How big is the alt bubble? – Bitcoin Magazine

Below is an excerpt from a recent issue of Bitcoin Magazine Pro, Bitcoin Magazine premium market’s newsletter. To be among the first to receive this insight and other market analysis on the bitcoin chain straight to your inbox, Subscribe now.

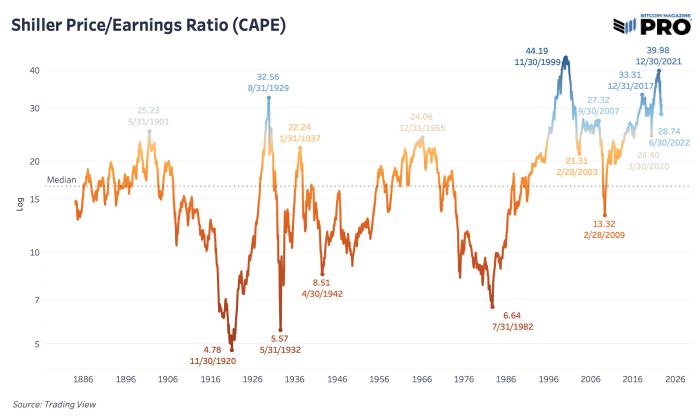

Shiller P/E ratio

Much of our commentary since the inception of Bitcoin Magazine Pro has been in relation to the relationship between bitcoin and stocks, and their reflection of the global “liquidity tide.” As we’ve previously discussed, given that the size of the bitcoin market relative to US stocks is minuscule (the current market cap of US stocks is roughly $41.5 trillion, compared to $452 billion for bitcoin). Given the trending market correlation between the two, it’s useful to ask exactly how over/undervalued stocks compare to historical values.

One of the best ways to analyze when the broader stock market is overvalued is the Shiller price-to-earnings (PE) ratio. Also known as the cyclically-adjusted PE ratio (CAPE), the calculation is based on inflation-adjusted earnings from the last 10 years. Through decades of history and cycles, it has been the key to show when prices in the market are far overvalued or undervalued relative to history. The median value of 16.60 over the last 140 years shows that prices in relation to earnings always find a way to go back. For share investments, where the return on the investment is necessarily dependent on future earnings, price you pay for said income is of utmost importance.

We are at one of those unique points in history where valuations have risen just shy of their 1999 highs and the “alt bubble” has begun to show signs of bursting. Still, with all comparisons to past bubbles bursting, we’re only eight months down the road. Despite the rally we’ve seen in recent months and the explosive inflation surprise upside move that came today, this is a signal about the broader market picture that’s hard to ignore.

Although the release of consumer price index data came in at a surprising 0.0% month-over-month reading, year-over-year inflation is at a distasteful 8.7% in the US. Even if inflation were to decline completely for the rest of the year, 2022 would still have experienced over 6% inflation during the year. The key here is that the cost of capital (Treasury interest rates) is adjusting to this new world, with inflation at its highest in 40 years, yields rising to record highs and pulling down multiples in stocks as a result.

If we think about the potential paths forward, with inflation being fought by the Federal Reserve with tightening policy, there is the potential for stagflation in the form of negative real growth, while the labor market turns.

Looking at the relative valuation levels of US stocks in past periods of high inflation and/or sustained financial repression, it is clear that stocks are still priced close to perfection in real terms (inflation-adjusted 10-year earnings). Since we believe continued economic repression is an absolute necessity as long as debt remains above productivity levels (US public debt to GDP > 100%), stocks still look quite expensive in real terms.

Either US stock values are no longer tied to reality (unlikely), or:

- US stock markets are crashing in nominal terms to lower multiples relative to the historical average/median

- US stocks melt in nominal terms due to persistently high inflation, yet fall in real terms, bleeding investors’ purchasing power

The bottom line is that global investors are likely to increasingly seek an asset to park their purchasing power that can escape both the negative real interest rates in the fixed income market and the high earnings multiples (and subsequently low or negative real interest rates).

In a world where both bond and stock returns are lower than annual inflation, where do investors park their wealth, and what do they use to perform financial calculations?

Our long term answer is simple, just check the name of our publication.