Paysafe: Deep Value Fintech Opportunity (NYSE:PSFE)

AsiaVision

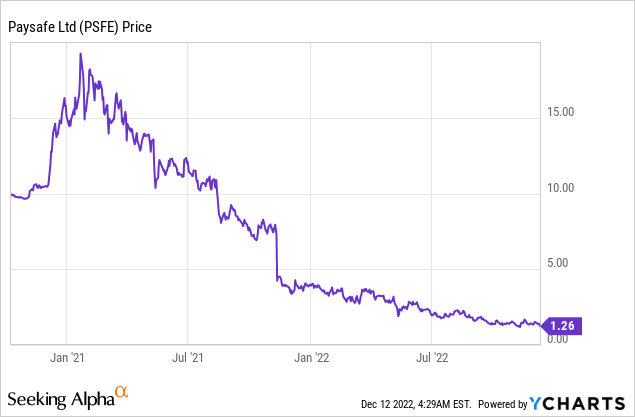

Paysafe Limited (NYSE:PSFE) is a global payments company founded in 1996, two years before PayPal Holdings, Inc. (PYPL). Since that time, the two businesses have taken massively divergent paths with PayPal growing market cap at over $83 billion and Paysafe now trades for ~$1 billion. Paysafe has had an interesting history, the company was originally listed on the London Stock Exchange, before being acquired by the world’s largest private equity firm Blackstone in 2017. In March 2021, the company was spun off via a SPAC merger with Foley Trasimene Acquisition Corp. II, on the New York Stock Exchange. Like many SPACs and growth stocks, the rising interest rate environment compressed the valuation multiple and caused the share price to plummet. Paysafe is now deeply undervalued in its own right. In this post I’ll break down the business model, economics and valuation, let’s dive in.

Business model

Paysafe offers a range of payment solutions from online payments to integrated software payments and even Point of Sale [POS]. The company also offers digital wallets “Skrill” and “Neteller.” In addition, Paysafe offers the latest authentication method for payments, called 3D Secure 2. The major card providers (Visa, Mastercard and America Express) stopped supporting 3DS 1, in October 2022. In Europe, a payment services directive [PSD] authorization was introduced in January 2021. To comply, merchants must therefore transfer their payments to the latest 3DS 2 authentication method. In the US, there is no mandate in place, but an increasing number of merchants are choosing to use the 3DS 2, to help with international payments. Paysafe is ready to take advantage of this regulatory shift towards more secure authentication technology.

Paysafe products (Paysafe website)

Paysafe also offers an interesting product solution called “Paysafecash.” This bridges the gap between offline cash and the digital world. For example, a customer can simply walk into a store and use cash to pay for online services, such as bills, loans, mortgages, etc., with the simple scan of a barcode. “Viacash” owned by Paysafe is the largest bank-independent payment infrastructure in Europe and has registered over 200,000 stores to support this solution. The service can also be used to get cashback by scanning a barcode, integrated with your banking app. The retailers registered are mainly mainland European stores such as the German supermarket chains, REWE, DM etc. Therefore, if you are not familiar with these, it would not be a surprise. Fintech giant Block (SQ) offers a similar solution in the US and has signed up major partners like Walmart to offer customers an easy way to add cash to their digital money app.

Viacash dealers (Paysafe)

Third quarter results

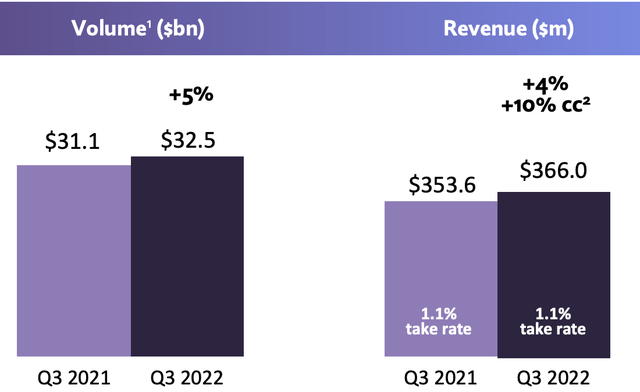

Paysafe reported strong financial results for the third quarter of 2022. Revenue was $366 million, which was up 4% year-over-year and beat analyst estimates by $13 million. This revenue growth may not seem very fast, but it was impacted massively (negative $23 million) due to unfavorable exchange rates from a strong dollar. This is because the company derives a large part of its income from Europe, but now they are listed on American stock exchanges, the company reports in dollars. On a currency-neutral basis, revenue actually increased 10% year-over-year, driven by growth in both the US acquisitions business and Digital Commerce. Payments volume increased 5% year over year to $32.5 billion.

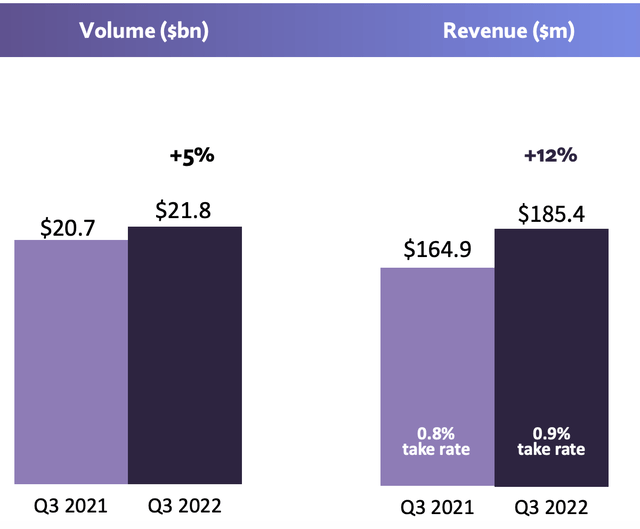

Paysafe payment volume and income (Q3.22 report)

Breakdown of revenue by business segment was $21.8 billion, up 5% year over year. Revenue was $185.4 million, a strong 12% increase from the previous year. This was driven by a 0.1% higher take rate (0.9%), which was driven by strong growth and expansion into the US SMB retail market.

The US gets revenue (Q3.22 report)

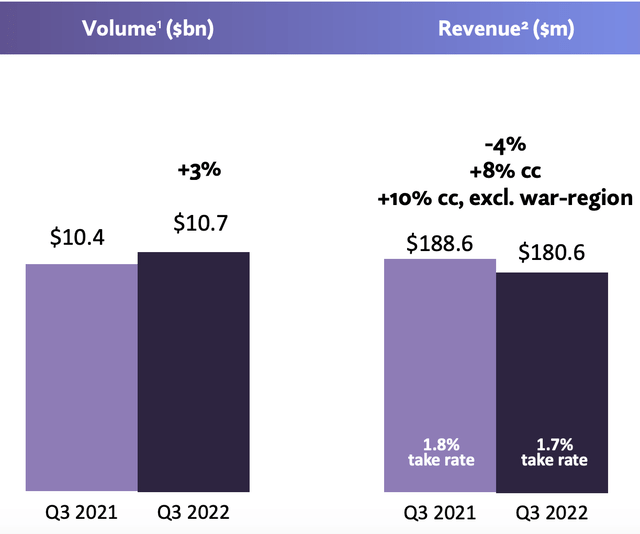

Paysafe’s Digital Commerce business reported $10.7 billion in payment volume, up just 3% year-on-year. Revenue was $180.6 million, which was actually down 4% year-over-year. However, it should be noted that this was primarily driven by the aforementioned unfavorable exchange rates and affected in war regions such as (Ukraine/Russia). On a constant currency basis, revenue was actually up 8% year-over-year. Excluding the war region, constant currency revenue increased 10% year-over-year.

Paysafe digital commerce (Q3.22 report)

The company also reported growth in its digital wallet business, which was up 2% year-over-year. Total deposits increased 9% year over year and 100,000 new accounts were funded in the third quarter.

Breaking down results by region, the company launched with 10 new merchants in Latin America and with the iconic bet365 gambling company in Mexico. The iGaming market was also strong in North America with over 45% revenue growth in the third quarter. Paysafe is currently live in 23 states, the business recently launched in Kansas with DraftKings, Caesars and PointsBet. Over the next few quarters, Paysafe plans to launch in Maryland and Ohio.

Profitability and cash flow

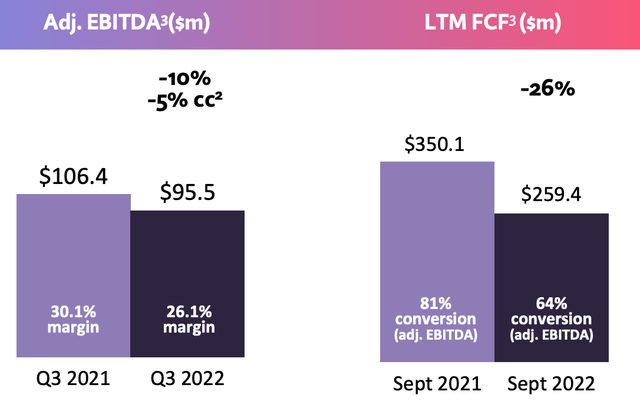

On a GAAP basis, Paysafe finally became profitable, reporting a net income result of $1 million, which was significantly better than the negative $147 million generated the previous year. This growth was mainly driven by an intangible “impairment” charge. Adjusted EBITDA was $95.5 million which was down 10% or 5% on a constant currency basis. This was mainly driven by higher interest costs. Overall, the company reported Non-GAAP earnings per share of $0.04 which beat analyst estimates by $0.02.

Adjusted EBITDA (Q3.22 report)

The business reported $259.4 million in free cash flow for the trailing 12 months, with a conversion ratio of 64%. Going forward, the company expects a 60% to 70% adjusted EBITDA to cash flow conversion ratio. The company has a robust balance sheet with $220.2 million in cash and short-term investments. The company has high long-term debt of $2.2 billion, but only $10.2 million of this is current debt, due within the next 2 years.

Advanced valuation

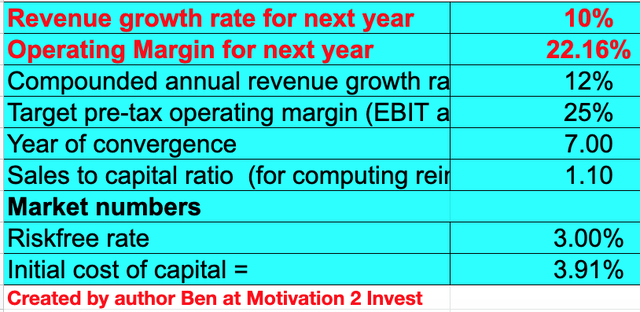

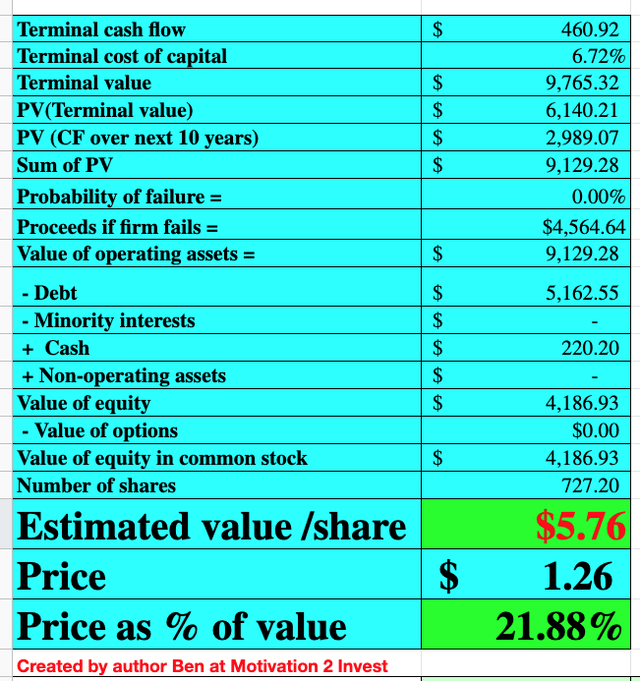

To value Paysafe, I plugged the latest economics into my advanced valuation model, which uses the discounted cash flow (“DCF”) method of valuation. I have forecast 10% revenue growth for next year, which is similar to this year on a constant currency basis. However, in years 2 to 5, I have forecast a slight improvement to 12% p.a., as economic conditions are likely to improve.

Paysafe share assessment 1 (Created by author ben at Motivation 2 Invest)

The company also has a healthy pre-tax operating margin of 22.16%. I have predicted that this will increase to 25% over the next 7 years as the business continues to scale and execute a greater number of upsells.

Paysafe share assessment 2 (Created by author Ben at Motivation 2 Invest)

Given these factors, I get a fair value of $5.76 per share. The stock is trading at $1.26 per share at the time of writing, making it ~78% undervalued, which is significant.

Note: Paysafe has a meeting in December 2022 to seek shareholder approval for a 1 to 12 reverse stock split. Since Paysafe’s share price has fallen to just over $1, this would make sense to make the company look safer to investors. However, it should be noted that this is mainly a psychological difference.

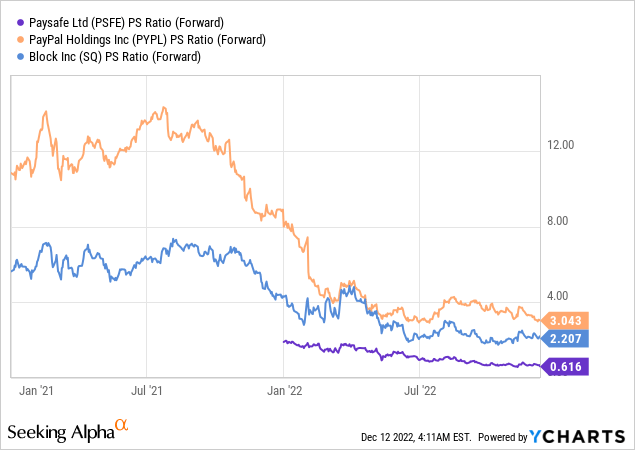

As an additional data point, Paysafe trades at a price-to-sales ratio = 0.62 which is cheaper than historical levels. In addition, Paysafe trades much cheaper than fintech peers such as Block and PayPal, even though these businesses are significantly larger.

Risks

Recession/payment volume

The high inflation and rising interest rate environment has led many analysts to predict a recession. During a recessionary environment, both consumers and businesses have their input costs squeezed, which generally results in lower expenses and thus lower revenues for fintech companies.

Final thoughts

Paysafe is a global fintech company that continuously renews its product range. The company faces headwinds from unfavorable exchange rates and the macroeconomic situation. However, the business still managed to grow its finances steadily in the third quarter. Paysafe’s shares are significantly undervalued at the time of writing and can therefore be a great long-term investment.