Fintech Hubs in the Middle East and Africa

What are key fintech hubs in a region that nearly one in four people call home? The region in question is of course the Middle East and Africa (MEA).

For a region that is home to nearly 70 countries, MEA’s diversity offers a range of social, economic and cultural backgrounds that are home to some of the richest and poorest countries in the world. As a result, when ranking these hubs, you need to consider broader economic development indicators. Namely those relating to technology and wider digital, as well as those related to fintech.

Understanding that, you can categorize fintech hubs by country across MEA through the following levels:

- Tier-one – Premier Global Fintech Hubs

- Tier-two – Emerging Fintech Hub

- Tier Three – Early Stage Fintech Hub

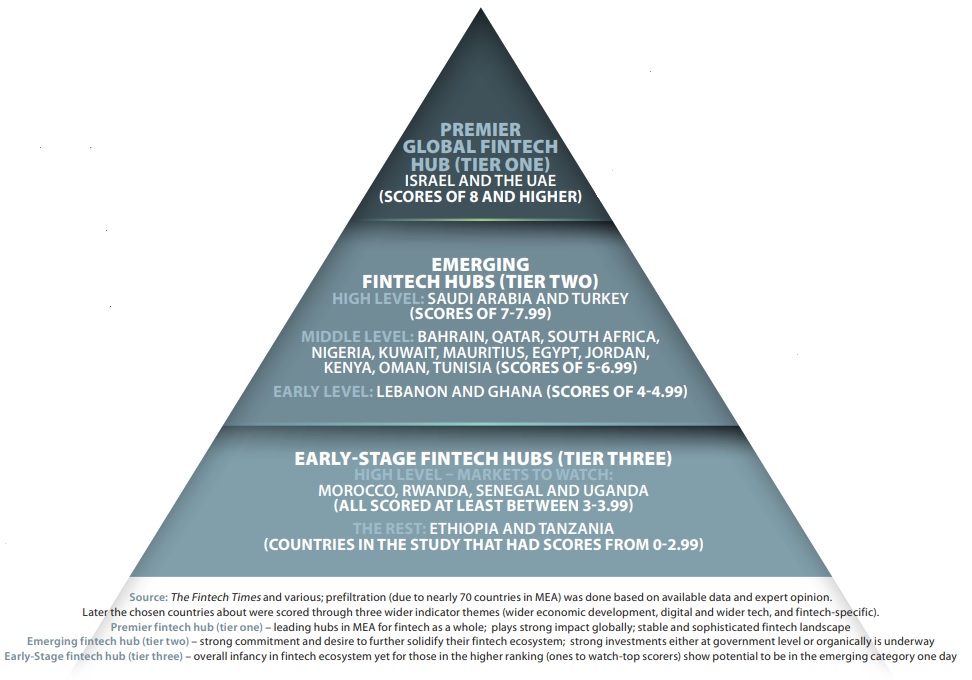

What are the tier-one leading global fintech hubs in MEA?

Israel and the United Arab Emirates

Israel and the United Arab Emirates share similarities that would consider them to be tier-one fintech hubs:

- Strongly developed economies – both are developed economies with a high standard of living. In turn, this has attracted talent from around the world.

- Home to large commercial, finance

- l and technology hubs – the two countries host respective hubs in other sectors. Especially those related to fintech such as finance and technology, with Tel Aviv in Israel being a hotbed of innovation (in addition to other parts of the country) and the UAE home to both Dubai and Abu Dhabi.

- Entrepreneurial hub and business friendly – this can be seen by the number of fintechs and technology companies they have. The UAE has over half of the fintechs from the Middle East and Africa (MENA) region (minus Israel and Turkey). Israel alone outnumbers the rest of the MENA region. In addition, it has also produced quite a few of the world’s unicorns just in fintech alone.

- Innovation-friendly policies – both governments have prioritized innovation, with Israel a major investor in R&D and the UAE envisioning a world of blockchain and metaverse.

What are tier-two emerging fintech hubs in MEA?

Saudi Arabia and Turkey (Tier-Two – Higher Range), Bahrain, Qatar, Kuwait, Egypt, Oman, Nigeria, Mauritius, South Africa, Kenya, Jordan and Tunisia (Tier-Two – Middle Range), Lebanon and Ghana ( Tier- Two – Lower range)

The Tier-Two category – whether in the higher, middle or lower range, shares similar characteristics:

- Large Populations or Small with an Outward Vision – Many on this list, such as the Big Four in Africa (Nigeria, South Africa, Kenya and Egypt), Turkey, Saudi Arabia have large populations. There are also the small ones like Mauritius which, despite being small, have strong external visions of being a regional hub. In many ways, it already has.

- Government ambitions with fintech in mind and pro-business policies – Many on this list have seen fintech play a strong role in their economic development prosperity. They have seen what wider digital development can bring to their GDP and the overall quality of life. This has also seen them generally promote the business as a whole, and fintech plays a part in that – through attracting foreign direct investment (FDI) and growing entrepreneurship to name a few. Some have historically been and still are financial or commercial hubs. Namely Bahrain, Kuwait and Lebanon, as well as Turkey and South Africa.

What are tier three early fintech hubs in MEA?

The remaining countries in MEA not mentioned will be considered to be tier three fintech hubs. This is divided into two subcategories:

Morocco, Rwanda, Senegal, Uganda (higher-tier “Markets to Watch”) and the rest of MEA (general tier-three – examples include Ethiopia and Tanzania)

Tier three nations share similar characteristics:

- Lack of fintech-specific and financial services derivatives or infants – Some of those on the list have fintech-specific derivatives or aspirations and/or financial services, where the government aims to support the growth of these sectors and create the ecosystem. However, these sectors are still very much in their infancy, not only compared to the world, but also among their other higher-ranked MEA peers. For example, many in this category still lack a specific strategic government vision and its implementation to take the sectors into overdrive, for example with Ethiopia and Tanzania.

- Middle or lower middle income or low income economies – their economic development of course has an impact on their infrastructure and current situation showing a lack of technology or availability that either limits innovations in fintech or makes it completely inaccessible to begin with, something many on this fintech categorization can relate to each other.

- Aspiration with future economy – There are aspirations, despite various challenges, that see the countries to convert their income status in the long term, so that they can alleviate poverty, but use technology and digital to help with that. Finally, “Markets to Watch”, as with Rwanda in particular, if their growth trajectory continues, will see them as Tier-Two fintech hubs for the foreseeable future.

To read more check The Fintech Times – Fintech: Middle East and Africa Report 2022.