Fintech crash is an M&A opportunity for bold banks

The Robinhood logo is seen on a smartphone in front of a displayed stock graph in this illustration taken July 2, 2021. REUTERS/Dado Ruvic/Illustration

LONDON, July 21 (Reuters Breakingviews) – Bank chiefs have spent years fretting over disruptive fintech upstarts including Affirm ( AFRM.O ), Klarna and Robinhood Markets ( HOOD.O ). Now that the former market darlings are on the ropes, established lenders like Goldman Sachs should think about buying them.

Banks are already scooping up smaller fintechs. JPMorgan last year bought British digital wealth manager Nutmeg for just under $1 billion, according to Reuters, while UBS ( UBSG.S ) agreed to pay $1.4 billion for Wealthfront in January.

But the latest market storm brings bigger fish into the net. Publicly traded pay-later group Affirm and its private rival Klarna are worth about $8 billion and $7 billion respectively, compared to peaks of nearly $50 billion. Their fast-growing consumer lending businesses could be attractive to Goldman, which already dabbles in the sector through a credit card partnership with Apple ( AAPL.O ). Meanwhile, $8 billion trading app Robinhood is worth little more than net cash. Buying it could help a lender target the so-called “mass affluent” US wealth market, such as UBS.

Register now for FREE unlimited access to Reuters.com

Headstrong founders can be an obstacle. Klarna’s Sebastian Siemiatkowski, Affirm’s Max Levchin and Robinhood’s Vladimir Tenev want to shake up old-fashioned economics, so they can resist selling to a dinosaur. Possible future regulatory interventions against the companies’ operations is another risk. And their red ink is a headache for the banks. Old-school lenders tend to be valued at a multiple of earnings or book value. Buying a loss-making group can therefore destroy the equity value.

The financial problem can be solved. Imagine Goldman bought Affirm for a 30% premium, implying an enterprise value of $10.5 billion. Achieving a respectable 10% return on investment by 2026 would require about $1.3 billion in pre-tax earnings, assuming a 21% rate, compared with a projected pre-tax loss that year of $179 million, using Wedbush- forecasts. Closing the gap would mean cutting two-fifths of Affirm’s costs that year. That might be plausible given the likely overlap in marketing and loan underwriting, as well as Goldman’s ability to fund through cheap deposits rather than expensive wholesale markets. Wedbush analysts expect Affirm’s financing costs as a percentage of revenue to rise to 8% next year from 6% in 2022.

It may be difficult to get fintechs to the negotiating table if the upstarts see the crash as a blip. Klarna’s chairman Michael Moritz, for example, expects the valuation to improve “after investors come out of the bunkers”. But interest rates are rising, and markets are less inclined to fund startup companies’ losses. The bank managers’ best argument for an agreement may be that the disruptors have no other choice.

follow @liamwardproud on Twitter

CONTEXT NEWS

Klarna said on July 11 that it had raised $800 million from investors. The deal valued the Swedish pay-later group at $6.7 billion, after including the new capital. That compared to a valuation of $45.6 billion in the previous fundraising round, in June 2021.

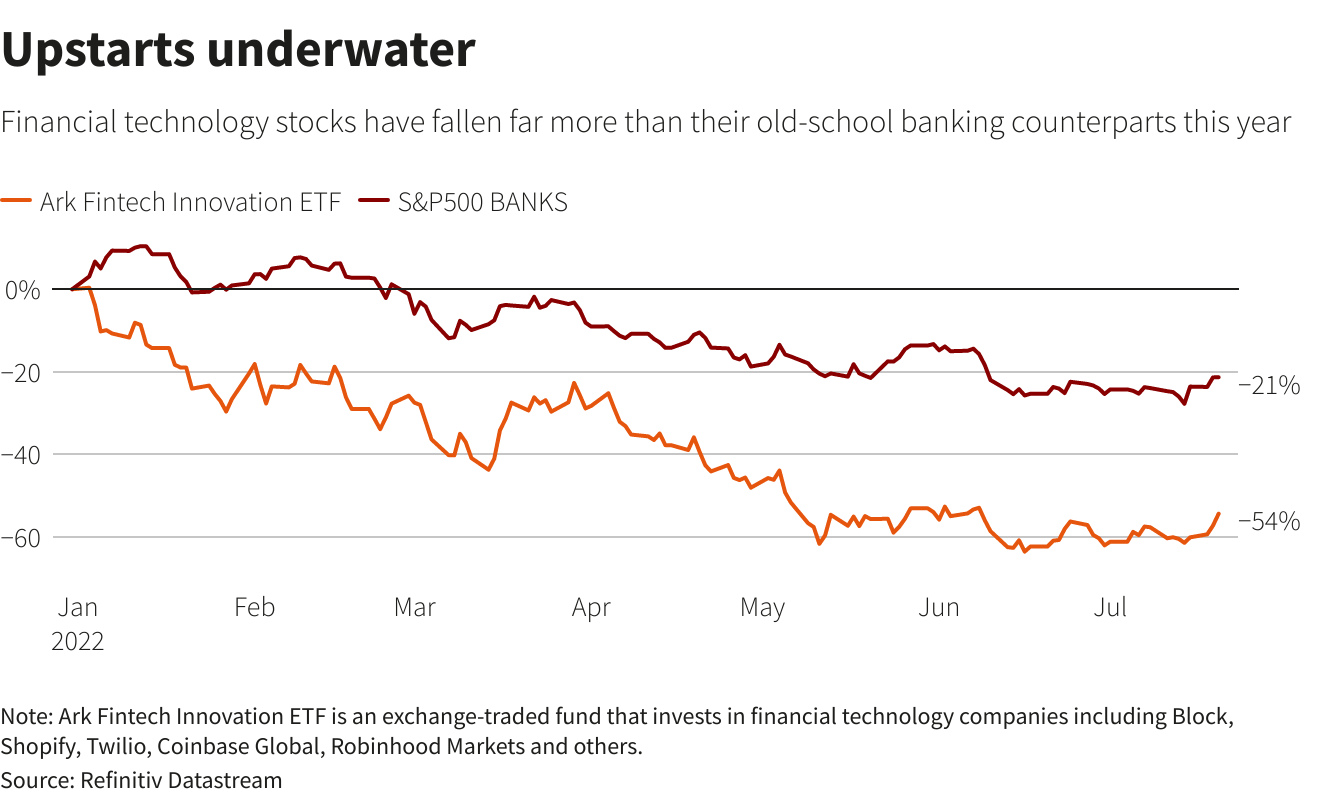

The ARK Fintech Innovation exchange-traded fund, which seeks exposure to fast-growing financial technology companies, fell 54% between the start of 2022 and July 20.

Register now for FREE unlimited access to Reuters.com

Editing by Neil Unmack and Oliver Taslic

Our standards: Thomson Reuters Trust Principles.

The opinions expressed are those of the author. They do not reflect the views of Reuters News, which is committed under its fiduciary principles to integrity, independence and freedom from bias.