Bitcoin vs. Gold: Which is the best buy?

bodnarchuk

Bitcoin vs. Gold

One thing that I think all investors will agree on is that the economy is characterized by uncertainty at the moment. Rising interest rates with the aim of fighting inflation, fear that a banking crisis will turn into something systemically damaging, increasing oil prices due to a surprise cut by OPEC+, and recent jobs data coming in weak, all point to significant volatility in the days, weeks and months ahead. Recently, the price of Bitcoin (BTC-USD) has risen significantly, and many investors are likely to interpret this as a flight to safety. This point is further reinforced by a rise in gold prices, with gold historically serving as a meaningful hedge against inflation and other economic pain. But I look at this picture a little differently.

Although I certainly recognize that there is a lot of uncertainty in market right now, I think the drivers behind the rise in Bitcoin and the rise in gold are both very different. At the end of the day, I argue that Bitcoin is a speculative false security with no fundamental value behind it, with prices rising in response to a reduction in worries about what the future holds. While it is true that gold is good in an inflationary environment and has rallied in part due to concerns over inflation, I believe the recent upside can be attributed to shifting market demand for the precious metal.

The Rise of Bitcoin

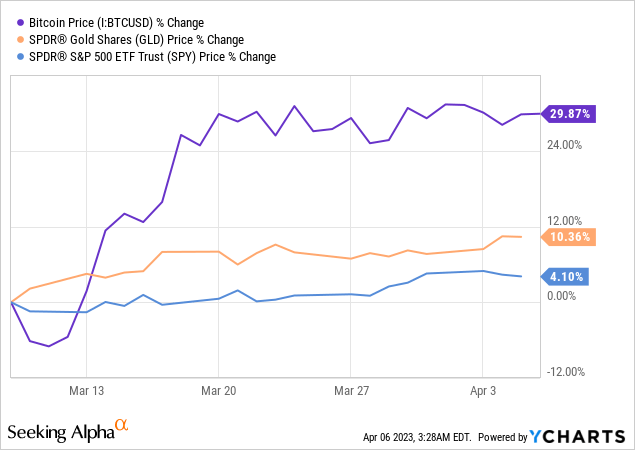

Regardless, 2023 is proving to be a great year for Bitcoin and those who have it. At the time of writing, it is up 69.4% compared to where it ended last December. It outperforms the broader market, gold and pretty much everything else. Because of the limited supply and the belief by speculators that it is similar to gold in that it acts as a store of value, it may be tempting to believe that the rally can be attributed to market participants who believe that the future will be worse than the past. Those who rely on this argument can argue, quite convincingly, by pointing out that the price of Bitcoin has risen by 29.9% since March 9 of this year. For context, March 10 was the day Silicon Valley Bank, which was owned by SVB Financial Group (OTC:SIVBQ), more or less collapsed.

The argument here is that as fears of a banking crisis spread, and the risk of further contagion increases, investors will move to safer assets to reduce potential losses should things get really bad. Using SPDR Gold Shares (NYSEARCA:GLD) ETF as a proxy for gold, upside for the commodity since then was also significant, coming in at 10.4%. In fact, this rise has pushed gold very close to its highest price reported in 2020 during the worst days of the COVID-19 pandemic. Seeing both of these increases could be all the evidence market participants need to conclude that, as has been speculated in the past, Bitcoin provides a suitable store of value in uncertain times.

However, the picture I see is quite different. Although we saw some spread of the contagion, it is now clear that regulators have the banking crisis under control. With the promise to fund uninsured deposits at the institutions that have failed, and active supervision that has led to other financial institutions absorbing the assets of the most problematic firms, it seems to me that we are nearing the end of the current crisis. So what then has been the reason for the rise in Bitcoin?

Fundamentally, I believe there is no value in Bitcoin beyond the small benefit that comes from being able to instantly transfer value from point A to point B. But that amount, I would argue, in no way justifies the prices even close to where they is today. This is something I argued for in an article last November. Although Bitcoin prices have risen significantly since then, I said there is no telling how high or low it will trade before the market finally realizes its worthlessness. That is the nature of a speculative bubble. And a speculative bubble is exactly what seems to be inflating today.

As interest rates began to rise, it became riskier to allocate capital in certain ways. As I highlighted in another article not too long ago, venture capital and other early stage capital has all but dried up over the past year or so. Interest rates make borrowing more expensive, and they make speculative endeavors more dangerous. Once the banking crisis began and regulators stepped in, it became pretty clear that the narrative about interest rates would change. Since then we have seen one additional rate increase of 0.25%. However, it seems very likely that at most we will see only a further rise this year. And by next year, if not sooner, interest rates should start to fall. Before all this happened, there were concerns that interest rates would have to continue to rise, which would also have increased the likelihood of a hard landing rather than a soft landing for the economy.

Given the speculative nature of Bitcoin, the idea that interest rates could peak lower than previously expected, and eventually begin to decline sooner rather than later, will certainly fuel the bullish nature that Bitcoin holders inherently possess. I think my argument here is further supported by the fact that since March 9th, the market, as measured by the S&P 500, is up 4.1%. With interest rates looking more dovish because of what has happened to the economy, all assets should see upside. If the move higher in Bitcoin was instead a flight to safety response, you would expect the broader market to experience a pullback. That clearly hasn’t happened.

So what about gold?

Those who disagree with me will point out that gold prices have also been on the rise. I have already mentioned this earlier in the article. The only main reason you would expect this to happen is if you anticipated further pain ahead, especially pain associated with further inflation. The prospect that lower interest rates may be forthcoming will also contribute to the idea that inflationary pressure should decrease. And if that’s the case, expect gold to fall.

Gold.org

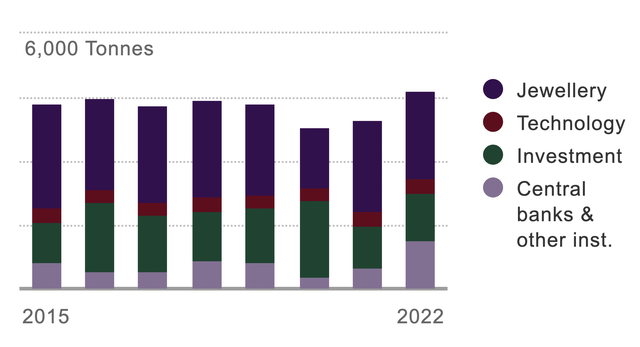

When you dig deeper into the gold data available, you start to get a completely different picture. According to one source, using data from 2022, the single largest use for gold is not an investment. Instead, it’s for jewelry. During 2022, a whopping 2,086.2 tonnes of gold was used in the jewelery sector. That equates to about 45% of all gold consumption for that year. Technology accounted for a further 308.5 tonnes, or 6.7%. In comparison, the investments comprised only 1,106.8 tonnes, and made up 23.9% of the total demand. For both jewelry and technology, these levels were below those seen in 2021. Meanwhile, the amount of gold purchased for investment rose by around 10.5%. But total gold consumption as a whole increased by about 18% year over year.

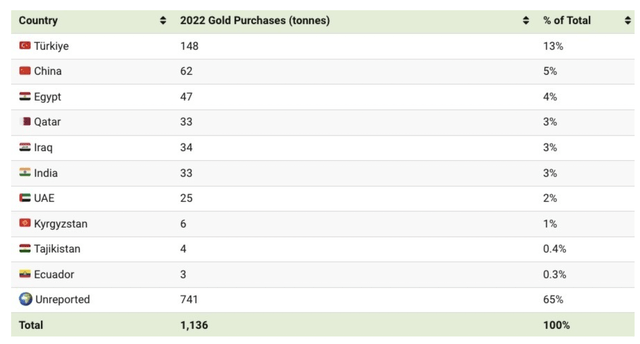

This increase was driven by a more than doubling of the amount of gold purchased by central banks and other institutions. The figure shot up 152.3% from 450.1 tonnes to 1,135.7 tonnes. This amounted to about $70 billion worth of purchases, and it marked the fastest pace of gold purchases by central banks since 1967. When you break down the data by country, you see that the single largest buyer was Turkiye, with 148 tonnes of the product acquired. This was followed by a distant second for China at 62 tonnes. While one could argue that these purchases are a flight to safety, the purchases are inherently different from the broader market’s purchases.

World Economic Forum

For example, Turkiye bought so much of the precious metal because it was trading with double-digit inflation. As of October last year, the nation experienced inflation of 86% compared to what it had seen at the same time a year earlier. The purchases made by China, meanwhile, were likely due to rising geopolitical tensions between China and the United States. There have also been allegations that both China and Russia are buying gold and not reporting it, with the aim of reducing the dollar’s influence on global trade. There is no reliable data that I can find that indicates buying trends since the end of last year. But gold prices have risen 22.4% since November 1 last year, indicating buying was likely strong heading into 2023.

Remove

Basically, I have no hope that anything positive will come out of Bitcoin. It is currently significantly overvalued and has likely risen in response to the idea that the economic environment going forward will be more welcoming to speculative activities. Because of this, I am incredibly bearish on it. Although I also recognize that prices can move significantly in either direction in the short term. Gold, meanwhile, is a little different. Strong demand from central banks as opposed to a flight to safety from investors is likely to have been the driver behind the price increase in recent months. Those who disagree with me can point out that this is a separate security. But because of the nature of the central bank, it’s a very different kind of flight than what investors would participate in. If I’m right and if the interest rate environment becomes more dovish, and assuming central bank purchases eventually stabilize rather than increase. , I could imagine that gold would fall from here. Although I have to choose between it and Bitcoin, I think the long-term prospect that investors would do well to keep in mind is gold. Even if this is the case, I prefer to have my money parked in stocks since my long-term goal is to beat inflation, not match it.

Editor’s Note: This article discusses one or more securities that are not traded on a major US exchange. Be aware of the risks associated with these stocks.