Cable wants to help banks cut financial crime through automated insurance

Image credit: Cable / cable co-founders Natasha Vernier and Katie Savitz

People in the United States reported $8.8 billion in financial fraud in 2022 to the Federal Trade Commission, and while the FTC received fewer reports, 2.4 million versus 2.9 million in 2021, the total amount is 30% higher than in 2021. Wire transfer or payment fraud amounted to $1.6 billion in 2022.

When you expand this globally, Cable co-founder Natasha Vernier told TechCrunch that financial crime becomes a $4 trillion problem. And a Vernier, co-founder Katie Savitz and the Cable team have been working on it since 2021.

Vernier explained that banks and fintech must first have controls in place to reduce risk. Controls can include Know Your Customer checks, sanctions, screenings, transactions and monitoring, all of which providers like Unit21 and Alloy do.

About a decade ago, banks were fined by regulators for having “inadequate financial crime controls,” and while the number of fines fell as surveillance providers came in, some banks still receive fines for having “ineffective controls,” Vernier said. That’s because there is a second requirement that regulated financial institutions must meet, which is to independently test whether their controls are actually working.

“So far this has been done entirely manually,” she said. “Banks and fintechs manually test a small percentage of accounts to try to see if these checks are working. That’s what we’ve automated, and we believe we’re the first and only automated solution available at the moment.”

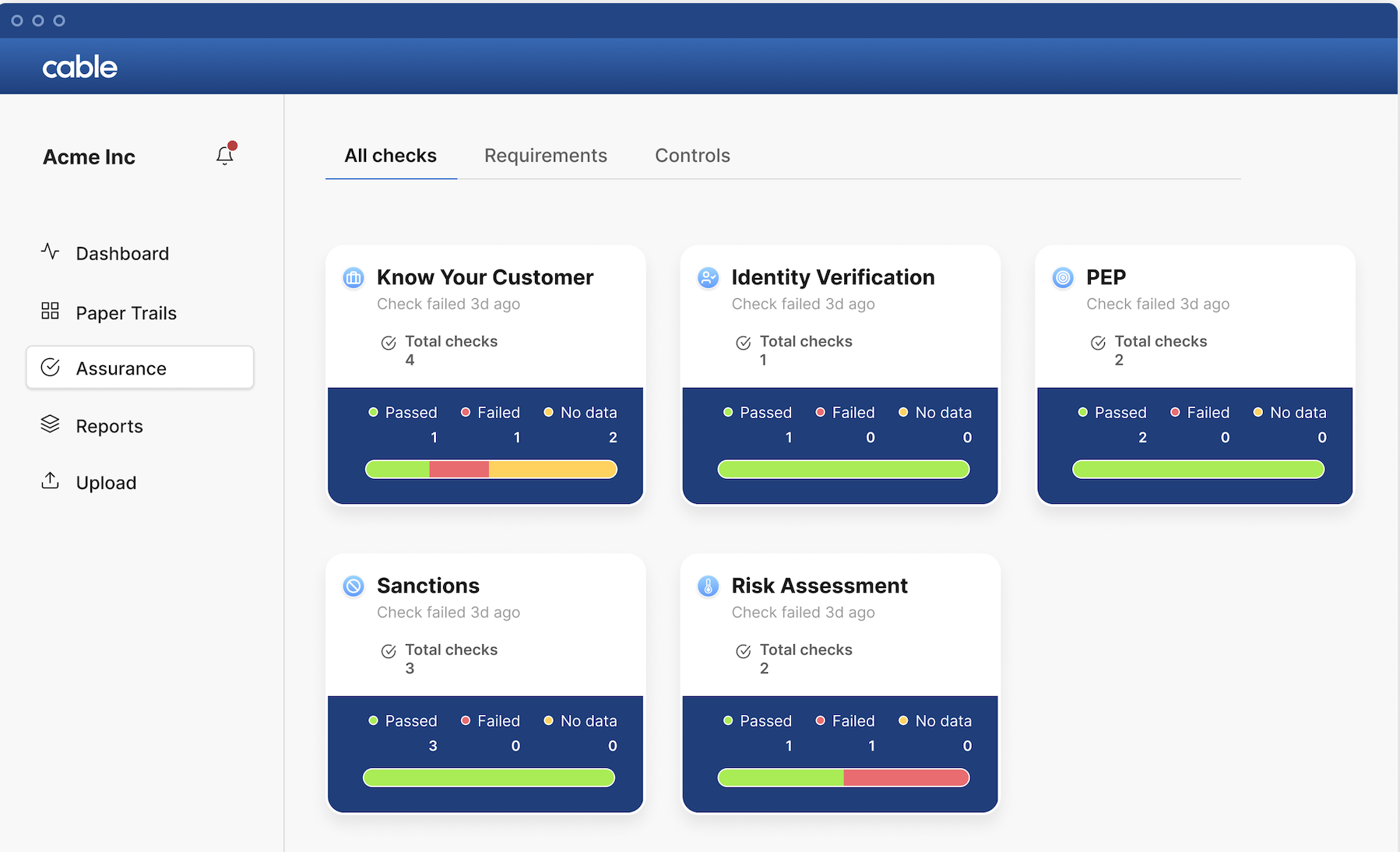

Cable’s Financial Crime Risk Assessment Panel (Image credit: Cable)

This makes Cable’s platform, which provides automated assurance and risk assessment, complementary to many of the financial crime providers. It enables banks and fintechs to monitor all their accounts – not just a fraction as before – to know in real time whether they are compliant with regulations and whether their error controls are working as expected to combat breaches.

Cable also provides Banking-as-a-Service organizations with oversight of the fintech partners they work with – remember that most fintechs do not have banking licenses and therefore work with banks to provide financial services.

In the past year, the company has increased revenue fivefold, and since 2021 has attracted clients including Axiom Bank, Quaint Oak Bank and Griffin on the banking side, and fintech and crypto companies, including Tide and Ramp.

“Fintechs have to partner with banks to essentially borrow their license,” Vernier said. “That’s where we find real traction and one of the areas that the OCC (Office of the Comptroller of the Currency) is particularly focused on right now: banks that lend their license to fintechs. They need to understand the effectiveness of the controls on these fintechs , and our product is perfectly suited for that use case.”

Today, Cable announced an $11 million Series A, led by Stage 2 Capital and Jump Capital, with participation from existing investor CRV. The new investment gives the company just over USD 16 million in total funding.

The capital enables the company to hire across product, engineering, data and go-to-market teams and also accelerate product development. Vernier said the company has only built out 1% of the products and features on its two-year roadmap.

Meanwhile, Vernier said as the banking industry moves forward, it will continue to add more ways for consumers to manage their finances instead of just traditional banks. And with that will come more scrutiny from regulators for improved oversight, which is why she said it’s the “perfect time for Cable to raise more money and accelerate.”

“Regulators are particularly interested in efficiency testing, but also just the volatility in the banking industry right now, with COVID and whether we’re in a recession or not, there’s increased financial crime,” Vernier said. “We have certainly seen, globally, an increase in fraud and other types of financial crime in recent years. And as real-time payments roll out in the US, we will see more financial crime.”