Iris Energy: Winning the race against time? (IREN)

Just_Super

Iris Energy (NASDAQ:IREN) is a Bitcoin (BTC-USD) mining stock that I have covered in the past on three different occasions:

For a more in-depth look at my thoughts on Iris, I encourage you to read each of the previous articles.

Short summary

Iris attempted an aggressive scaling of BTC production capacity last year and quickly grew from 0.9 EH/si in April to 3.9 EH/si in late October. The problem the company ran into was that the scaling attempt essentially came at the worst possible time when BTC’s price fell dramatically following the collapses of Terra Luna (LUNC-USD), Celsius (CEL-USD) and FTX (FTT-USD). Arguably making matters worse for many in the Bitcoin mining community was an increase in electricity costs that crushed mining operations profitability and pushed many over-leveraged miners into insolvency.

While I think many would agree that Iris did a better job of managing its balance sheet than certain mining companies, the loss of machines that were secured through special vehicles put Iris back to square one and without any BTC in its coffers due to the company’s production winding down strategy . With about a year to go until the next Bitcoin halving, mining companies are running out of time to acquire as much BTC as possible before the block reward is cut from 6 BTC down to 3.

Iris updates

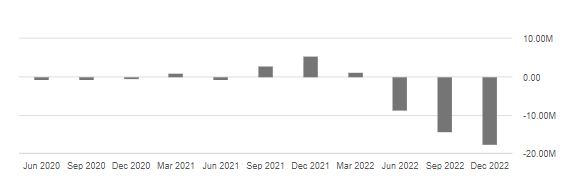

In February, Iris reported $13.8 million in revenue for the 2nd quarter of fiscal 2023. This was a 15% quarter-on-quarter revenue decline that the company attributed to falling Bitcoin prices and the reduced number of Bitcoins mined during the period. This was combined with increases in electricity, land and business costs resulting in $17.7 million in negative operating income for the quarter:

Operating income (Seeking Alpha)

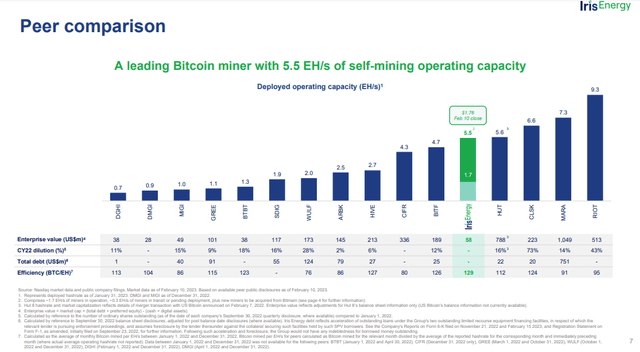

Earlier this month, Iris revealed 156 BTC mined and 1.7 EH/s of operational capacity from its February production update. Shortly after that production update in February, Iris announced that the company has begun installing additional machine deliveries that will ultimately take the company’s operating exahash from 1.7 EH/s to 5.5 EH/s. Most of them will be online soon:

160MW of data center infrastructure (supporting ~4.9 EH/s) is available immediately, with commissioning of the first 20MW at Childress (supporting the remaining ~0.6 EH/s) in the coming months.

If Iris is able to execute on bringing these machines online, it will make the company a top 5 public miner by monthly production capacity:

Production guidance (Iris Energy)

Note that this slide does not include Core Scientific (OTCPK:CORZQ) which still had the largest mining capacity in February but is now going bankrupt.

Revenue modeling

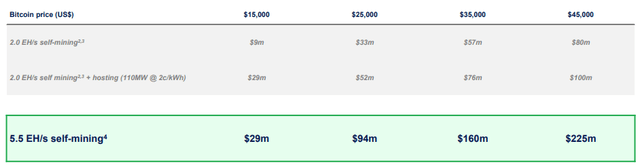

Aside from energy costs, Bitcoin prices, and potential regulatory risk that comes from mining in crypto-unfriendly jurisdictions, the major headwind shared by all of these public miners is the block reward halving that is about a year away. If Iris can execute scaling goals and achieve 5.5 EH/si Q2, the company projects annual revenue generation of $94 million at a $25k BTC price:

Income projection (Iris Energy)

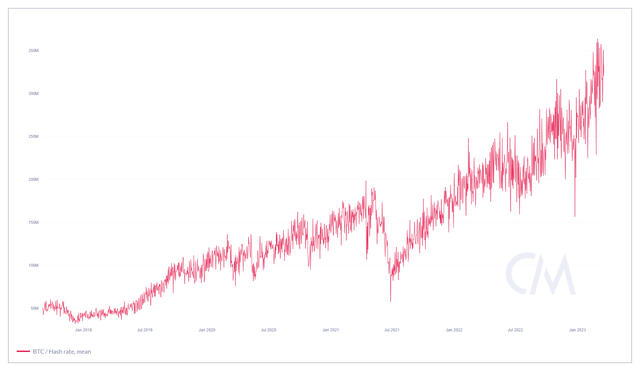

So far in 2023, Iris has generated 328 Bitcoin at an average EH/s of 1.6. At the company’s current BTC per EH/s levels, 5.5 EH/s per second could generate just under 568 BTC per month, assuming the global hash rate remains at levels similar to where they have been for the past two months.

Global Bitcoin Hash Rate (CoinMetrics)

However, this is not a sure thing as I expect the global hash rate to likely continue the broad trend higher. To estimate Iris’ turnover at full capacity of 5.5 EH/s, an additional effort is required; how much BTC Iris can mine per exahash. Over the past 12 months, the company’s BTC per EH/s has varied significantly, but has generally been somewhere between 115 and 130. Given the current global hash rate trend and the increasing Bitcoin price that will possibly bring more miners back on net, d take a more cautious view when considering BTC per EH/s expectations:

| Monthly income from 5.5 EH/s BTC production | |||||

| Bitcoin price | |||||

| BTC per EH/s | $20,000 | $25,000 | $30,000 | $35,000 | $40,000 |

| 85 | $9,350,000 | $11,687,500 | $14,025,000 | $16,362,500 | $18,700,000 |

| 90 | $9,900,000 | $12,375,000 | $14,850,000 | $17,325,000 | $19,800,000 |

| 95 | $10,450,000 | $13,062,500 | $15,675,000 | $18,287,500 | $20,900,000 |

| 100 | $11,000,000 | $13,750,000 | $16,500,000 | $19,250,000 | $22,000,000 |

| 105 | $11,550,000 | $14,437,500 | $17,325,000 | $20,212,500 | $23,100,000 |

| 110 | $12,100,000 | $15,125,000 | $18,150,000 | $21,175,000 | $24,200,000 |

Source: author projections

If we assign a base case of 90 EH/s to a $30k BTC price, Iris is looking at roughly $14.9 million in monthly revenue, or $44.6 million per quarter if the company continues to sell production. Measured in Bitcoin, this base guess could generate 1,485 BTC per quarter if the company decides to switch to a HODL strategy at any point before the halving.

Main takeaway

Although Iris has been very clear about winding down production to fund its operations, the company may at some point reconsider this approach before the Bitcoin halving next year. When the block reward is cut, mining revenue will drop dramatically unless the price of BTC increases significantly. If that happens, it will claim companies like Iris Energy to have some BTC in their treasury that they can sell after halving.

At current EH/s levels, Iris is unlikely to be able to scale a HODL stack comparable to companies like Riot Platforms (RIOT) or HIVE Blockchain (HIVE) if it chooses to pivot balance management in anticipation of the halving . But even in the event that it doesn’t pivot its financial management strategy, Iris stock should benefit greatly from the production expansion in the coming months if it can meet its timelines.