Nu Holdings: Buffett-Backed Fintech Has Crypto Tailwinds (NYSE:NU)

Jirsak

Nu Holdings Ltd. (NYSE:NOW), or “Nubank,” is the largest Fintech bank in Latin America and is on a mission to “bank the unbanked” in the region. The company was founded in 2013 and backed by a number of top investment firms from Sequoia Capital to Tiger Management and even Chinese tech giant Tencent (OTCPK:TCEHY)(OTCPK:TCTZF).

Latin America is fertile ground for major fintech disruptions. The continent has a large unbanked population, high mobile interest usage and favorable public regulation. Therefore, Nu Holdings is poised to continuously benefit from these tailwinds, as well as those provided by cryptocurrency, which is a service the company provides (more on this later).

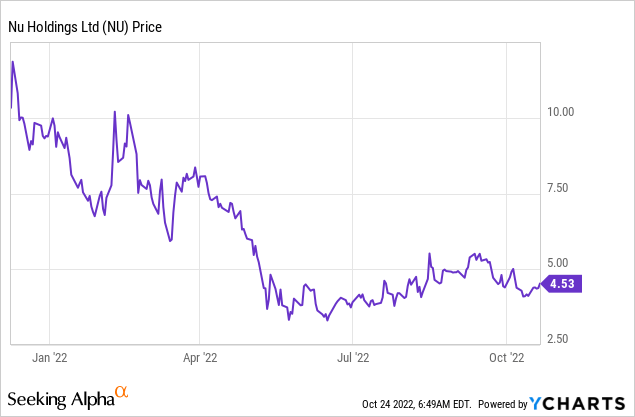

In addition, Warren Buffett’s Berkshire Hathaway ( BRK.A )( BRK.B ) sold stakes in payments giants Visa ( V ) and Mastercard ( MA ) in the first and second quarters of 2022 and loaded up on $1 billion worth of shares in Brazilian fintech bank. Berkshire Hathaway bought 107 million shares at an average price of ~$9.38 per share. At the time of writing, Nu Holdings is trading at ~$4.53 per share, which is now significantly cheaper than the level at which Berkshire invested. Therefore, in this post, I will break down the company’s business model, financials and valuation. Let’s dive in.

Fintech business model

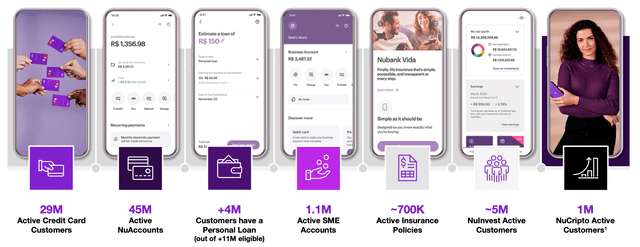

Nu Holdings was founded in 2013, as a single solution fintech application that made it possible to manage a Mastercard credit card through a mobile application. Following the success of this, the company launched a loyalty card program, loans and then of course crypto. At the time of writing, the business has 29 million active credit card customers, 45 million active accounts, and over 4 million customers have personal loans through the business. Nubank also caters well to small and medium-sized businesses and has 1.1 million of these users on its platform.

NuBank product (Investor presentation)

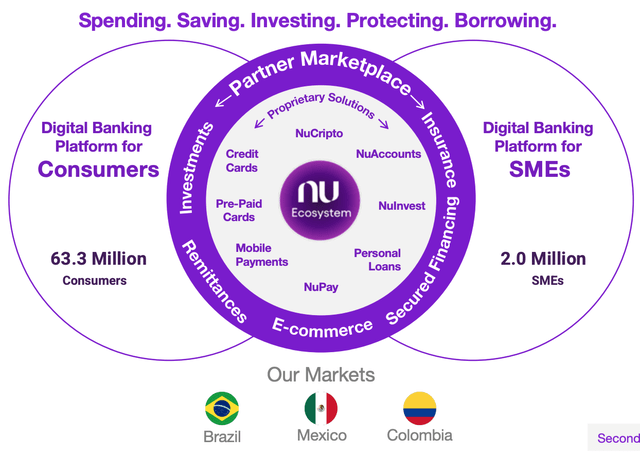

The platform is essentially like the European fintech app Revolut, but on steroids. It enables consumers to spend, save, invest, protect and borrow. The company is the number one issuer of new payment cards in the three main markets of Brazil, Mexico and Columbia.

The NuBank Platform (investor presentation)

In late October 2022, Nubank announced its plans to launch its own custom cryptocurrency on the Polygon/Ethereum Blockchain. The plan is to launch these crypto tokens to 2,000 users initially for testing as part of a larger reward program in Brazil. This could be a real game-changer, as it could offer another revenue stream for the business, while leveraging the popularity of crypto, but with its own solution.

Growing economy

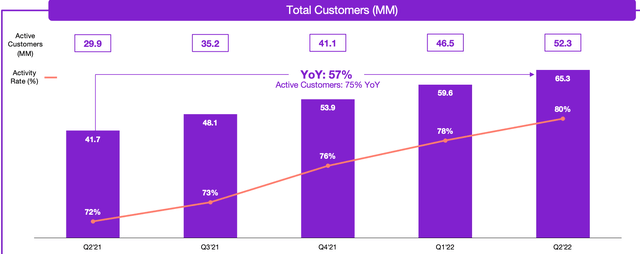

Nu Holdings generated solid business results in the second quarter of 2022. The number of customers was 65.3 million, which reached a record high for both retail and SME customers. This was mainly driven by strong user growth in the company’s main market, Brazil. Users in this region increased by a rapid 51% year-on-year to 62.3 million, and the activity rate reached a record high of 80%. Nu customers now represent a staggering 36% of Brazil’s adult population.

The platform is also the primary bank for over 55% of the monthly active customers. This is an important confirmation of trust for the business, as it means that users do not need to have an older bank, which solves the potential for Nubank. In Mexico, the customer base of the business increased by a rapid 6 times to 2.7 million. In Colombia, the company also increased its users to 314,000. Tracking the “Activity Rate” is key to the success of the platform, as users using the platform more regularly are likely to complete more transactions. In this case, we see that the business has increased its activity rate from 72% in Q2.21 to 80% in Q2.22, which is positive.

Total customers (Q2 Earnings Report)

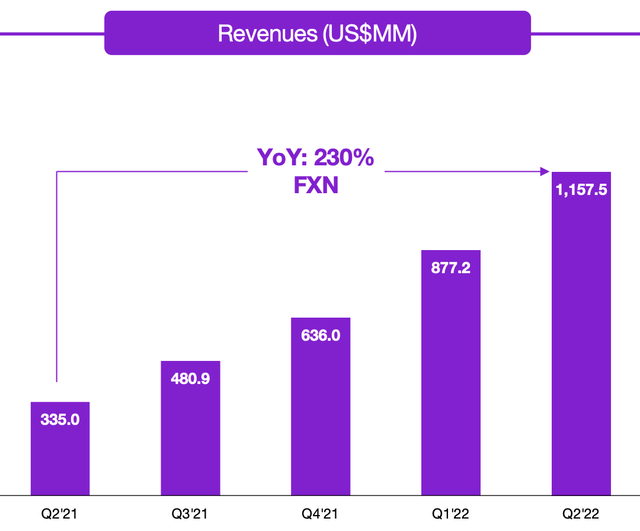

Nubank generated record revenues in Q2.22 of $1.2 billion, which increased a whopping 244% year-over-year. The company also generated a strong gross profit of $363.5 million which was up 118% year over year. Gross profit margin was squeezed from 50% in Q2.21 to just 31% in Q2.22. This was mainly driven by rising interest costs. As the company’s loan portfolio matures and interest rates begin to stabilize, I estimate that gross margins will recover, which is in line with management’s predictions.

Income (Q2,22)

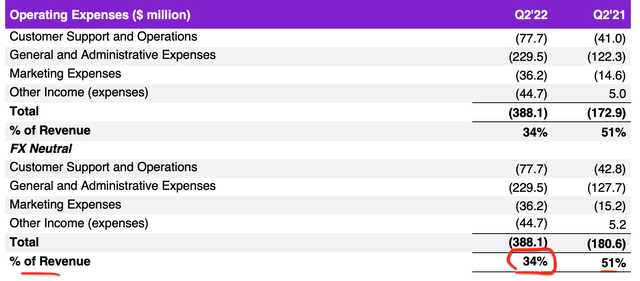

Nubank generated solid operating expenses of $388.1 million, which increased by a rapid 124% year-over-year. This increase in expenses was driven by growth in customer support expenses and marketing. General and administrative expenses increased by an eye-popping 88% year-over-year, which was primarily driven by an increase in headcount and stock-based compensation. Although an increase in expenses may look bad at first glance, as a percentage of total revenue, expenses have fallen from 51% in Q2 2021 to just 34% by Q2 2022. Therefore, the business shows increased operating leverage, which is a positive sign going forward and means that top line revenues are growing faster than bottom line costs. The credit portfolio particularly benefits from a larger scale as the low-cost deposit base can help expand the net interest margin.

Operating costs (NuBank)

The company reported a net loss of $29.9 million in Q2 2022, which is worse than the $15.2 million produced in Q1 2022. This was driven by stock-based compensation and the aforementioned factors. Analyzing the balance sheet of Nu Holdings is quite challenging as capital requirements, like any bank, can skew the accounts. At first glance, however, it looks like the business has $3.7 billion in cash and cash equivalents. In addition to total debt of $617 million, this means the company is in a solid liquidity position overall.

Advanced valuation of Nubank

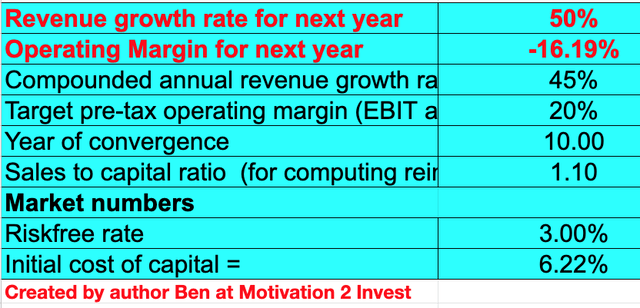

To value Nubank, I have plugged the latest financials into my advanced valuation model, which uses the discounted cash flow method of valuation. I have predicted a steady income growth of 50% for the next year and 45% per year for the next 2 to 5 years. This is much less than the previous growth rate of 244%. Therefore, I believe that this revenue growth is relatively conservative and achievable, given the huge number of platform tailwinds and upsell opportunities.

Nubank share valuation 1 (created by author Ben at Motivation 2 Invest)

I have predicted that the company will increase its operating margin from -16.19% to 20% over the next 10 years. I estimate this will be driven by the increasing operational leverage identified earlier and further platform efficiencies.

Nubank share valuation 2 (created by author Ben at Motivation 2 Invest)

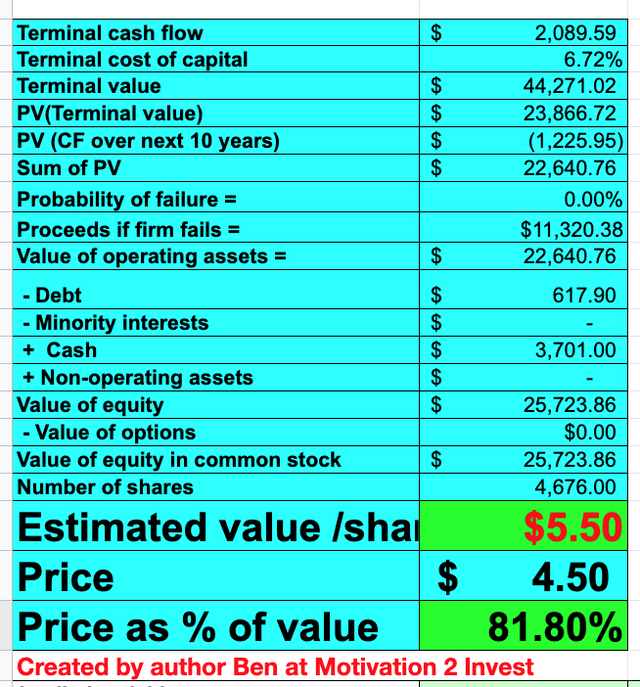

Given these factors, I get a fair value of $5.50 per share. The stock trades at $4.50 at the time of writing, so it is at least 18% undervalued. As an additional data point, the stock is trading at a price/sales ratio = 4.88 which is cheaper than historical levels.

Risks

Decrease in decrease/payments

Brazil has a fairly high inflation rate of 7.17%, and the central bank has raised interest rates 12 times to combat this. Therefore, analysts predict stagnant growth and declining exports over the next year at least. A slowdown in economic activity is not a good sign for any fintech or payments company, as they tend to gather revenue from payment volume. In addition, higher input costs for the consumer could lead to higher default rates for loans. The good news is that inflation has started to fall in Brazil, but is still higher than pre-pandemic levels of ~4%.

Final thoughts

Nu Holdings is a dominant fintech company that has truly disrupted the traditional banking system in Brazil and Latin America as a whole. The company will face competition from the “Amazon of Latin America” MecardoLibre (MELI) which offers loans and Fintech payments. However, Nu Holdings is a pure fintech play that has a multi-platform solution that is used by a large percentage of people for their traditional banking. The share is undervalued at the time of writing and thus appears to be a great long-term investment.

![Deciphering the link between Bitcoins [BTC] block sizes and miner fees](https://statics.ambcrypto.com/wp-content/uploads/2023/05/AMBCrypto_three_bulding_blocks_with_each_bigger_than_the_last_w_4cc3870d-30bd-4a69-b3f3-2c5b6e98f1af-1000x600.png "Deciphering the link between Bitcoins [BTC] block sizes and miner fees")