Marathon Digital: Has the storm weathered? (MARA)

Adrian Vidal

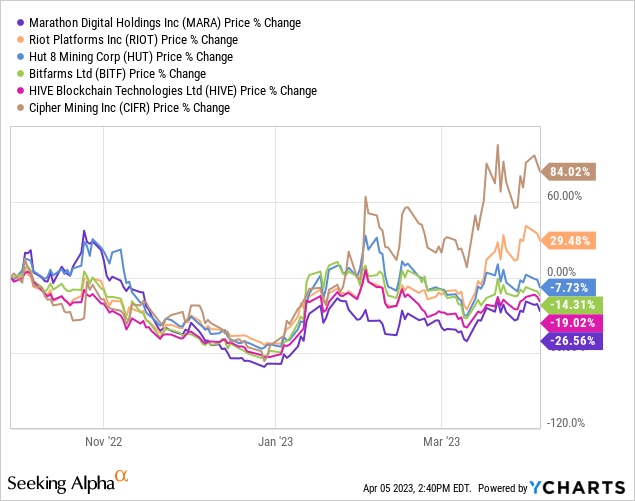

I last covered Marathon Digital (NASDAQ: MARA) at the end of September when the company’s share price was $10.77. The main takeaway from that article was both Marathon’s debt position and the company’s reliance on third parties would underperform peers. While MARA’s performance since that play certainly hasn’t been the worst of the public miners over the past two quarters, some of the names that I’ve liked more than MARA have actually outperformed:

Over the past six months, we’ve seen Riot Platforms (RIOT) transition to the point where they are now the industry leader in market capitalization. We’ve also seen a small degree of multiple expansion over the last couple of quarters in many of these names as well:

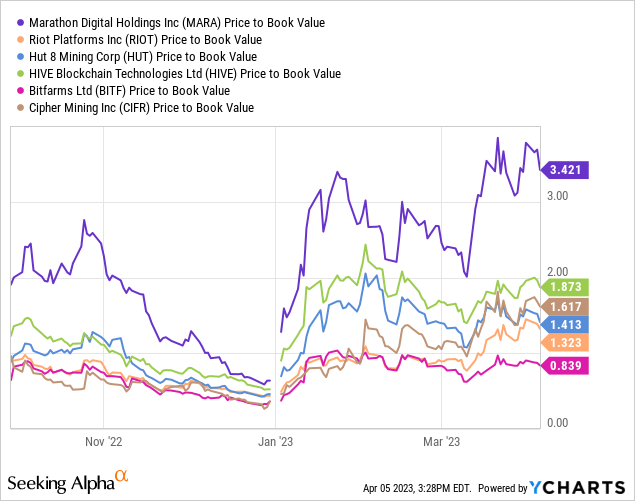

At the end of September, MARA traded at 1.7x book value and has since doubled to over 3x book. But again, this isn’t unique to Marathon Digital, as just about every company in the chart above has seen their price book multiples roughly double over the past 6 months.

The Bitcoin setup

It’s a very different fundamental setup now for many of these companies than it was just a few months ago. For example, the price of natural gas has come down again, which has helped put a temporary floor on mining profitability, even as the hash rate continues to hit new highs. Bitcoin (BTC-USD) itself benefiting from a banking crisis narrative that saw the price of BTC move from about $19,500 up to over $29,000 in about two weeks.

BTC daily (TradingView)

There are also positive signs technically. We are two months from a golden cross of the 50-day above the 200-day moving average, and both are still moving higher. We are four weeks away from a test and hold of the 200 day and BTC is now trying to break above resistance that could see it go well above $30k if this rally can continue. Positive signs can also be seen in some of Bitcoin’s valuation multiples.

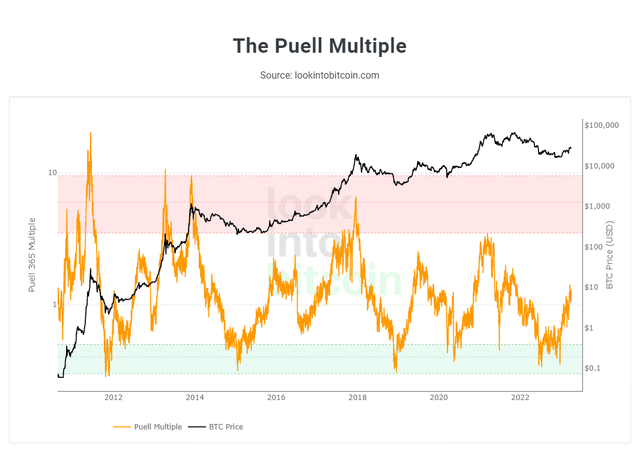

Look at Bitcoin

Bitcoin’s Puell Multiple is now well above 1 after being largely below 0.5 for the entire second half of 2022. In previous cycles, this type of activity in the Puell Multiple following deep sub-0.5 lows over an extended period has often indicated BTC the bottom is in and the next bull cycle is not far behind. If history repeats itself, Marathon Digital is well positioned to benefit.

Mars Production & HODL Stack

Purely from a Bitcoin treasury perspective, no public miner has more BTC on balance than Marathon, and very few miners come close to MARA in terms of EH/s mining capacity. Riot is close to 10.5 EH/s as of March. Only Core Scientific (OTCPK:CORZQ) has a larger mining operation, but that company is going through bankruptcy. Crypto Winter was harsh on these companies, and those that were overcharged were executed. I suspected that Marathon Digital could also be a potential crash, but I’m less convinced if the BTC low is actually in.

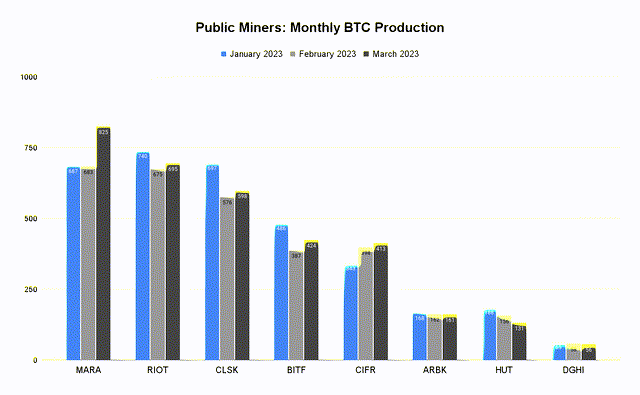

We’ve had the production numbers for March trickling in from the miners for the last few days, and by my count we have eight miners who have updated the numbers. So far, only two public miners have produced more BTC in March than in both January and February: Marathon Digital and Cipher Mining (CIFR):

Monthly BTC production (Company information)

These gains came largely from large increases in EH/s for both companies. MARA exploded higher from 9.5 to 11.5 and CIFR increased more modestly from 5.2 to 5.7. Riot Platforms, CleanSpark (CLSK) and Bitfarms (BITF) also increased EH/s, but to a lesser extent in percentage terms. MARA not only increased output better than peers last month, it also had one of the better months of overall BTC Treasury growth; add 74 BTC to your balance:

| February 2023 | March 2023 | Mon/Mon | % | |

| RIOT | 7,058 | 7,072 | 14 | 0.2% |

| MARA | 11,392 | 11,466 | 74 | 0.7% |

| COTTAGE | 9,242 | 9.133 | -109 | -1.2% |

| BITF | 405 | 435 | 30 | 7.4% |

| CLSK | 100 | 196 | 96 | 96.0% |

| ARBK | 101 | 85 | -16 | -15.8% |

| CIPHER | 465 | 427 | -38 | -8.2% |

Source: Company information

From my point of view, there is a clear mark from March, and that is Marathon Digital. It is the only company of the eight to have reported growth in both production during January and HODL stack during February.

Balance at the end of March (Marathon Digital)

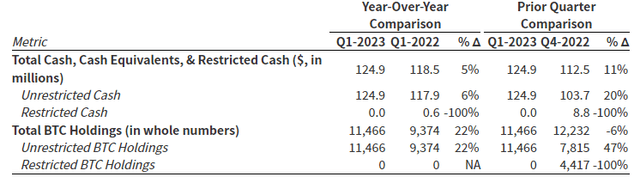

For Marathon, the stack is down 6% from the end of Q4, but what remains is now completely unencumbered after the company paid down $50 million in debt.

We exited the quarter with approximately $124.9 million in unrestricted cash and cash equivalents and 11,466 Bitcoin, whose market value was approximately $326.5 million on March 31.

These are positive signs from a company that still looks pretty rough on paper from a purely fundamental standpoint. But the fundamentals look a lot less bad if Bitcoin continues to rise from here.

Risks

Like many other miners, Marathon’s business was punished last year by a combination of margin squeezes, value declines and issues affecting third parties. Marathon lost a huge amount of money even after reducing stock-based compensation by over $136 million from 2021 to 2022. If Bitcoins If the price goes up, Marathon can conceivably get out of its debt position. But it’s still only an “if” and possibly a big if the Fed continues its rate hikes. Which is also another “if”, but that’s a topic for another article.

MARA common shares outstanding (Seeking Alpha)

Marathon had just under $125 million in cash at the end of March, and much of that came through shareholder dilution to end the year. Outstanding ordinary shares increased by approx. 25% from Q3 to Q4 after going from 116.8 million shares to 145.6 million common shares outstanding. A final risk to consider is the upcoming departure of the company’s CFO Hugh Gallagher, who is retiring in May.

Summary

There are more BTC miners who have healthier balances. But there are very few that have the combination of BTC stack and production capacity that Marathon has. Capacity that the company continues to scale through the rest of 2023. If you are looking for a simple Bitcoin proxy bet that will move up when Bitcoin moves up, MARA should do the trick and possibly to a greater degree than other mining companies that lack the ability to meaningfully scale BTC -holdings before the halving.

I still do not personally hold MARA shares and I do not plan to buy any at this time. But I think Marathon has shown encouraging signs in recent months. I would also like to disclose that I am a shareholder in Applied Digital (APLD). So I have indirect exposure to Marathon as it is Applied’s largest hosting client. There is still a very large short position in this name. While I’m not buying MARA over RIOT, I don’t see Marathon as a sell anymore.