Marqeta stock: FinTech with $ 30 trillion market opportunity (NASDAQ: MQ)

2Ban / iStock Editorial via Getty Images

The FinTech market (financial technology) is growing at a rapid pace, as consumers demand faster payments, frictionless experiences and lower costs. According to a study, the Fintech industry was valued at $ 112.5 billion 2021 and is expected to grow at a rapid 19.8% compound annual growth rate (CAGR), reaching $ 332.5 billion by 2028. The number of Fintech Unicorns (valued at over $ 1 billion) has quadrupled the last 18 months and is now a total of 241.

Marqeta, Inc. (NASDAQ: MQ) is a modern card issuing and processing platform, running many of these Fintech unicorn card programs, from Square (SQ) to DoorDash (DASH), Coinbase (COIN) and even Uber (UBER). The company processed $ 125 billion in payment volume over the past 12 months, of the $ 847 billion card-based payment market.

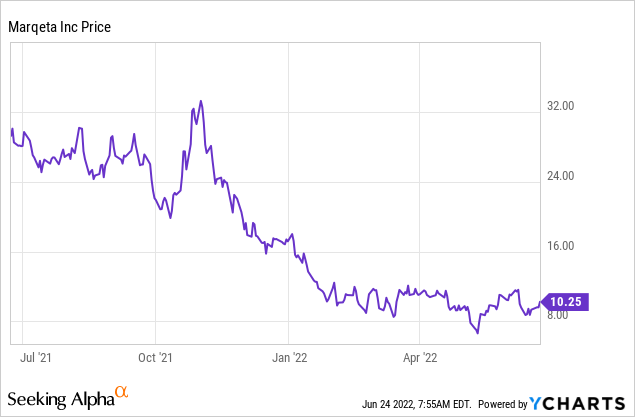

Marqeta was founded in 2010 and struggled to find the product market suitable for 2015. Since then, they have increased revenues rapidly, by 40% to 55% CAGR, which gave them momentum for listing in June 2021. The company was listed at. $ 31 per share, but since then the share price has fallen by 67%. This decline was mainly caused by high inflation and rising interest rates. The macro environment has compressed the valuation multiples for all “growth stocks” because their valuation is weighted more against future cash flow estimates. Despite this decline in the share price, the company has had a strong quarter, with revenue growth of over 54%.

The stock is now undervalued in itself, according to my discounted cash flow model, while according to the company, they are attacking a $ 30 trillion total addressable market (“TAM”) across global card payments.

Let’s dive into the business model, the economy and the advanced valuation for the juicy details.

Modern business model

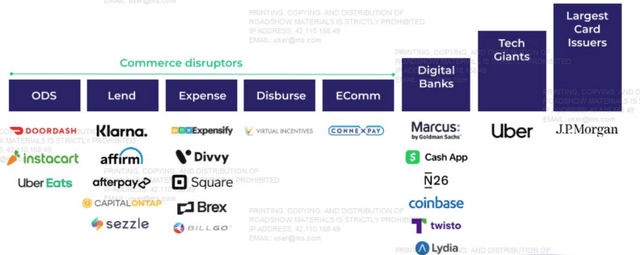

Marqeta is a modern card issuing and processing platform. Traditionally, if a company wanted to build a card program, they had to go through sitting banks. This was a time consuming, archaic and costly process with limited flexibility. Marqeta’s platform uses an open API (Application Programming Interface), which puts the power of card issuance in the hands of Fintech Innovators. The goal is to enable their elite Fintech customer base such as Square, DoorDash, Uber, Coinbase, Klarna and more to quickly launch, globally scale and flexibly manage their modern card programs.

The company offers three main services:

- Card issue: This service makes it possible to issue physical, virtual and tokenized cards. This is the type of card you see in your Apple Pay or Google Pay mobile wallet.

- Treatment: This involves transaction authentication (3DS secure), Spend Controls and even Just in time (JIT) financing, which can free up cash flow for businesses and reduce fraud.

- Applications: The Marqeta platform offers a complete dashboard, which allows user-friendly transaction monitoring and configuration of services to suit business needs.

Marqeta (Investor presentation)

Customer case studies

The square

Marqeta has been working with Square (now called Block) since 2018. They are the backbone of the “Square Card” used with Square’s popular Cash App. This enables immediate access to funds for small business owners, helping them improve cash flow and manage business expenses. Square is Marqeta’s largest customer and generates approximately 70% of their total revenue.

DoorDash

A good example of Marqeta in action is with DoorDash, an online food delivery company. The platform is the backbone of DoorDash’s red card program, which is given to each “Dasher” (delivery driver) to pay for orders. Just In Time Funding means that the cards are loaded with the “just” the right amount to pay for an order, and expense checks help prevent fraud.

Doordash red card (Marqeta customer recommendation)

Coin base

Coinbase Global is one of the most popular crypto exchanges in the world. The Coinbase card (powered by Marqeta) allows users to use their cryptocurrency in the real world.

Buy now, pay later (Klarna, Affirm, Afterpay)

Klarna is Europe’s leading supplier of Buy Now, Pay Later (“BNPL”). They used the Marqeta platform to launch a short program of just three months in Australia, while older technology would take much longer. Recently, they announced the “Klarna Card” built on Marqeta that enables US consumers to “buy now and pay later” anywhere with their “Pay in 4” solution both online and in stores. BNPL providers Affirm (AFRM) and AfterPay also use Marqeta’s platform for their virtual wallets and lending services.

JP Morgan

The world’s largest bank JPMorgan Chase (JPM) announced a partnership with Marqeta, for a virtual card system for their commercial customers.

Goldman Sachs

Goldman Sachs (GS) also collaborates with Marqeta, in relation to their digital banking services, Marcus Platform.

Income model

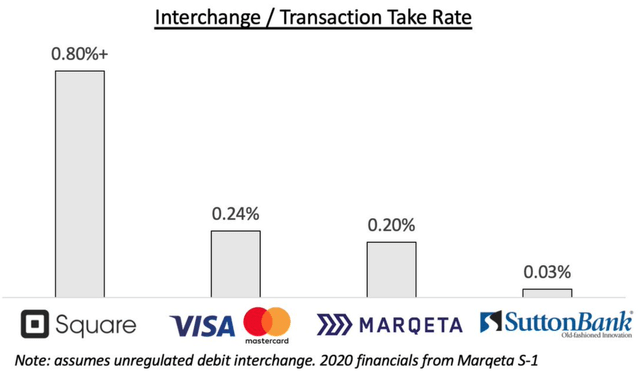

Marqeta has a usage-based model, which is based on payment processing volume. Their income comes from charging Interchange Fees, Platform access fees, fraud monitoring services, ATM fees and tokenization services. Their revenue model is in line with the customer’s incentives. The more creative ways customers can increase their payment volume, the more benefits Marqeta and its customers will benefit.

Marqeta exchange fee (S1 Filing Data & James Ho Twitter))

Technical model

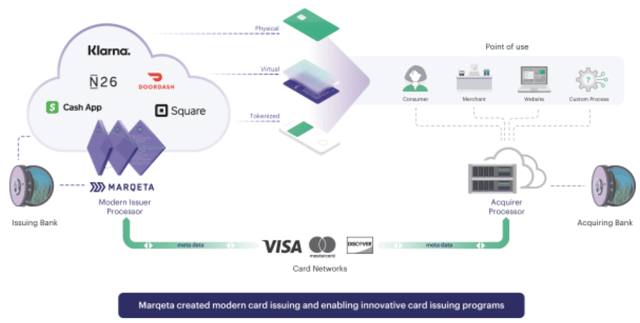

Marqeta’s platform sits at the center of Fintech customers, card providers such as Visa, Mastercard, Pulse (Discover) and issuing banks. The unique thing about their platform is their Open API. This is a software engineer’s dream with good documentation, high reliability (99.9%) and even a sandbox environment for testing.

Marqeta (S1 Filing SEC)

Growing economy

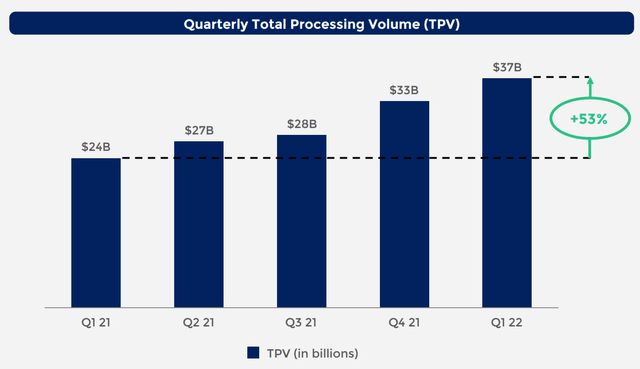

Marqeta generated some amazing financial results for the first quarter of 2022. Total treatment volume (TPV) was $ 37 billion, a rapid increase of 53% from year to year. While net income was $ 166 million, an increase of 54% year over year.

Treatment volume (Q1 Revenue Report)

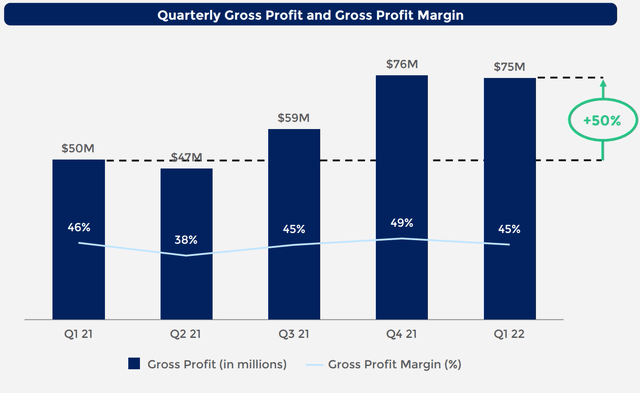

They generated a gross profit of $ 75 million for the first quarter of 2022, which increased by a rapid 50% from year to year, resulting in a gross margin of 45%. The gross margin was somewhat down from 49% in Q4, but still in line with the previous quarters.

Gross profit (Supplement for income report for 1st quarter)

Marqeta reported a loss of $ 61 million and an adjusted EBITDA loss of $ 10 million in the first quarter of 2022. The company’s largest expense was compensation and benefits, which amounted to $ 100 million. While investing $ 11 million in technology, about double the previous year. Marketing costs came in at $ 559 million, an increase of only 12% from year to year.

The company has a robust balance sheet of $ 1.2 billion in cash and cash equivalents, a decrease of approximately 4% from the previous year. In addition to $ 447 million in transferable securities. An analysis of the balance sheet shows no interest-bearing debt, which is fantastic and only $ 11.6 million in operating leases, presumably for their offices in Oakland, California, London, the UK and internationally.

Advanced valuation

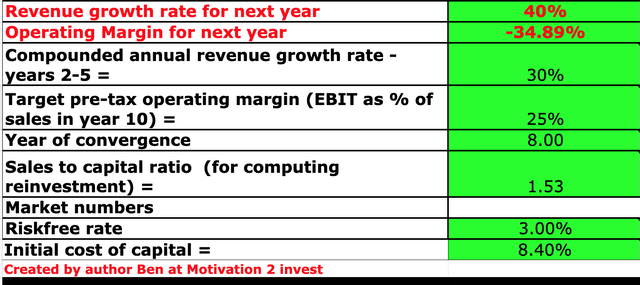

To value Marqeta, I have plugged the latest financial calculations into my valuation model, which uses the discounted cash flow method for valuation. I have predicted 40% revenue growth for next year, which is at the conservative end of the company’s own guidance. In addition, I have predicted 30% income growth for the next 2 to 5 years, which is also quite conservative based on historical growth rates of 50% +, albeit from a lower income base.

Marqeta valuation (created by author Ben Alaimo)

I have predicted that the operating margin will increase to 25% over the next 8 years as the company scales, which is the average for the software industry.

Marqeta valuation model (created by author Ben Alaimo)

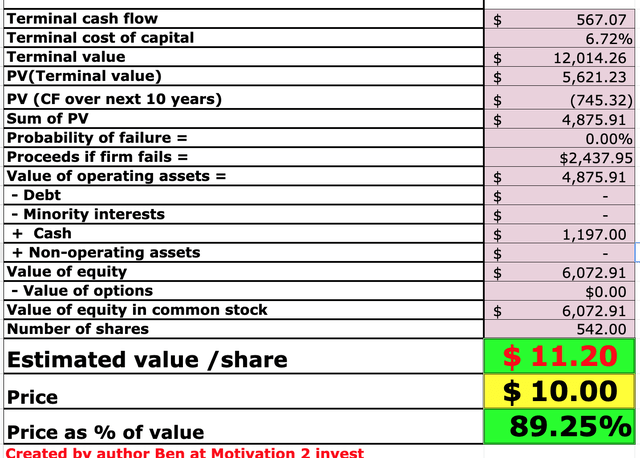

Given these factors, I get a fair value of $ 11.2 per share, which means the stock is ~ 11% undervalued at the time of writing.

Monte Carlo simulation

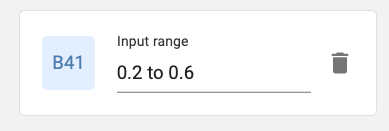

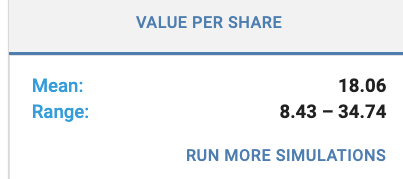

The valuation above is a fairly conservative estimate, and to give you an overview of the range of outcomes, I have also done a Monte Carlo simulation (below). I have predicted that revenues will grow in a range between 20% (0.2) to 60% (0.6) per year over the next 2 to 5 years.

Monte Carlo Simulation 1 (created by author Ben Alaimo)

Monte Carlo Simulation 2 (created by author Ben Alaimo)

Given these factors, I get a valuation range of between $ 8.43 in the slow growth scenario and up to $ 34 per share for the higher growth (best case) scenario. This gives me an average valuation of $ 18 / share, which means that the stock has an upside of about 80%.

Risks

Competition analysis

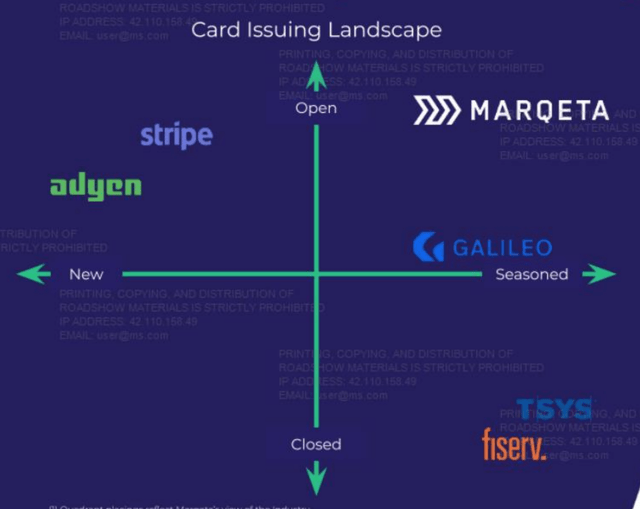

Marqeta has a best in class and user-friendly card issuance platform. However, they are not alone in the market. The company’s main competitor in the issuance of Open API cards is Galileo Financial Services, which was acquired in 2020 for 1.2 billion dollars by the Fintech giant SoFi. Although a smaller player than Marqeta, Galileo’s platform runs card programs with Robinhood (HOOD), Monzo (own, Paysafe, Transferwise (LSE: WISE) and even the European Fintech giant Revolut, which recently has a value of 33 billion dollars.

Other competitors include the payment giant Stripe (recently valued at a staggering $ 95 billion) and offer virtual card issues to customers such as Postmates. In addition, Holland-based Adyen (AMS: ADYEN) (OTCPK: ADYEY) often referred to as “PayPal of Europe” also offers card issuance. The good news for Marqeta is for the other companies, card issuance is just one product line, and thus they may not be as focused on gaining market share, which seems to be the case so far.

Competitors (Marqeta Investor presentation)

Square is their biggest customer

Square is Marqeta’s largest customer, with their Cash app card. This has been a blessing for Marqeta as far as they have ridden on the wave of increasing transaction volume in the cash tap. However, if Squares Cash App Card starts to decline in use or they decide to use alternative technology, there is a risk to the company, although there are no signs of this yet.

Consumption costs may decrease

The annual inflation rate in the United States accelerated to 8.6% in May 2022 and has consistently been much higher than the Fed’s target of 2% since early 2021. Inflation is pushing consumers with higher food, gas and electricity costs. The Ukraine-Russia war has only irritated rising energy costs and higher interest rates will make mortgages more an expense for households and reduce surplus incomes for consumers.

Economics 101 says higher costs equate to lower demand. Since many of these Fintech companies earn their revenue based on transaction volume, smaller volume equals less revenue. Although I think this is only a temporary problem (until inflation subsides), it is still a risk for all businesses.

Last thoughts

Marqeta is a fast-growing technology company, which has a best-in-class system for modern card issuers. Their platform already drives many Fintech disruptors, and they are set to continue to grow strong. The recent macroeconomic climate with high inflation and rising interest rates has lowered the valuation of all “growth stocks”. However, the stock is now undervalued in itself and thus looks like a large long-term investment and opportunity for Growth At A Reasonable Price (GARP).