Coinbase Stock: Remains In Uncharted Waters Midt Crypto Selloff

Cryptocurrency and mobile technology solarseven

Investment statement

Coinbase (NASDAQ: COIN) has fallen 80% since reaching its record high of $ 360 in November last year, eroding $ 48 billion in value. So, what happened? There are several reasons. First, the general trend of growth stocks being hammered at times of rising interest rates and rising share premiums. Second, the bitcoin price collapsed by 60%. And last but not least, its poor performance and $ 1.58 billion cash drain in Q1-22. These factors led us to make significant adjustments to our FCF valuation model with a new target price revised down to $ 52. This price is in line with today’s market, so we changed our view to keep and will follow how things develop in the crypto market for further analysis.

Crypto sales

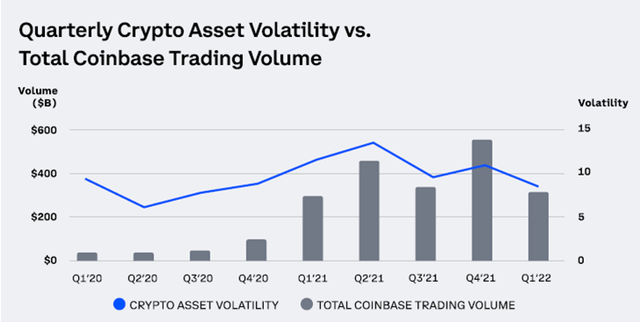

As we have thoroughly researched in our previous article, Coinbase has always had a high correlation with Bitcoin (BTC-USD) due to the significant involvement of retailers and the nature of the business. Considering recent cryptocurrencies, it is not surprising that COIN has had a massive hit with its revenues falling by half and its operating cash flow turning from a profit of USD 846 million in Q4-2021 to a cash loss of USD 830 million in Q1 in year. Thus, one of the risks we have talked about before has materialized, and since COIN is a relatively young venture with revenues still not sufficiently diversified between retail and institutional money, we saw a massive fall in the share price.

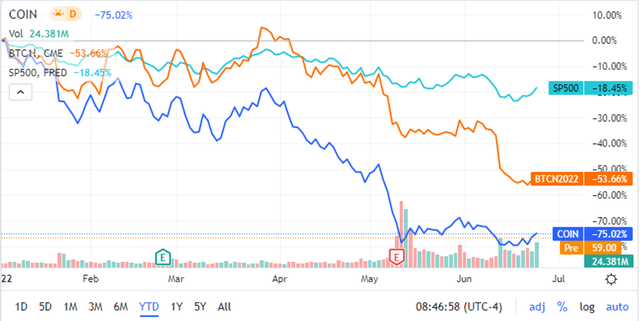

How things will develop for COIN from now on depends mainly on developments in the crypto market, and this is a big unknown. What we have learned so far is that crypto is not a hedge against stock market pulls, and the diversification benefits were hugely overestimated in the past. Since the beginning of this year, S&P has lost 18% while BTC fell 54% with Coinbase falling 75%.

Seeking section for alpha maps

Bitcoin’s sales were caused by two main factors: a) the Fed and other central banks’ hawkishness in response to rising inflation and b) the collapse of the Terra blockchain in May. The latter event forced the Luna Foundation Guard to sell 80,000 Bitcoins aimed at supporting the dollar stick of its UST stablecoin. This dump created massive selling pressure with the BTC price falling from USD 39k to USD 29k in a few days in early May. It also did not help UST from the collapse, and the link was then broken with the stablecoin price falling from $ 37 to less than a dollar. This incident created tremors in the crypto area with retailers rushing to get rid of their crypto positions.

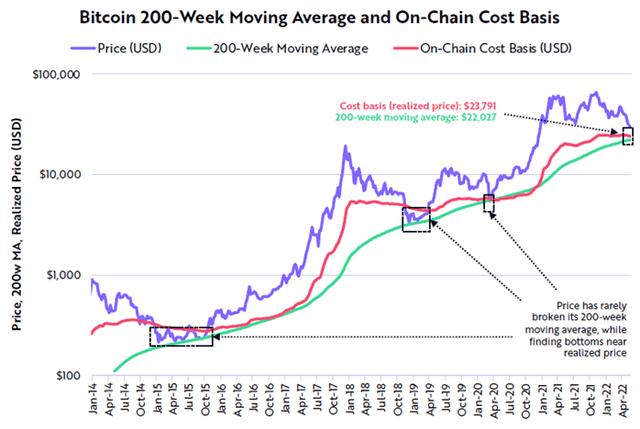

From the chart perspective, BTC has broken many technically important levels such as the 200-week moving average and its cost basis realized price – the levels that have not been broken by other major bitcoin sales in 2014 and 2018. It created more downside pressure with BTC to look. for a support of a technically important $ 20k that currently holds.

ARK Invest Bitcoin monthly report for May 2022

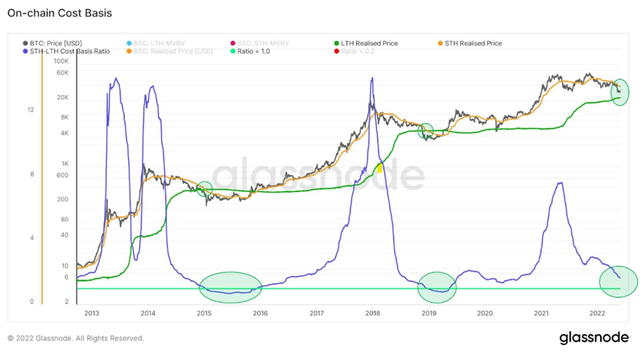

If we look at other indicators that are somehow considered fundamental to Bitcoin, such as short-term owners of bitcoin vs long-term owners cost basis, we can see that there has been a capitulation of short-term owners, but the relationship still has some room to go to the support it held in 2015 and 2019.

Diagram published by beINcrypto

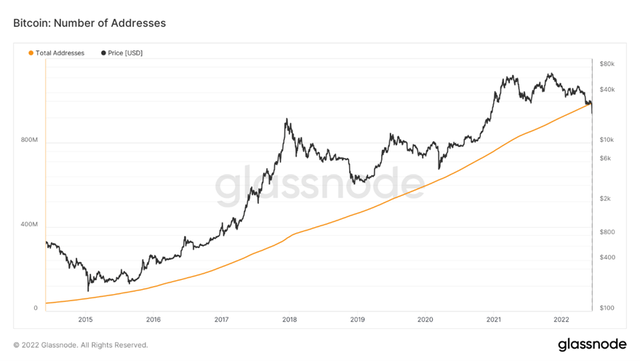

Another positive factor is that the number of total addresses has actually continued to increase and is approaching 1 billion total addresses (990 million as of June 20, 2022), indicating continuous Bitcoin adoption.

Bitcoin: number of active addresses (Glass Node Studio)

It is always difficult to call a market bottom, and when we analyze previous crypto bear markets, we can see that sales in 2014/2015 lasted for almost two years, while in 2018 it lasted for 360 days. The average length of an American bear market is approx. 9 to 10 months, but there are large differences with the shortest of 33 days and the longest 622 days in the period 1929–2021. We can not also look at bitcoin fundamentals in a vacuum as we have to consider the general state of the economy, inflation, war, etc. All these factors will depend on how long this bear market will last.

To sum up, the bitcoin market looks fundamentally healthy, and there are indications that bitcoin is being oversold. However, further price developments cannot be seen in isolation and depend to a large extent on current macro developments such as inflation, political uncertainty, the length of the war in Ukraine, to name just a few.

Economy

The COIN Q1-2022 results were on a weak side, but this has been widely expected given the turmoil in the crypto market. Its monthly users decreased from 11.4 million to 9.2 million QoQ, but was still 50% higher than in Q1 last year. Trading volume fell in line with the volatility of cryptocurrencies.

Coinbase Q1-2022 Shareholder letter (Coinbase Q1-2022 Shareholder Letter)

Revenue fell 49% to USD 1.2 billion, and COIN recorded a net loss in the first quarter since the listing. Although transaction costs fell by 45% as these are directly related to revenue, the operating cost side increased by a total of 9%, mainly due to an increase in the number of employees as COIN increased its total staff by 33% in this quarter. COIN gave no indication of their cost management plans at the earnings interview, but we have seen reports in FT in June that they plan to cut almost a fifth of employees.

Total net loss was USD 430 million while adjusted EBITDA was USD 20 million (down from USD 1.2 billion QoQ). Cash flow was also negative by USD 1.5 billion, with a loss of USD 830 million and cash flow from investments negative USD 691 million (mainly driven by investments in cryptocurrencies).

The company has $ 6.1 billion in liquidity that will help it withstand three to four quarters of cash drainage without additional financing, so its financial solidity depends directly on how long this bitcoin bear market will last.

Valuation

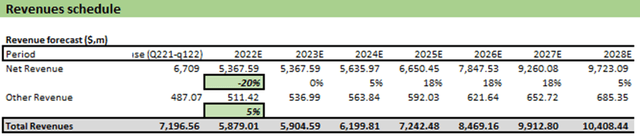

Since our previous article on Coinbase in February this year, we had to adjust our valuation model quite dramatically. First, our revenue forecasts have been reviewed downwards over the next two years. We estimate that the top line number will fall by 20% in 2022 and will be flat in 2023 (against previous estimates of an average increase of 18% in both years). This is based on previous precedents for crypto sales, as in both 2014/15 and 2018/19 we saw almost a year of directionless trading after the bear market in crypto.

The author’s estimates of revenue growth (Author’s calculation)

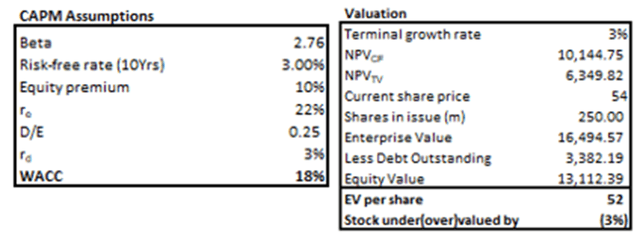

Another significant adjustment was to the CAPM model. The US Treasury 10-Year that we use as a proxy for the risk-free interest rate increased from 1.8% to 3%, and we have also revised the equity risk premium to 10% to take into account increased volatility in the crypto market. As a result, the WACC rate we use to discount FCF has increased from 11% to 18%.

Author’s FCF rating (author’s calculation)

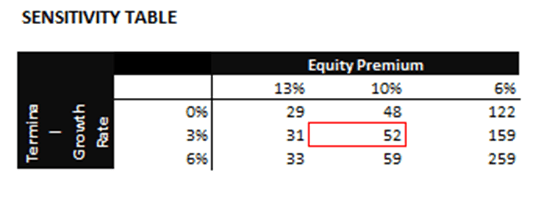

As a result of discussed adjustments, our target price for the stock is around $ 52, which is exactly where it is trading now. For investors with a different risk appetite, we also present the sensitivity table below, which shows the target price’s dependence on the equity risk premium.

The author’s calculation

The current average market risk premium in the US is 5.6%, so if we use it, the target price will be around $ 160.

Risks

As we mentioned in the previous article, there are three main risks associated with cryptocurrency exchanges, and these are highly correlated with bitcoin, regulation and cyber security threats.

Fundamental to bitcoin looks convincing, but judging by the recent stories, the market probably has some room to decline further. The market also expects Mt Gox to release BTC 137k to its creditors as early as August, which could increase existing sales pressure.

Are there any chances that the bear market in bitcoin will not end? I personally think it is very unlikely since we have already seen several bear markets in crypto rooms, and with each subsequent increase the chances of following price recovery because the market becomes more mature with an increasing number of developers and investors.

Summary

Given the current state of the crypto market, we had to implement significant adjustments to some of the inputs in the free cash flow valuation model, which have affected the target price down to $ 52 (compared to the previous $ 358), which is in line with the current market price. Coinbase is still very closely correlated with the bitcoin price, which poses a huge risk in times of crypto bear markets.

According to the latest stories and an upcoming unlocking of 137k BTC, we believe that we will see another leg down in the bitcoin price that will add more sales pressure in the short term. Whether COIN is able to withstand this period of high volatility depends on how long the current bear market will last. With a cash buffer of $ 6 billion, COIN has a certain cushion for a while, but if there is no improvement in the crypto market by Q1 / Q2 next year and without further funding, we believe COIN may get into trouble. We currently have a view on this stock based on the FCF model and believe we need to see some improvement in the crypto market before revising our COIN forecast.