Cipher: Do Not Look Up (NASDAQ:CIFR)

Charday Penn/E+ via Getty Images

Cipher Mining Inc. (NASDAQ: CIFR) is building mining capacity at an impressive rate; it has signed an unprecedented Power Purchase Agreement (PPA) with Luminant that gives it a competitive edge over all the miners I follow except Riot Platforms (RIOT).) and guarantees a profitable Bitcoin (BTC-USD) operation at all Bitcoin prices in the last three years. The PPA has the flexibility to allow Cipher to sell the electricity purchased under the agreement back to the grid when electricity costs make it more profitable than mining Bitcoin. Last quarter it sold electricity, it added $150,000 in profit to the bottom line.

Cipher has signed an equally impressive deal with Canaan (CAN) for 11,000 new miners which will be activated in Q3 and indicated in the recent earnings call that this is part of an expanded agreement that gives Cipher favorable purchase prices and payment terms.

Management is delivering growth while minimizing debt and dilution, trying to build a true industry leader. Listening to the recent earnings call, it was clear that they believe they are already industry leaders and are on the right track. They see no obstacles and press on with energy and speed.

They keep their heads down, work hard and follow the plan. If they look up, they may see some downsides on the horizon, potentially seriously disrupting their plans.

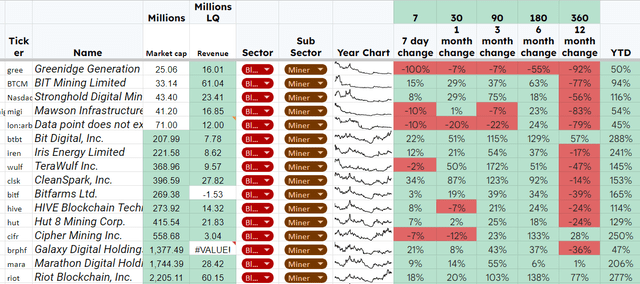

This is the third article I’ve written about Bitcoin miners in the last few weeks. They have experienced a price boom that started in December and continues. Initially, Cipher led the pack, but as you can see from the dashboard below, they have recently fallen back. This article will explain the reason for the initial growth and present an argument for the decline.

Mining companies’ results (May 10) (Author database)

In the last earnings call, I was looking for information on two things (Q1 2023, May 9)

- How is the capacity building going?

- What is happening with the Luminant trial?

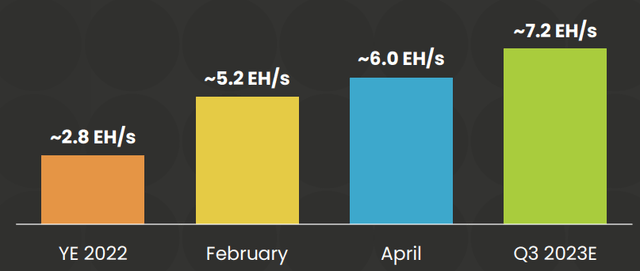

Cipher Capacity Build

Cipher is growing fast; they are doing a great job (Slide 7 of the Q1 2023 earnings call presentation)

Cipher capacity (revenues for the first quarter of 2023)

7.2EH/s makes Cipher a real player in this market. Riot Platforms cites a current figure of 9.8 and a target of 11.

I listened with interest to hear how well the development was going; I heard management say “best in class” enough times that I started counting when they said it. I was impressed with the quoted Bitcoin mining performance, 45 in two days (May 7th and 8th), and of the low-cost production and energy prices paid. The purchase of 11,000 mining rigs from Kanaan was exciting and I liked how the operation was funded by selling Bitcoin mined.

However, they did not mention, nor were they asked about, a lawsuit that could potentially bring this particular company down.

Cipher is at odds with Luminant

Luminant, a subsidiary of Vistra Energy (VST), supplies electricity to Odessa, one of Cipher’s 4 mining facilities. The power is delivered through a power purchase agreement which is an excellent deal for Cipher. It provides very affordable energy and allows Cipher to sell energy back to the grid when the price of electricity is higher than the value of Bitcoins mined. Cipher management believes it gives them a significant competitive advantage over their competitors. From the research I’ve done, they’re probably right. PPA has delivered an average cost per kWh of 2.7c (slide 3 of earnings call presentation) compared to Riot at 2.9c and Hut 8 Mining Corp. (HUT) of 3.4c. Of the 16 miners I track, 9 publish their energy costs, and these are the three lowest numbers.

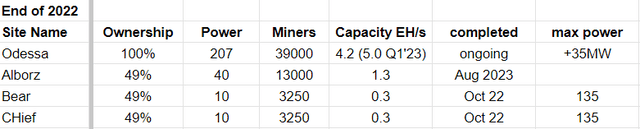

The Odessa site is critical to the success of Cipher. They have four mines; Odessa is wholly owned, and they have a JV in which they are a minority shareholder in the other three.

Cipher Mining Sites (Q1 2023 Slides)

In the earnings call, we heard that the Odessa site (based in Texas) has continued its build-out and reached 5.0 EH/s capacity, meaning Odessa represents 84% of Cipher’s mining capacity. Cipher owns 49% of its other locations as part of a JV with WindHQ. In the earnings call, we heard that Cipher ordered 11,000 more miners for Odessa and expects to have them installed by Q3.

Management did not mention the legal dispute with Luminant in the first quarter earnings call. The FY 2022 report (from P60 10K 2022) described the issue as inconsequential. In my view, it is potentially very material.

Luminous trial (FY 2022 10,000 notes)

In this case, Luminant is seeking repayment of $6.7 million it claims was paid to Cipher in error. Cipher said in the FY 2022 report

We completely dispute the allegations made by Luminant, and we intend to contest the case vigorously

The industry has a precedent, which is the reason for my concern. Hut 8 encountered a similar problem with the electricity supplier to one of its sites provided by Devon Energy (DVN) subsidiary Vista. (I covered the issue in my recent article (The Bitcoin Miners Are Flying, But Where Is Hut 8 Going?).

Hut also vigorously contested the claim; finally, Vista turned off the power!

The matter has still not been resolved, but the entire site is still without electricity, and the nearly 8,000 mining rigs that should be in operation are in storage. Hut does not expect to be able to provide power to the area and is looking for new homes for the miners (and a new PPA to provide power).

If Luminant cuts power, as happened to Hut, Cipher will lose 84% of its mining capacity, as well as the PPA, the source of its competitive advantage, valued on the balance sheet at $71 million (derivative line items slide 13), and it could be in territory for continued operation.

Luminant has not paid the money to Cipher under the PPA (page 60, item 3 10k FY 2022), which means they take the dispute far more seriously and have the right to terminate this contract.

(page 4 FY 2022 10K)

The agreement also includes certain curtailment events that give Luminant the right to limit the electrical power delivered in each contract year. Subject to certain exceptions for early termination, the agreement provides for a subsequent automatic annual renewal, unless one of the parties gives written notice to the other party of its intention to terminate the agreement at least six months before the end of the current period.

The risk seems overwhelming and management reported it as not a significant issue.

Having over 80% of their mining rigs in a single location in Texas is another problem. In December 2022, a storm in Texas damaged a building and took 17,000 Riot Platform’s mining rigs offline. Riot, the market leader and operator of several sites, has sufficient capacity to cope with this level of disruption; I’m not sure that’s true with Cipher.

Cipher bought 11,000 miners from Canaan.

Cipher said on the earnings call that the 11,000 miners are the lowest costs and best payment terms they’ve ever had; they also said it was the best deal they had ever heard of in the business!

In the conversation, we heard how the managing director had taken a several-week trip to Asia to build a better relationship with one of the mining producers. They mentioned having discussions with Bitmain, MicroBT and Kanaan. The CEO discussed the sales pitch they presented; Cipher believes that as a market leader they have superior finances and the ability to be a leading long-term customer.

Kanaan is the lesser known of the three. Its Avalon mining rig has a reputation for working well in high temperatures (useful for Texas) and is known for its reliability. It is not considered as powerful or profitable as Bitmains Antminer or MicroBT’s WhatsMiner. It is challenging to get precise information about the mining profitability of the different miners since it is a source of competitive advantage for miners and producers

As far as I know, the two actual market leading miners (in terms of capex) Riot and Marathon Digital Holdings (MARA) are not following Cipher and buying from Canaan. They buy from Bitmain and MicroBT. It makes me wonder if the amazing deal that Cipher signed was not one that Bitmain and MicroBT were prepared to sign. This agreement may result in Cipher having poorer mining performance per rig compared to the market leaders they want to be.

Executive Pay

I think too many SPAC deals have lined the managers’ pockets at the investors’ expense. I have avoided several companies on this issue alone.

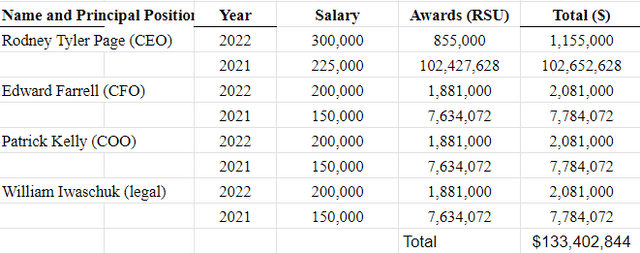

Cipher CEO Tyler Page previously worked for Bitfury as head of business development. Bitfury started in Holland in 2019 as a Bitcoin miner; they are now an investment firm and have invested in several companies across the crypto landscape. Bitfury owns 5% of Hut 8 and 81% of Cipher.

Page was at Bitfury for eight months before becoming the founding CEO of Cipher. Page received $103 million in salary and awards during the first two years of Cipher’s operation. The power of attorney where this information comes from explained that it was necessary to keep him in business. (As a comparison, the CEO of RIOT received a total of $43 million for the same period)

Payment to officers (Proxy page 28)

The amount of money is substantial, but the majority is performance-based restricted stock, so shareholders should benefit if Page gets the full amount.

Best in class: groupthink?

I often listen to earnings calls live; you can get additional information from how management answers questions and reads out their prepared statements. After this conversation, I came away convinced that the management believed they were already the best mining company in the class. They said the phrase more times than I can remember. I heard no dissent or disagreement, no one thought they were anything but best in class. The managers already believe they are the best Bitcoin mining investment and can’t understand why the market doesn’t agree and the share price isn’t rising at the same rate as others.

It reminded me of the Hollywood movie where the characters were so busy making money from the asteroid that they forgot it was on its way to Earth.

Cipher economy

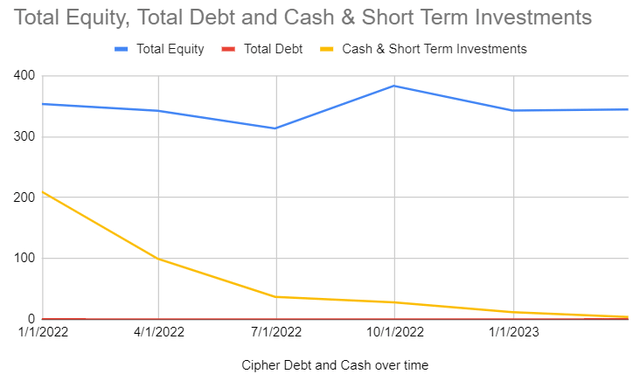

Decipher debt and cash over time (Author database)

Cipher has zero debt, but has now used most of the cash raised in the SPAC transaction. In April, Cipher mined and sold 406 Bitcoins to fund its operations, leaving 427 Bitcoins.

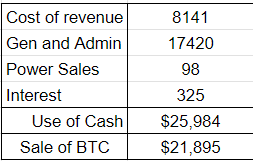

During the last quarter, Cipher reported the following cash movements.

Cash usage (Revenue Q1 2023)

It is a low-cost operation with only 28 employees (versus 489 at RIOT). However, with a reported $3.9 million in cash and roughly $12 million in BTC, its short-term assets are only $16 million, less than what it spent in Q1 2023.

Cipher said it intends to continue to fund its growth and operations using the Bitcoin it produces, and while it has a large ATM prospectus in place ($250 million), it does not intend to issue new shares. It looks like a tight balancing act; I expect any significant disruption will force Cipher to take on debt or go to the markets.

Conclusion

Cipher has increased its capacity rapidly and signed excellent deals, making it a low-cost operator with a potentially sustainable cost advantage due to its PPA.

It has increased its capacity with very few employees compared to its peers.

Cipher is short on cash and uses the bitcoins it produces to fund its operations, so I think any drop in production will likely mean a trip to the ATM shelf.

The PPA with Luminant is its biggest asset and its biggest threat.

At the moment it seems too risky to buy into Cipher.

My next miner article will be on Riot Platforms.