Did you know these facts about Blockchain technology?

From India’s CBDC launch to startups incorporating blockchain technology, why is everyone adopting it?

New Delhi,UPDATED: December 22, 2022 1:49 PM IST

Did you know these facts about Blockchain technology?

By Nidhi Bhardwaj: Blockchain, also known as distributed ledger technology (DLT), uses a decentralized network and cryptographic hashing to make the history of any digital asset immutable and transparent.

Introduced in October 2008 as part of a proposal for bitcoin, a virtual currency system that does not rely on a central authority to issue money, transfer ownership or verify transactions.

Bitcoin was the first use of blockchain technology. Cryptography is used to link the growing list of records, known as blocks. Each transaction is independently verified by peer-to-peer data networks, time-stamped and added to a growing data chain. The data cannot be changed once it has been registered.

What makes Blockchain popular in India?

Blockchain is a digital ledger that has recently received a lot of attention in the technology world. But why has it grown in popularity? So let’s delve into it to fully understand the concept.

As for Indian businesses, nearly 56 percent of them are incorporating blockchain technology into their core business. The National Informatics Center has established a Blockchain Technology Center of Excellence (CoE), which serves as a coordinated, interoperable blockchain ecosystem across the country.

Furthermore, in December last year, the Ministry of Electronics and Information Technology (“MeitY”) released a national strategy for blockchain (strategy) which aims to incorporate blockchain technology into public systems, especially for e-governance, and offer blockchain as a service. The strategy also calls for state governments to create state-specific blockchain applications on top of the shared blockchain infrastructure.

With the increasing digital and decentralized innovations taking place, blockchain is also being explored in CBDC research and prototype experiments in India by the central government. Blockchain-based CBDC can help increase efficiency and create more secure payment systems.

What are the types of Blockchain?

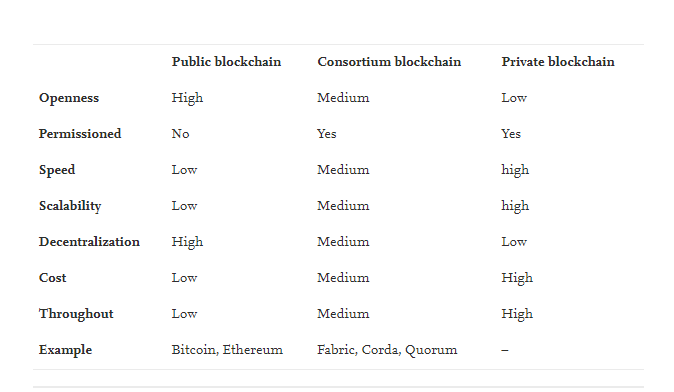

There are four types of blockchains, such as public blockchain, consortium blockchain, private blockchain and hybrid blockchain.

The public blockchain

When it comes to the public blockchain, top cryptocurrencies like Bitcoin and Ethereum are built on it. The permissionless platform underpins the public blockchain, which allows everyone to participate. This blockchain mode is extremely decentralized and lacks aspects of security and privacy.

Source: Elsevier

Consortium blockchain

Consortium blockchain is permissioned and built in collaboration with multiple organizations. Each organization is one node in the blockchain; if other organizations wish to join the consortium’s blockchain, authorization from the consortium is required. Consortium blockchain is less decentralized than public blockchain, but it has higher throughput and performs better. The consortium blockchain is represented by Hyperledger Fabric, Corda and Quorum. Quorum is Ethereum’s enterprise version.

Private blockchain

Private blockchain is permissioned and centralized than consortium or public blockchain. Private blockchain is managed by a single organization, which decides who can participate, implement consensus and maintain the shared ledger. The private blockchain is more trusted by the participants and performs significantly better than the consortium blockchain.

Hybrid blockchain

A hybrid blockchain is an innovative type of blockchain technology. This type of blockchain makes the data visible, accessible to all users and can be tampered with. However, some applications are not available to public or private users. IBM Food Trust is a hybrid blockchain that was created to improve efficiency throughout the food supply chain.

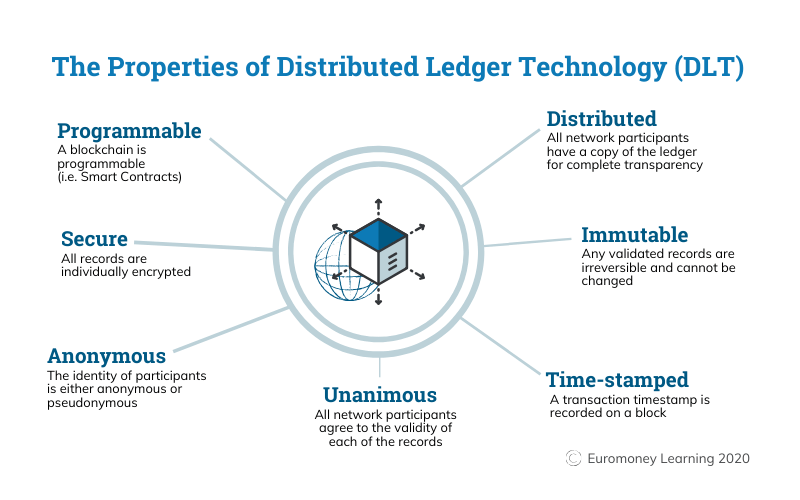

How does blockchain technology work?

Source: Euromoney Learning

- The data is shared openly with all network nodes and verified through consensus by participants known as miners.

- It supports encrypted transactions, timestamping and proof of work.

- In the case of blockchain, there is no centralized agency or institution that controls or ensures data security, as a bank would with a traditional database.

- This means that data on the blockchain can only be accessed by those authorized to do so, such as developers using real Bitcoin addresses or users who can prove their identity using private keys from their respective cryptocurrency wallets.