Bitcoin Will Return Above $32,000 in Rupture Against the US Dollar (NYSEARCA:BTC)

KanawatTH

Investment thesis

The US dollar is facing challenges with de-dollarization, debt crisis, potential economic recession and the rise of cryptocurrencies such as Bitcoin (BTC-USD). Against this backdrop, Bitcoin’s popularity has grown. After finishing the first quarter on a strong note, it is is entering a consolidation phase and will have the chance to get back above $32000.

Technical Analysis: Entering Consolidation, Next Major Resistance at $32000

Driven by several factors, including tight monetary policy and the banking crisis, the crypto market performed strongly in Q1 2023, with the total market capitalization growing by 49% to $1.19 trillion. BTC rose 72% to close at $28,440, while Ethereum (ETH-USD) rose 53% to close at $1,827.

BTC bounced back after testing the $15,000 support in Q1. And entering a new quarter, BTC also enters a new journey in terms of weekly and monthly lines.

We used the Donchian Channel (“DC”) indicator to assess market volatility. From the weekly chart, we can see that the weekly line of BTC is still below the mid-band of $32,000 and it has fluctuated slightly for over two weeks after the strong rally. It seems that BTC is still in a consolidation phase after rebounding at the weekly level. Meanwhile, the Average True Range (ATR) indicator has emerged from a long-term downtrend, but remains at a cyclical low, indicating that the market is still consolidating. Therefore, by combining the two indicators, we believe that if the weekly line breaks meaningfully above the middle band, while the ATR indicator also reverses and breaks through, it means that BTC will enter a strong upward phase and it is advisable to go into the market at an appropriate time.

Bing Ventures

The monthly line of BTC has just experienced three consecutive bullish candles, but it has yet to recover the loss from last June when BTC started at $35,000. Combined with the center line of the DC indicator in the weekly chart, we think $32,000 could be the next major resistance level. Using the DC indicator, we can see that the monthly line of BTC is still below the middle band, but is high above the lower band. Meanwhile, the ATR indicator continues to be in a long-term downtrend. This means that an immediate reversal may not be in sight. Indicators such as increased outflows from stablecoins and capital outflows from stock exchanges also confirm that the upswing is not sustainable.

Bing Ventures

Macro environment: Fed tightening cycle near end, multipolar reserve system be the trend

The US payroll data for April released on May 5 was better than expected and showed that the labor market was robust. Meanwhile, the Consumer Price Index (CPI) report released on April 12 showed inflation slowing again. Although market concerns about the vulnerability of the US Dollar Index increased, given that economic activity is at a reasonable level and inflationary pressures have eased, we believe that the Fed’s tightening monetary cycle may be coming to an end.

Bureau of Labor Statistics

In the past, the Fed’s aggressive tightening policies have resulted in massive capital inflows, leading to a global crisis in the US dollar. While the dollar crisis intensified, it did not lead to liquidity risk. And in the first quarter of 2023, global capital flows into dollar-denominated assets have slowed. Therefore, we believe that the US Dollar Index could fall to its lowest level of the year in the coming weeks and remain sideways thereafter.

Most importantly, the Russia-Ukraine war has made it clear to people in the US dollar system that US dollar reserves can be frozen by the US. The gradual decoupling from the US dollar and multipolarization will be the trend in the global financial market.

A potential result of this trend is Bitcoin consolidating its position in the global financial landscape. And the performance of US stocks and US Treasuries confirmed favorable macro conditions contributing to this trend.

US stocks’ performance in the first quarter was in line with expectations with both fundamental and technical indicators in bullish mode. First, personal consumption expenditures (PCE)’s below-expected year-on-year increase of 5.1% in February indicated subdued inflationary pressures, which boded well for the stock market. Second, the US economy remained strong and corporate profits continued to grow, supporting the rally in US stocks. Third, the employment rate looked good. And on the policy front, the Federal Reserve’s change in stance also helped to reduce downward pressure on the market.

Bloomberg

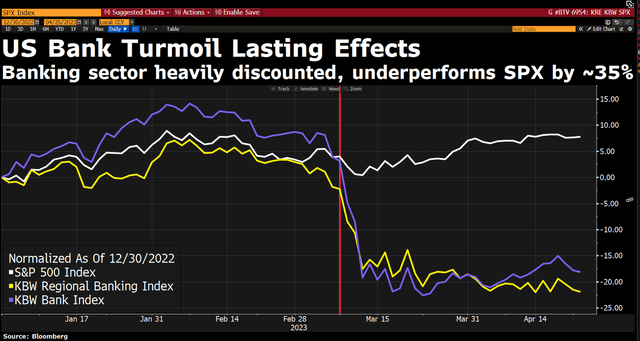

In Q1, the S&P 500, Dow Jones and Nasdaq all performed strongly, with the Nasdaq leading the rise due to the better performance of technology stocks. Meta and Tesla shares both rose over 60%. On the contrary, bank shares performed worse. Both the KBW Nasdaq Bank Index and the KBW Nasdaq Regional Banking Index declined.

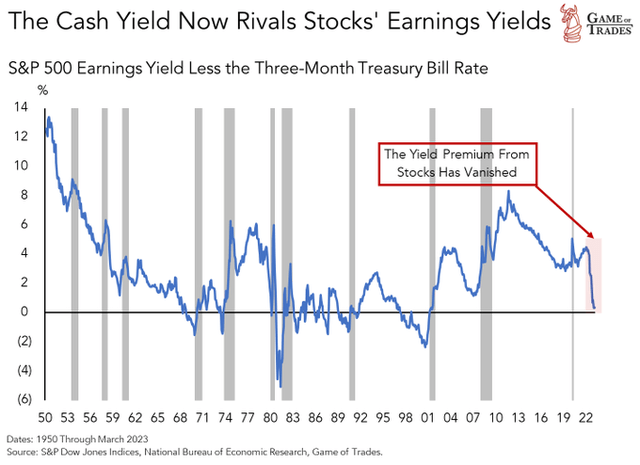

It should be recognized that the general rise of the S&P 500 has covered the sluggishness of the entire market and large technology stocks have become safe havens for investors. We believe the US economy is at a crossroads when it comes to choosing between continued growth in the stock market and an economic recession, and one of the biggest risks the market will face in the coming months will be the US economy falling into stagnation.

S&P Dow Jones Indices

The ongoing first quarter earnings season and key financial data releases should have a big influence on market performance, especially the data on cooperative performance and economic growth. That the Fed becomes more dovish will contribute to an improvement in the market.

The performance of US stocks in the 2nd quarter is unpredictable due to the continued existence of some uncertainties from last year, particularly the impact of interest rate increases on the US economy. Although the S&P 500 has been in sideways movement lately, daily volatility is increasing, making it difficult to assess the true health of the market. As S&P 500 companies successively release their Q1 earnings, we believe that EPS forecasts will be reduced. We also believe that the trend of reduced profit margins may continue until the end of the year before we restore growth.

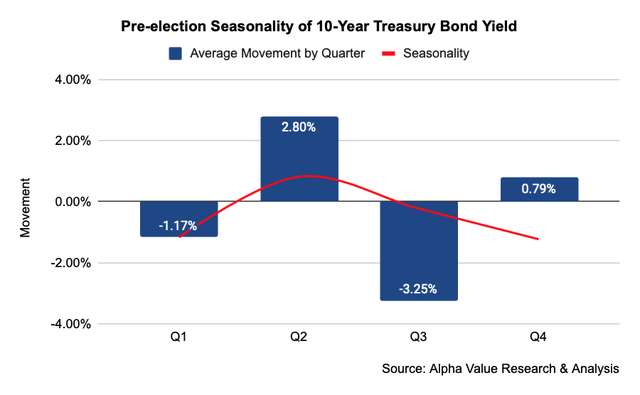

The US 10-year Treasury yield often stays in long-term downtrends, but every time it rises to the upper edge of a downtrend channel, a global financial crisis occurs. This time the speed and degree of the upward breakthrough was unprecedented in 40 years. Currently, the US Treasury yield curve is rapidly turning positive, which could be a harbinger of a US economic recession. Britain and the Eurozone were big buyers of US Treasuries, while Japan and Korea pulled money out of the market “reluctantly” and China continued to cut holdings. We believe in the second quarter that international capital inflows to the US will decline further, and foreign purchases may even register a net decline.

Alpha Value Research & Analysis

Influenced by the recent banking crisis, investors’ expectations for the US 10-year Treasury yield for the next three months should move downward, but mainstream views will still be for it to fluctuate within 3.4% ~ 3.6%.

Barclays

According to the Treasury International Capital report, at least 16 countries sold US government bonds in January this year, including China, Belgium, Luxembourg, Ireland, Brazil, France, Saudi Arabia, Germany, Mexico, Israel, Kuwait, Colombia, Sweden, Bahamas, Vietnam and Peru. This trend reflects the growing recognition of the negative effects of the debt-based economic model in the United States, and apparently indicates that the monetary authorities of various countries are increasingly aware of the unreliability of the US debt as a core asset supporting the US dollar.

Conclusion: BTC is heading back above $32,000

We believe that when some country’s fiat currencies collapse due to debt crisis, BTC will demonstrate its power to challenge the current debt-based financial system. As long as the size of debt continues to increase, BTC will gain an increasingly larger share as a source of capital in the debt recovery pool. In the second half of 2023, we predict that BTC will rise above $32,000 thanks to catalysts including a slowdown in inflation, easing of energy problems, a ceasefire in the Russia-Ukraine war and the reversal of the M2 supply trend.

Bloomberg, TheMarketMemo

The above factors will collectively drive the beginning of a new bull cycle. Consumers will gradually see Bitcoin as a store of value and a hedge against M2 inflation rather than a direct hedge against CPI inflation. Especially in middle regions of emerging markets that are full of frictions from multi-polarization, BTC will become one of the perfect natural alternatives to US dollar dominance. Meanwhile, if the US economy falls into a recession in one of our expectations, the Fed will likely stop raising interest rates and there will continue to be a surplus of money and deficits in government budgets.

Since competitors to the US dollar system have less power and discretion than the controller of the US dollar system, the possibility of their fiat currencies being weaponized by a few authoritarian politicians is fundamentally eliminated. In this context, Bitcoin’s narrative as a completely stateless currency makes it a more sensible choice. It is conceivable that large-scale use of Bitcoin could significantly reduce the possibility of conflicts between political interest groups.

In summary, we are at a critical turning point in the economic cycle, and while the Fed focuses all its attention on managing economic growth and inflation, it will face even greater challenges when unpredictable crises occur in the economy. In that situation, if there is no particularly negative news for cryptocurrencies, BTC will be able to go back above $32,000.