Forget Crypto, NFTs, Sucker Yields and Value Traps…Buy these REITs instead

anilaccum

When most people say, “I hate to say, ‘I told you so,'” let’s face it…

They don’t really mean it. They are actually happy to get “Nayah, nayah, nayah, I was right and you were wrong” in.

It really is disgusting.

I say that as someone who has been on the receiving end of the shock and on the self-righteous side. (Don’t all parents have?) But in this case, there is no complacency involved. I really hope you listened to me when I said to avoid:

- Cryptocurrencies

- Non-fungible tokens, or NFTs

- Suger gives in

- Value traps

I know they all have their individual and collective appeals – from the fear of missing out (“FOMO”) to wanting to be one of the cool kids to the lure of quick wins. I’ve fallen for this sort of thing before, and that may be why I’m not going to say, “I told you so.”

Been there. Done that. Felt the pain.

In fact, it was experience with such get-rich-quick, feel-good-in-the-moment schemes that made me where I am today. That is why I have made it my life’s mission to steer others away from such fates.

So trust me when I say I’m not happy when I point out that I told you to avoid these assets. For those who followed, hopefully this will inspire you to continue investing wisely.

And for those who didn’t, hopefully this will help you avoid such mistakes in the future.

Here is my overview of cryptocurrencies and NFTs

It has been a while since I dedicated an article to cryptocurrencies. Maybe it’s because they’ve lost a lot of luster since last June.

I think that’s when my son – who is very intelligent but very much part of Gen Z – largely tried to convince me that crypto and NFTs were a worthwhile venture. If so, he really did a good job of presenting his case.

That’s how I came to write “Crypto Today Seems Like REITs in the 1970s” the other day. It contained these summary points:

- “Just because Bitcoin is 13 years old doesn’t mean it’s established.”

- “In 1968, big banks began to realize that they could use the REIT structure to lend money to companies that build commercial real estate. Their stocks fell and fell hard – 21.8% in 1973 and 29.3% in 1974.”

- “Remember I grew up watching Star Trek in the 1970s… So I’m well aware that “innovation is the ability to see change as an opportunity – not a threat.”

In other words, I could see the potential of the asset class. But it remained too unestablished to be free of crooks and lunatics.

I’m even less willing to give cryptocurrency the benefit of the doubt. You can get the gist of my thoughts on that from my November 2021 article, “Become an NFT Landlord and Sleep Well at Night.”

Contrary to what the title suggests, I had an entire segment titled,

“Explaining NFTs and why I object to them.”

I learned the hard way

The next segment was “A Personal Story About an NFT Equivalent (Back in My Day).” It told the story of when:

“I thought I was a real estate mogul, renting out jets and taking fancy vacations to luxury resorts.

“I made a lot of money from the buildings I built – and used them all too often just as quickly. There were far too many benefits I enjoyed on funds that should have been invested wisely instead…

“For example, I sold a shopping center in 2004, which gave me about $400,000 to put in the bank. I soon used about $250,000 of that to buy up a franchised Athlete’s Foot location. And another $92,000 went to buy a diamond ring for my wife.”

I have not examined any of them.

As such, I can’t take credit for the fact that the diamond ring actually ended up being a worthwhile investment (worth over $250ki today). It was pure luck.

Athlete’s Foot, meanwhile, is “virtually defunct in the United States today.” My stores definitely are and so is the $250,000 investment.

As I said at the beginning, that’s why I’m so risk averse today. It’s not that I’m unwilling to dare.

I can be as bold as the next guy, believe it or not. If I could reveal details about the projects I am working on today, you would easily recognize it.

But that boldness must be supported by brains.

This means you don’t have to buy into suck returns, value traps or newfangled notions without knowing about them first.

2 buy with high conviction

Yesterday I spoke to a group of high net worth investors and I told them that I consider now the best time of my life to own real estate investment trusts (“REITs”).

These friends are all sophisticated investors who have built incredible wealth investing in private real estate, and I told them that:

“I’ve lived through several recessions and a global pandemic, and given what I’m seeing right now, you should load up on publicly traded REITs.”

I went on to say that:

“Mr. Market completely ignores the fact that REITs grow earnings and dividends, and while there are certainly risks associated with inflation and rising rates, most higher-quality REITs have stress-tested these forces and are well positioned to generate reliable dividend growth for years to come.”

Personally, I am taking advantage of the mispricing and increasing my exposure to REITs, recognizing that I have the potential to accelerate my retirement plans.

I am now in the best shape I have ever been in my entire life – physically, mentally and financially – and the next year or two could provide meaningful fuel for my eventual retirement.

Here are some REITs I buy…

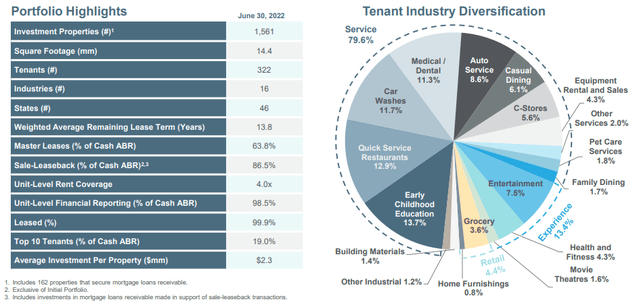

Essential Properties Realty Trust, Inc. (EPRT) is a net rental REIT that has a portfolio of 1,572 freestanding properties (14.8 million square feet) in 48 states. The diversified portfolio is leased to tenants in businesses such as restaurants (including quick service, casual dining and family dining), car washes, car services, medical services, convenience stores, entertainment, health and fitness and early childhood education.

EPRT Investor Relations

The healthy portfolio is 100% occupied with a weighted average embedded escalator of 1.5% per annum with solid coverage: unit level coverage of 4.2x with 99% of ABR required to report flat P&L levels.

EPRT’s balance sheet is positioned to fund external growth opportunities as the company maintains low leverage: Net Debt/Annualized EBITDAr of 4.4x, and a weighted average debt maturity of 5.7 years.

In Q3-22, EPRT generated adjusted funds from operations (“AFFO”) per share of $0.38, an increase of 15% compared to Q3-21. Over the nine-month period, AFFO was $1.15 per share on a fully diluted per share basis, which is a 19% increase over the same period in 2021.

EPRT maintained its 2022 AFFO per share guidance range of $1.52 to $1.54, implying a 14% year-over-year growth rate at the midpoint.

EPRT Investor Relations

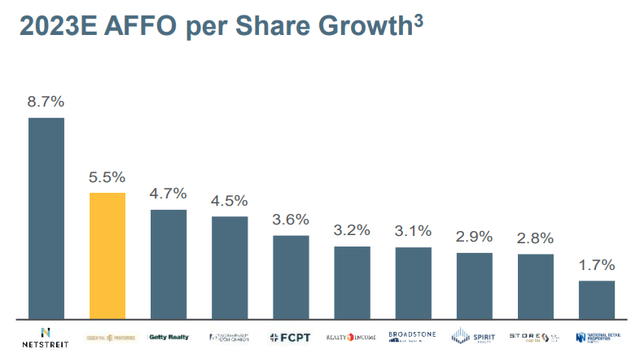

The company issued 2023 AFFO per share guidance in a range of $1.58 to $1.64, implying growth of 3% to 7% at the low and high ends of the range, relative to the midpoint of 2022 AFFO guidance per share.

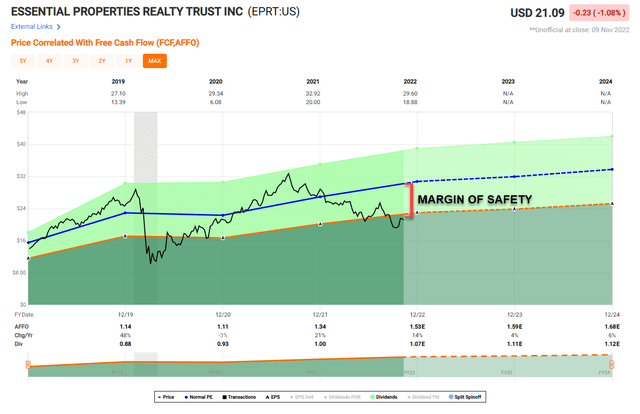

As shown below, EPRT is trading with a wide margin of safety – based on today’s price of $21.09 and P/AFFO of 14.0x. Normal P/AFFO is 20.1x and the current dividend yield is 5.1%. The payout ratio is just 70%, and iREIT believes shares could reach $28.00 by the end of 2023, which equates to a 30%+ annual return.

FAST graphs

Extra Space Storage Inc. (EXR) is another high-quality REIT we’re buying right now.

The Salt Lake City-based REIT is a member of the S&P 500 and owns and/or operates over 2,000 self-storage properties (1,009 owned, 304 JV and 864 managed), comprising approximately 1.5 million units and approximately 164 million square feet. of rentable storage space.

EXR is the second largest owner and/or operator of self-storage properties in the United States and is the largest self-storage management company. It is considered a best-in-class operator and has earned a reputation as a technology leader in the REIT sector. You can now find Extra Space stores in over 1,000 cities across the United States

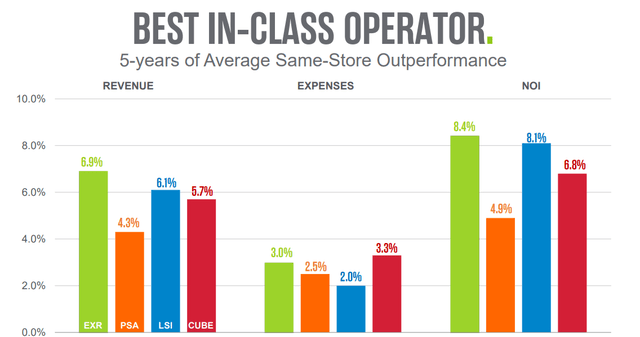

Over the past five years, EXR has outperformed its peers, as shown below:

EPRT Investor Relations

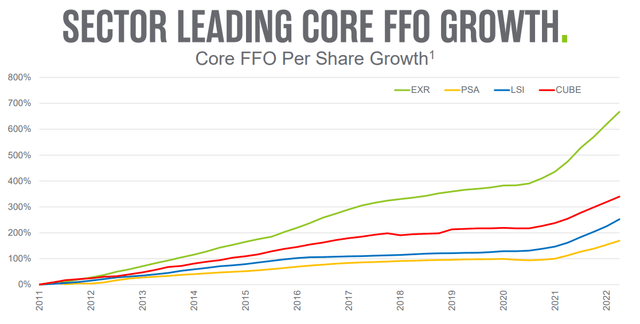

Importantly, EXR has excelled in generating the strongest FFO per share growth:

EPRT Investor Relations

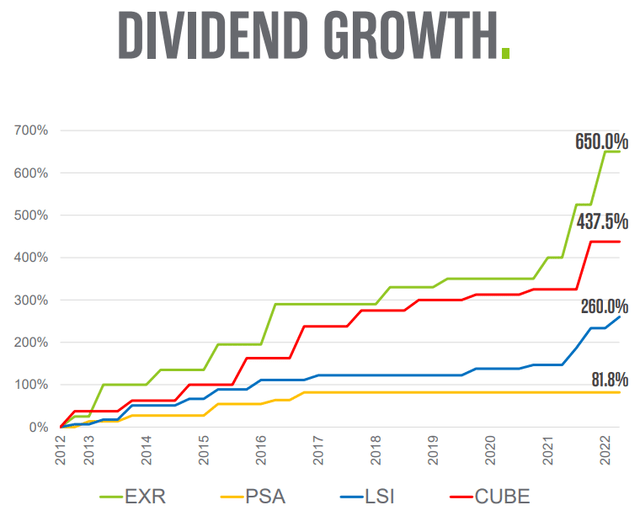

Of course, this has led to best-in-class dividend growth:

EPRT Investor Relations

In Q3-22, EXR posted strong same-store revenue growth of 15.5%, driven by strong rent growth, partially offset by lower year-over-year occupancy. Spend pressure across many items resulted in total same-store spend growth of 12.6% and same-store NOI growth of 16.4%.

This strong real estate NOI plus external growth efforts resulted in core FFO growth of 19.5% (includes an addition of $0.05 per share for estimated property damage and renters insurance claims related to Hurricane Ian).

EXR’s 2022 implied same-store revenue growth is the highest in the company’s history, and this is on the back of 2021, which was the company’s second-highest revenue growth year. The implied FFO growth in 2022 at the midpoint is 21%.

EXR also has a solid balance sheet, with net debt to EBITDA of 4.6x at the end of the quarter. The company increased its acquisition investment guidance to $1.65 billion, all of which are closed or under contract.

EXR tightened its core FFO range, which is now estimated to be between $8.30 and $8.40 per share, an implied increase of about 21% year-over-year.

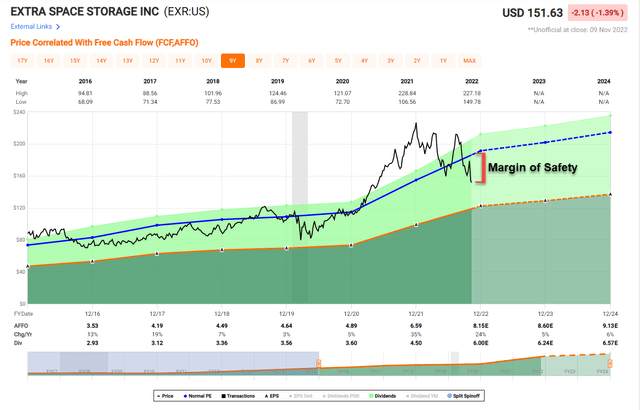

As shown below, EXR is also trading with a wide margin of safety – shares closed at $151.63 with a P/AFFO of 19.1x. The normal (P/AFFO) multiple is 23.5x, and the current dividend yield is 4.0%.

Given the pullback in pricing, we’ve become more fixated on this self-storage REIT, which has delivered on its “wide moat” scale and capital cost advantages. We target shares to return ~25% over the next 12 months ($19.82 by end-2023).

FAST graphs

In Conclusion…

Remember folks, earnings generate dividends, and dividends generate returns.

It’s that simple.

I wish I knew that secret 30 years ago, and if I did, I wouldn’t be writing this article right now.

Instead, I would live early retirement somewhere, maybe in Paris or Barcelona (I’ll be there in a few weeks).

PS: Possibly Portugal too (hoping to visit my friend and subscriber, Eric).

The good news is that I know how to invest now, and I’m happy to share my wisdom with you here at Seeking Alpha. My friend and fellow contributor Chuck Carnevale sums it up nicely,

“…if the long-term ownership of large businesses appeals to you as an investor, you should focus on where and how your returns will be generated. To me, common sense suggests that long-term performance will be functionally related to the success of the business in which it is invested . At the end of the day, often referred to as the bottom line, total return comes down to how profitable the business you choose is and how fast it grows over time.”

And…

“If the company pays a dividend, your investment will contain both a capital growth and an income component. If the company does not pay a dividend, you as an investor will rely solely on capital growth for your total return. In either case, the valuation at purchase will greatly affect your long-term total return.”