addition, Shopee also improved and expanded its buyer coverage of its logistics services in the first quarter, with more than 95% of Shopee’s buyer base now covered by Shopee’s delivery services. In Brazil, management shared that they continue to expand on their first and last mile in the country, and that they also have eight distribution and sorting centers in Brazil today. Shopee has also recently opened 15 new hubs in the past few months in an effort to improve logistics capabilities.

Another aspect that management is focusing on for Shopee is increasing its AI capabilities to improve not only the user experience but also drive operational efficiency. Shopee will also use AI to recommend more relevant products to users on its platform, and this has led to higher order conversion rates as it improves product discovery on the Shopee platform. Shopee has also adopted major language models to improve its own AI-powered chatbot, aiming to provide users with a better user experience, improved resolution of problems and shorter waiting times.

Digital entertainment

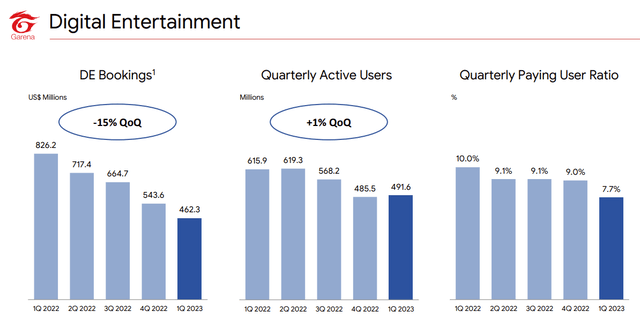

The Digital Entertainment segment provides headwinds to Sea Limited’s total revenue and EBITDA today, with Digital Entertainment revenue down 52% year-over-year and Adjusted Digital Entertainment EBITDA down 47% year-over-year. This was a result of weakened monetization in the segment as the ratio of paying users continued to be weak.

However, it was positive to see constructive comments about Garena from management during the earnings call.

Management indicated that they saw initial signs of improvement in Garena’s quarterly active user base, which increased 1% sequentially from 485 million in the previous quarter to 492 million in the first quarter. Positive user trends for Free Fire were also cited in April when management noted that Free Fire actually achieved a new peak in monthly active users over the past 8-month period. Additionally, as a result of ongoing efforts to improve gameplay and user engagement in Free Fire, there were positive responses to the recent improvements made to Free Fire.

Operational objectives for digital entertainment (Sea Limited IR)

On top of that, management also highlighted that Arena of Valor, the second largest game, reached a new record of quarterly active users and orders in the quarter. This comes after more than six years since the game launched and continued efforts to engage with users and improve monetization.

Finally, management highlighted several new titles it is launching, with Undawn expected to be published in Southeast Asia in the coming months, as well as the release of Black Clover Mobile in several global markets. Management has used AI to improve the efficiency of gaming operations, as they appear to be using AI to localize some of the content of the games to improve execution in the long run.

Given the comments on Free Fire and the new launches expected in the next few months, along with the end of the full year since Free Fire metrics started to deteriorate, I think we could see Garena bottom either this quarter or next, if Free The Fire trend continues to stabilize or improve.

SeaMoney’s growth continues

SeaMoney had a solid quarter, with revenue reaching $413 million in 1Q23, up 75% year-over-year. Importantly, SeaMoney generated $99 million in adjusted EBITDA, compared to an adjusted EBITDA loss of $125 million the year before. This improvement in adjusted EBITDA was a result of solid revenue growth, along with continued efforts to optimize costs as well as efforts to improve efficiency, including optimization of sales and marketing expenses.

SeaMoney’s credit business continues to grow. Sea Limited’s total loan receivables on the balance sheet reached $2 billion in the quarter, and net of credit losses is $281 million.

In addition, non-performing loans overdue for more than 90 days remained stable at 2% as a percentage of total gross loan receivables.

I would also like to note that management has been looking to diversify its funding sources, which include Sea Limited’s own bank deposits, channeling arrangements and bilateral asset-backed facilities with local and regional banks, and the company is looking to further diversify this by bringing in more financial investors. The majority of SeaMoney’s loan book is currently already financed from alternative sources other than own cash on the balance sheet.

SeaMoney also uses AI to improve its risk management capabilities to assess the fraud and credit risk of its users and to improve the KYC process for its products.

On top of that, management continues to expand its offerings at SeaMoney as it has been testing new insurtech products and more features and services in its banking apps. I also like that the team wants to integrate and synergize their SeaMoney and Shopee business to make it more seamless for users to use both offerings.

Last but not least, management remains confident in SeaMoney’s long-term potential and is expanding the SeaMoney business in a prudent manner to deal with the uncertain macroeconomic environment.

Money

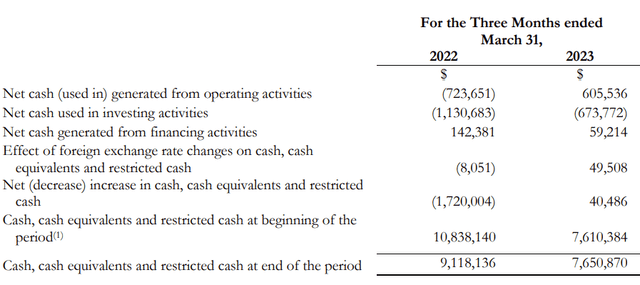

In 1Q23, Sea Limited achieved a net cash flow from operating activities of around US$606,000, a huge improvement from the cash flow of around US$724,000 in the previous year.

As a whole, Sea Limited added $40 million in cash during the quarter. I continue to be amazed at Sea Limited’s ability to turn its cash flows from last year’s total negative cash flow of $1.7 billion to a positive total cash flow of $40 million this quarter.

Sea Limited cash flows (Sea Limited IR)

Valuation

I reiterate my 1-year price target set for Sea Limited in my Sea Limited deep dive following this 1Q23 earnings report.

My 1-year price target for Sea Limited is based on a mix of DCF and the P/E method. For the P/E multiple method, I assume a 32x 2024F P/E for my estimate of Sea Limited’s 2024F EPS. For the DCF method, I assume 20% cost of equity and 20x terminal multiple.

Therefore, my 1-year price target for Sea Limited is $94.51, suggesting a 30% upside from today’s levels.

I would like to highlight that the way Sea Limited should be valued is changing a lot, as it used to be valued as a gaming company as Garena was the main part of the business, but today e-commerce and digital financial services are increasingly important to the Company.

Conclusion

Overall, I believe that 1Q23 was a strong quarter for Sea Limited as it showed that it can still grow rapidly despite its focus on operating efficiency and profitability. The company showed strong improvements in adjusted EBITDA margins for the Digital Financial Services segment and the E-commerce segment. While there continued to be headwinds to monetization in the Digital Entertainment segment resulting in revenue headwinds, adjusted EBITDA for the segment remained quite solid.

The first quarter of 2023 was another strong quarter for us across our businesses. We are focused on maximizing operational efficiency and improving user experiences. We continued to make meaningful progress on both fronts. We reinforced our commitment to achieving strong cost leadership for our ecosystem. We believe this will reinforce our structural advantages in driving profitable long-term growth in our markets. As a result, we continued to see significant year-on-year improvement in profitability for both Shopee and SeaMoney.

Therefore, my 1-year price target for Sea Limited is $94.51, suggesting a 30% upside from today’s levels.