Fintech Titan is cheap as analysts trim targets

Despite Mastercard (MA) is delivering solid first-quarter results, and broader market forces have enticed Wall Street analysts to lower their price targets. However, such target downgrades have been fairly mild, as analysts still have a favorable view of the company. I am bullish on MA stock.

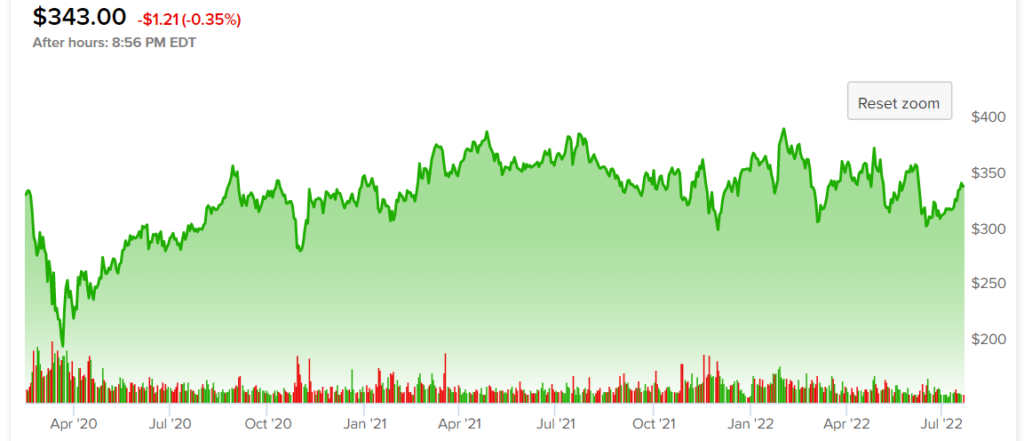

Shares in Mastercard have been under pressure for two and a half years, with shares trading around February 2020 levels.

Sure, the coming economic storm clouds could weigh on consumer spending. A consumer-facing recession does not bode well for any company, especially those looking to cut back on credit purchases. Still, as digital payments continue to take the place of cash payments, Mastercard has a strong long-term tailwind at its back.

Mastercard’s technical know-how is easy for investors to overlook

The emergence of new financial technologies, such as those offered by Apple (AAPL) Cards, can further accelerate the move away from cash. Given that this transition is far from over, especially in emerging markets, it’s really hard to dismiss Mastercard as it looks to leverage technologies to outgrow its big brother Visa (V).

As outlined by the firm’s recent investor day, commerce, ESG and technology remain Mastercard’s three pillars of growth. The technology pillar, I think, is the most exciting and could allow Mastercard stock to command a much higher multiple.

It’s been a bit of a rollercoaster ride for stocks in MA this year. Still, the stock has outperformed the market, now down just 14% from its peak in 2021.

In fact, the ultimate goal of any credit card company is to displace cash. As consumers embrace convenient digital payments, cash may be on the way out without firms like Mastercard innovating further. Either way, Mastercard has its foot on the pedal, with exposure to emerging technologies such as artificial intelligence, cyber security and even digital currencies.

Mastercard could be a sneaky blockchain play

Mastercard’s president of data services Raj Seshadri recently noted the many potential uses of blockchain technology, noting that there are “many fascinating blockchain applications that have nothing to do with crypto.”

As the euphoria surrounding cryptocurrencies and blockchain begins to fade, Mastercard will likely be watching to see where they can incorporate blockchain technologies. Digital currencies and improved security are just two benefits of blockchain infrastructure.

While Mastercard isn’t your typical fintech stock, I think the firm is more than capable of out-innovating its smaller rivals, especially as rates rise and credit becomes harder to come by.

For now, it is difficult to gauge how blockchain technologies will shape our future. When it comes to cryptocurrencies there is a lot of smoke and mirrors. As the hype dies down, we will gradually see established firms like Mastercard embrace the nascent technology. For now, it’s a wild card for payment giants like Mastercard, but not one to be ignored.

The blockchain remains an abstract concept for many. However, it may be easier to see the technology and its applications as akin to the metaverse. It’s an exciting frontier that exists today, but it may be years before corporate America can fully embrace it.

Mastercard is a growth stock with a modest multiple

Mastercard stock has never been dirt cheap, but it doesn’t deserve to be, given its outstanding growth profile. At the time of writing, MA stock trades at 16.9 times sales and 35.5 times trailing earnings, which are below their five-year historical average multiples of 17.9 and 43.2, respectively.

Yes, there are headwinds ahead as economic growth is challenged by interest rate hikes. But if there’s one company that can emerge from the other side of the recession in a position of strength, it’s Mastercard.

For the most part, Wall Street is a raging bull on Mastercard stock amid the mild decline, and it’s not hard to see why, as the firm looks to be closing the gap with Visa.

Wall Street’s Take on Mastercard

As for Wall Street, Mastercard has a strong buy consensus rating based on 19 buys and one sell assigned over the past three months. The average Mastercard price target of $416.22 implies 20.9% upside potential. Analysts’ price targets range from a low of $298.00 per share to a high of $472.00 per share.

Conclusion: Mastercard remains a strong buy on Wall Street

Mastercard is an incredibly well-run company with a wide moat and technological know-how. Some analysts may trim away from their price targets, but Mastercard is one of the few stocks that is holding on to its Strong Buy rating among the analyst community.

Mediation