Galaxy Digital Stock: Emerging Stronger After Crypto Reset

solar seven

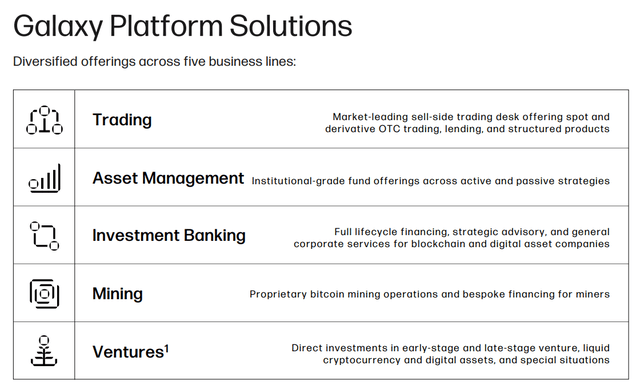

Galaxy Digital Holdings Ltd. (OTCPK:BRPHF) is a leading financial services provider in digital assets and blockchain technologies. The company captured the massive growth in the area in recent years across a diversified business that includes trading, asset management and investment Banking operations. While 2021 was a record year for the company, the recent environment has been defined by the sharp correction in crypto and broader macro headwinds. Galaxy Digital shares are down more than 70% in the past year, underscoring the extreme volatility.

We last covered the stock back in 2021 with an optimistic view, while noting that cryptocurrency trends were the main risk to consider. Much has happened during the period, and we reiterate a positive long-term outlook, recognizing some reset expectations. The key to recognize is that capabilities in Web3 such as payments, Defi and metaverse are still in the early stages of adoption. Galaxy Digital can benefit from themes that go beyond any single cryptocurrency. A planned US listing on Nasdaq compared to the current primary trading on the Toronto Stock Exchange could be positive for the stock going forward.

The company IR

Galaxy Digital Key Metrics

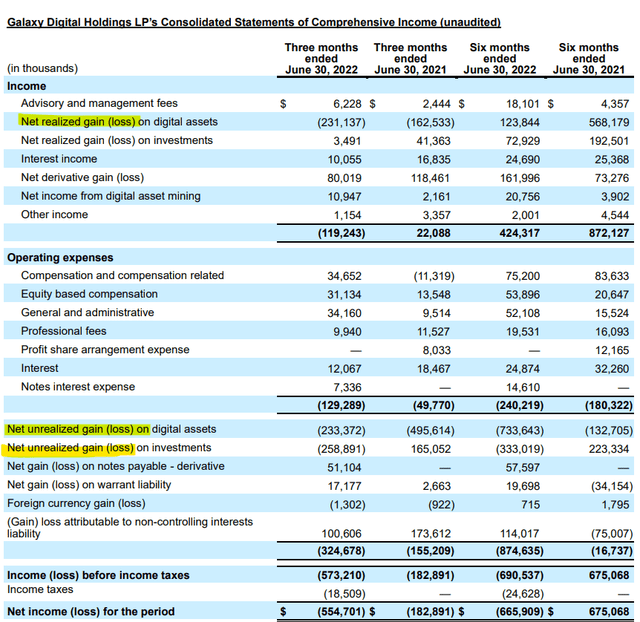

The company last reported results for the second quarter in August, with a net loss of -$555 million. The context here addresses the deep selloff in related cryptocurrencies and the value of over 215 portfolio companies. The company’s digital assets and investments were reduced by -492 million dollars on a net unrealized basis.

There was an additional -$231 million in realized losses from digital assets during the quarter related to trading in Bitcoin (BTC-USD) and Ether (ETH-USD). The company also had some exposure to “Terra Ecosystem” (LUNC-USD) which collapsed during Q2 and created some contagion effects to other parts of the crypto market. On this point, CEO Mike Novogratz noted during the conference call that the crash was working to accelerate a needed deleveraging across the sector in Q2, with liquidations leading to a better sense of stability into Q3 compared to fear and uncertainty back in May.

The company IR

Elsewhere from the results, there were some strong points. Core advisory and administration fees reached $6.2 million, up from $2.4 million in the year-ago period. Galaxy Digital has also moved forward with its proprietary Bitcoin and digital asset mining which generated net income of $10.9 million in Q2 compared to just $2.2 million in Q2 2021.

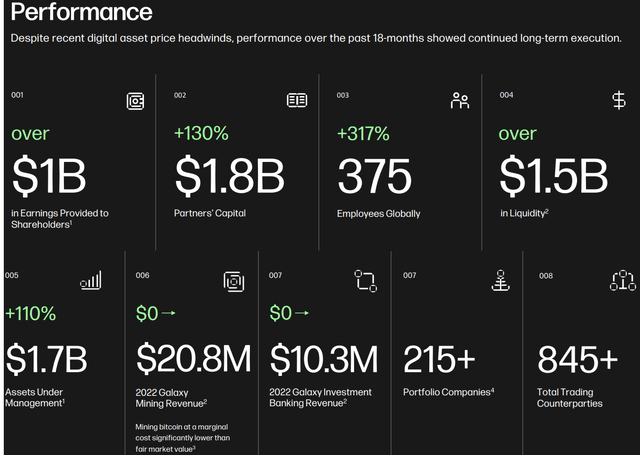

The company focuses on the results of the last 18 months, which confirms the transformation of the operation over the period. Asset Management AUM of $1.7 billion, up 110% based on momentum from multiple fund products and investment vehicles. Partners’ capital, effectively the company’s net equity under the current structure, of $1.8 billion has increased 130% compared to the end of 2020. The company ended the quarter with over $1.5 billion in liquidity, including over $1.0 billion in cash compared to $425 million in long-term notes.

The company IR

Canceled BitGo acquisition

An important development came in August when Galaxy Digital announced it was closing its planned acquisition of BitGo, an institutional provider of digital assets. The original $1.2 billion cash-and-stock deal disclosed in March was expected to generate synergies by adding additional businesses and complementing Galaxy’s current offerings. Fast forward, BitGo allegedly failed to submit an audited annual report for 2021 by July 31, which was cited by Galaxy as a breach of the agreement.

There is some controversy because reports suggest that BitGo is attempting to sue Galaxy for $100 million as an “improper rejection” of the merger. CEO Mike Novogratz already claims the lawsuit is unfair and plans to defend the company in court. The first point to cover is that if the allegations are true, Galaxy Digital appears to have a strong case to walk away from the deal, as BitGo simply failed to comply with a basic regulatory requirement.

In our view, the termination ends up being positive for Galaxy considering that the timing of the original terms from March in Q1 was reached during a high price environment for the crypto market. In other words, if it wins the lawsuit, Galaxy may have simply gotten lucky with the opportunity to walk away from a major deal that was undermined after the market selloff in the second quarter.

It remains to be seen how the lawsuit from BitGo progresses, although the upside is that Galaxy Digital can now enter 2023 with a stronger balance sheet and presumably some room to seek out new deals at attractive prices.

What’s next for Galaxy Digital?

The key takeaway from delving into Galaxy Digital’s financials is that by getting past the quarterly volatility in asset prices, the underlying financial group is profitable with ongoing growth opportunities. While there are parts of the business that are correlated to cryptocurrency price trends, the stock’s real attraction is its broader diversification into related blockchain technologies.

Among venture capital portfolio companies, exciting startups and emerging players are uniquely positioned to take advantage of the market shake-up to consolidate their leadership in Web3 services and solutions. It remains possible that one of these investments develops into a major global company in the next five to ten years as a windfall for Galaxy Digital shareholders.

The company IR

The benefit from the large losses in Q2 and the sale of the stock is to consider that the digital asset/crypto market has at least stabilized into Q3. For reference, the current price of BTC at around $19,000 is only slightly below the level at the end of Q2 on June 30 at $19,500. Other cryptocurrencies such as ETH have outperformed with a strong decline.

This means that assuming the “crypto winter” has already run its course, there is a case to be made that the correction in Galaxy Digital shares has more than priced in some of the worst case scenarios through a valuation reset.

In the near term, a sustained rally in the BRPHF will likely need the challenging macro setup to cooperate. We can look forward to confirmation that inflation has peaked globally in the coming months, potentially opening the door to a resurgence in global growth expectations. Crypto is a side of “technology” that we believe can lead higher. From there, Galaxy Digital is the type of high-beta momentum name that could transition to the upside.

A rise in the leading cryptocurrencies can add volume to trading activity as a positive for operational and financial calculations. We want to see BTC make a move above $25k as the first level of technical resistance to support a more sustained rally in the sector. On the other hand, all eyes must be on the quarterly low for Bitcoin as it briefly traded below $18,000 as a measure of sector sentiment. A return to that level is likely to put BRPHF’s $3.59 cycle low back into play as a downside risk.

Seeking Alpha

Final thoughts

A solid balance sheet combined with a best-in-class asset management platform keeps Galaxy Digital interesting. While the events of the past year have included several surprises, we argue that the company has weathered the storm and is poised to emerge stronger. Going into the quarterly results expected sometime in November, key points to watch will be trends in core fee-based advisory and asset management business along with cash flow trends. We want to see operating costs controlled with some effort to focus on profitability.

In our view, the stock could trade higher through 2023 in a scenario where the crypto sector picks up and blockchain technologies gain momentum. An update from management regarding the progress of the reorganization into a US Delaware incorporated company along with a timetable for the Nasdaq listing could support a structurally higher valuation multiple for the stock as an upside catalyst.