How has Fintech impacted unbanked populations?

In recent years, fintech has emerged as a powerful force in the financial sector. But what does it mean for populations traditionally excluded from formal financial services?

In this blog post, inspired by Oxford’s Fintech programme, we will explore the impact of fintech on unbanked populations, how fintech for unbanked populations has evolved, and the pros and cons of fintech solutions now and in the future.

The impact of fintech on financial inclusion

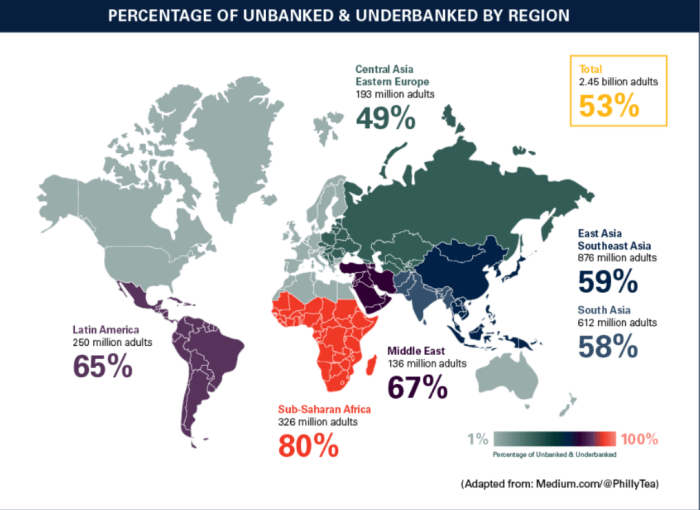

In both emerging markets – particularly Africa, Asia and South America – and existing markets, reliable mobile wireless access has helped unbanked populations gain access to financial tools and services. As the Global Findex Database 2017 reports (Demirgüç-Kunt et al., 2018):

1.2 billion adults have acquired an account since 2011, including 515 million since 2014. Between 2014 and 2017, the proportion of adults who have an account at a financial institution or through a mobile money service rose from 62 percent to 69 percent globally. In developing economies, the proportion rose from 54 per cent to 63 per cent.

Join Oxford’s Fintech program today

Develop a network of professionals pioneering financially inclusive solutions in Oxford’s Fintech programme, powered by Esme Learning. Don’t miss out – registration closes on 31 January 2023.

How has fintech for unbanked populations evolved?

In the early 2000s, when countries like the Philippines and Kenya first started launching mobile payments, fintech faced a number of barriers. Governments were concerned about consumer protection and competition, big banks often used their influence to block fintech-friendly policies, and regulators didn’t know how to address mobile solutions.

Since the early 2000s, however, hundreds of millions of previously unbanked adults have opened accounts for the first time. Many have specifically opened accounts to receive digital salary payments or government transfers. In Thailand, nearly one in five adults banked their first account to receive government benefits. In Georgia, Uzbekistan and Kazakhstan, this figure was even higher – close to 30 percent.

Now, mobile money accounts have spread from East Africa to West Africa and beyond, dramatically increasing the proportion of adults using digital payments. In some countries where mobile money is widespread, such as Kenya, more than 90 percent of account holders make digital payments.

Fintech’s benefits for unbanked populations

For historically unbanked populations, fintech can help provide more convenient and affordable access to the global financial system. With fintech apps and services, unbanked adults can get:

- Easy access to financial services. Mobile banking apps allow users to transact without visiting a physical bank branch. Apps can help unbanked adults manage their finances without taking the time or money to travel to a long-distance bank.

- Emergency funds. During Covid-19, governments used digital financial services to spread fast and secure payments to citizens and businesses in Peru, Zambia, Uganda and Namibia (Agur et al., 2020). Likewise, fintech can help unbanked individuals quickly raise money from family and friends in a crisis.

- Improved administrative services. Fintech can digitize public salaries, pensions and social transfer payments, helping governments like Mexico save upwards of $1.3 billion per year. Clear online transactions can also help reduce costly errors, overpayments and government corruption, channeling money back into vital public services.

- New opportunities for small businesses. Peer-to-peer fintech platforms can make it easy to send and receive money without going through a traditional financial institution. Crowdfunding platforms help low-income entrepreneurs launch startups, projects and platforms with the help of a wider global community.

Fintech’s disadvantages

Despite fintech’s benefits, unbanked adults remain vulnerable to being exploited or excluded from critical services. When using fintech solutions, they often face risks similar to those they may face in the formal financial system:

- Predatory lending. As discussed in Oxford’s Fintech programme, unbanked individuals often lack access to strong consumer protection laws. Companies can offer expensive loans via mobile phones, leaving unbanked individuals struggling to pay off their loan balances and getting heavily in debt.

- Expensive prices. While some fintech offerings are free or low-cost, others may charge higher lending or payment fees. These higher rates can be written into disclaimers and go unnoticed until the payments are prohibitive.

- UX design flaws. Many fintech products are designed for people who are already comfortable with technology. Poorly designed interfaces or system architectures can deter those unfamiliar with computers and smartphones and make transactions impossible to complete.

Build fintech solutions for unbanked populations

Do you want to build fintech solutions for unbanked populations? Esme Learning designs and develops management education programs in collaboration with leading universities and companies from all over the world. Browse our full list of programs in Artificial Intelligence, Blockchain, Cybersecurity, Digital Disruption and Digital Finance at https://esmelearning.com/collections/all.