A map of the Fintech market. An overview of the sector by use case | by Medha Agarwal | August 2022

An overview of the sector by use case

In the last posts, I have talked about how we at Redpoint define fintech, why the ecosystem is important, as well as defined the universe of fintech infrastructure. In this post, I delve into a topic I’ve wanted to explore for a long time – a deeper look at the components of the fintech ecosystem and its sub-sectors (plus a market map, of course!).

As a reminder, we define fintech as any technology or business model innovation that improves the delivery of financial services.

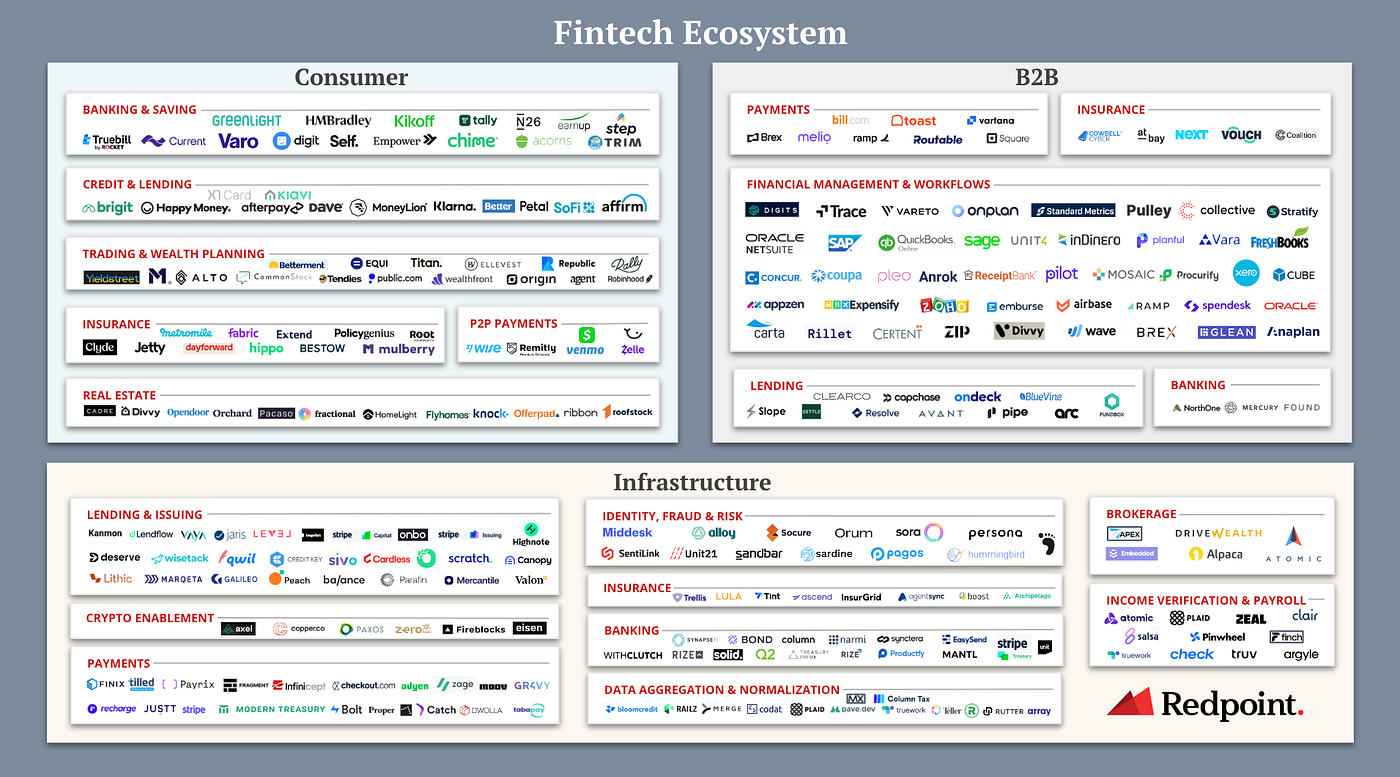

Given this broad definition, I debated a dozen different ways to segment the market before landing on the simplest and most intuitive. I see the landscape as 3 broad categories: consumer, B2B and infrastructure.

There are many ways to further segment the market. I chose to do it by use case, because that’s how the end users see the market: as needed. My hope is that this helps operators and consumers navigate the landscape of companies they can leverage for any specific need. Whether you want to find out who the players are, or see where there is white space, this market map can help you wrap your head around the many areas of fintech, how they fit together and where opportunities exist.

Consumer fintechs offer products and services to consumers. As a result, their GTM and user experience is oriented towards individuals versus businesses or developers. Within the consumer segment, there are 6 categories of companies.

Bank and savings

This category includes neobanks for consumers and savings products. The thesis here is that segments of consumers have been completely ignored or underserved by traditional institutions, so offering products more tailored to their needs will create loyalty and unlock cross-selling opportunities, thus meaningful revenue per customer. For example, Chime eliminated overdraft and account fees for users, which can amount to up to 4% of profits in traditional banks. While these fees were lucrative, they were most punitive for lower-income consumers, which is the segment Chime originally focused on serving.

58% of Americans — roughly 150 million adults — live paycheck to paycheck, according to a recent LendingClub report. By helping consumers make ends meet and ultimately save, businesses can build strong relationships with these users and monetize this emerging wealth over time, while helping to improve the lives of millions.

Credit and lending

Americans love lines of credit. 77% of Americans have some form of debt. Companies in this category offer consumers a specific type of debt — mortgages, credit cards, student loans, cash flow, etc. Like the category above, the task is often to focus on a specific segment and expand products and segments from there. SoFi, for example, started by offering lower-cost student loan refinancing options for students from top universities and has expanded into mortgages, banking and other products over time.

Trading and wealth planning

This category includes many products I review under the “financial management” umbrella. I think there is a significant trend towards consumers wanting a more active role in their finances. The rise of Robinhood, M1, crypto etc. illustrates this interest in platforms and tools that enable users to have more fine-grained control over where and how their money is invested versus more traditional wealth advisors. In conversation after conversation with millennials and Gen Z, they express skepticism about the value added by organizations that charge 1% on AUM and a distaste for models that require regular face-to-face interaction.

Companies in this category empower and empower consumers to manage their finances more actively, whether it’s stocks, taxes, options, etc. Some companies are working to put more targeted investment strategies on autopilot for lower costs (eg Wealthfront, Titan, Betterment), others provide access. to asset classes that private investors previously had no access to (e.g. Rally, Yieldstreet), and still others are trying to optimize taxes (e.g. Agent).

Insurance

Similar to the unbundling of the bank account, insurtech in recent years has seen new players offering an improved digital delivery of insurance products, characterized by better user interfaces, user interfaces and transparency. Many of these companies offer easier access to insurance products such as life, auto and homeowners/renters. Many are now also innovating on the distribution model and some on underwriting as well.

P2P payments

This segment of companies enables the transfer of money between consumers. The use case and experience vary, but the structure is similar – a consumer most often transfers money from one digital wallet to another. Venmo, Cash App and Zelle are among the most famous examples.

Property

This is a broad one. Companies in this category innovate on the experience of owning a home – whether it’s buying, selling or ownership. For example, Opendoor has made selling a home more turnkey and arguably guaranteed, while Divvy enables consumers to work towards the opportunity to buy a home through a rent-to-own financing structure.

Companies in this sector build products and services for companies. Unlike fintech infrastructure, these are applications that are most likely usable as stand-alone products versus as building blocks for others. These products are used directly by the buyer for their own workflows, as opposed to building a new product or service for their end customers. Within B2B there are 6 categories of companies.

Payments

Business to business payments continue to be an area of high friction and opportunity. It is very challenging and expensive for businesses to accept, send and manage payments today. Given the meatiness and complexity of payments, companies in this space are starting with a specific wedge, working to simplify and streamline a specific aspect of that process. For example, Ramp and Brex started by making it easier for start-ups to get their first credit card to pay faster and easier for products and services, while Melio is focused on improving invoices and non-card payments (ACH, bank transfer, etc..) .

Insurance

Companies in this category, like consumers, offer products such as cyber and P&C to their customers. Often they innovate on distribution or underwriting by focusing on underserved segments of the market.

Financial management and workflow

This category is arguably the meatiest in B2B because it encompasses the suite of products that enable businesses to manage their finances – to track, plan and account for income and expenses. This spans ERP and accounting, AP/AR reconciliation, consumption management, bookkeeping and equity management. For example, Onplan builds modern FP&A software for finance teams to make scenario planning and collaboration faster and easier, while Appzen streamlines the compliance process.

We broke this part of the fintech stack down in depth in previous posts where we went over the current state, opportunities for innovation, as well as buyer personas.

Lending

These companies lend capital to companies. Like insurance, they often build unique distribution or warranty opportunities. Settle offers invoice financing for e-commerce, while Pipe focuses on SaaS businesses.

Banking operations

These companies provide banking services to businesses. Like their consumer counterparts, companies in this category generally target underserved users and offer a more tailored experience with better user experience, integrations and products. NorthOne, for example, targets small businesses and provides them with value-added features such as integrations for more seamless synchronization of data, mobile payments and budgeting.

I have previously shared my view of the enabling infrastructure opportunity and a market map of the fintech infrastructure market and its subcategories. These companies supply the building blocks that provide power fintech use cases. This is important to emphasize – they can run traditional fintechs, but also non-fintechs that want to include financial services in their offer. This is a growing trend that I continue to be bullish on. I have grouped the landscape into nine areas of use:

- Lending

- Identity, fraud and risk

- Banking operations

- Crypto activation

- Insurance

- Data aggregation and normalization

- Payments

- Broker

- Income verification and salary

Do you like what you’ve read? Sign up for future Lag Cents posts and message me if there are any topics you’d like me to cover in the future.