Greyscale Bitcoin Trust: Cathie Wood Is Right, Finally (Rating Upgrade) (GBTC)

Marco Bello

Two new fears directly related to the FTX collapse are widening the discount to the NAV of Grayscale Bitcoin Trust (OTC:GBTC). This fear has exacerbated fundamental price declines from the ongoing correction in Bitcoin (BTC-USD) as well as a decline related to the Trust’s regulatory setback this summer. But much-maligned Cathie Wood maintains her conviction in the blockchain thesis and the Trust; Ark Invest has tactically added around 450,000 shares in the Trust to its holdings since the FTX bankruptcy.

From my perspective, Wood’s timing on GBTC additions is almost right. This is especially true for those with a longer horizontal allocation to digital assets and as an earmarked part of the core holdings of Bitcoin. And the article below describes three arguments for why the current discount to NAV represents an opportunity for those who are willing to waive their own custody:

- Questions regarding the trust’s reserves are unwarranted, and the extensive recent FUD from both crypto and mainstream media is exaggerated. Coinbase (COIN) Custody is a literal and figurative fortress. From a trust standpoint, Coinbase has simply been rated differently than FTX.

- The foundation’s discount to NAV will probably be reversed in the end. There are a couple of mechanisms, but a reasonably likely and short-term solution relates to the trust’s litigation against the SEC regarding its proposed transition to an ETF. Legal pundits believe the court could find the SEC discriminated against the Grayscale transition of an ETF compared to “equivalent” Bitcoin futures ETFs.

- Both Grayscale and Genesis are subsidiaries of Digital Currency Group. The lending arm of Genesis is facing a liquidity event and rumors of bankruptcy. Genesis is also facing a securities investigation likely related to its lending activities. Uncertainty and bad news reign, but the direct blowback on Grayscale and Trust’s pricing in the long term may be somewhat exaggerated and limited by legal, technical and practical reasons.

Greyscale Bitcoin Trust: Trusting Coinbase Custody

A Nov. 18 blog and email from Grayscale set off a firestorm of criticism when the company stated it would not publicly provide proof of reserves for its money.

Due to security concerns, we do not make such wallet information and confirmation data publicly available through a cryptographic reservation certificate or other advanced cryptographic accounting procedure.

Safety, security and transparencygrayscale.com, 18 Nov. 2022

In the days following the collapse of FTX, Binance CEO Changpeng Zhao had argued that industry participants should eventually publish a Merkle tree-style proof of reserves and started the process of providing wallet addresses, quantity and block heights for Binance’s major companies.

All assets held under Grayscale’s digital asset products are held by Coinbase Custody. Coinbase has already used a more traditional way of proving assets, although they also use some cryptographic proof. As publicly listedUS-based company, their financials are externally audited on a quarterly basis and a comprehensive annual report is submitted to the SEC.

When external auditors come in to look at our cold storage reserves, they randomly sample addresses that we claim to own, and require us to move those funds to demonstrate ownership, through our key signing ceremony.

How crypto companies can provide proof of reservescoinbase.com, 8 Nov 2022

Coinbase was founded in 2012 by Brian Armstrong. Both the company and Armstrong have been scrutinized over a relatively long period. There is no record of credit losses from any financing activities or a record of exposure to customer or counterparty insolvency. There is also no real fear that the Grayscale assets could be entangled in a Coinbase bankruptcy. Consider the following:

- Coinbase is not going bankrupt. In addition to maintaining strict 1:1 customer holdings, the company itself at the end of Q3 had $5.6 billion in near-cash and over $600 million in digital assets. The obligations amount to just over $4 billion, of which $3.4 billion is conservatively financed, long-term debt. Finally and most importantly, it now appears that Coinbase will operate within its $500 million EBITDA range for this year.

- If Coinbase were to go bankrupt, the likely interpretation of Uniform Commercial Code Article 8 would be that the customer’s assets are not Coinbase’s property and cannot be claimed by its creditors.

- Assets in escrow can be further removed from creditors by not being listed on the balance sheet, as platform user assets are under Staff Accounting Bulletin 121 from the SEC.

Coinbase has been and is storing Grayscale’s digital assets safely.

Grayscale’s lawsuit against the SEC

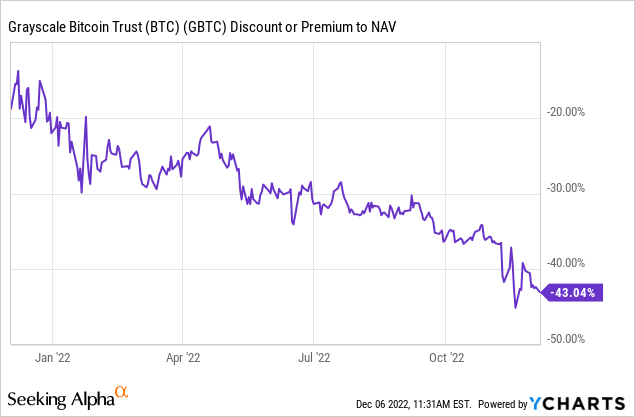

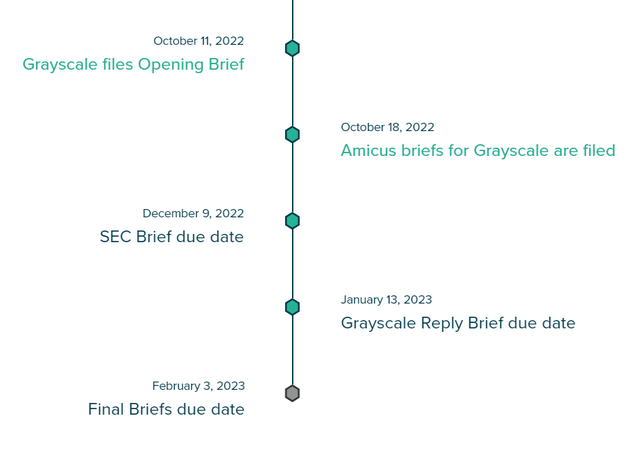

Over the summer, the SEC rejected Grayscale’s proposed conversion of its Bitcoin Trust into a spot-backed Bitcoin ETF. Trading as an ETF will provide a mechanism for the product’s price to adjust to the holding value and remove the 43% discount to NAV. Grayscale has filed for review of the SEC decision at the United States Court of Appeals for the DC Circuit. If Grayscale wins the lawsuit, the SEC injunction would be lifted and the trust would likely be allowed to convert to an ETF.

Grayscale’s main argument in the lawsuit is that the SEC is acting arbitrarily because its conversion proposal is treated differently than “equivalent” Bitcoin futures ETFs. In the opening letter, Grayscale’s explains:

In approving bitcoin futures ETPs, the Commission necessarily determined—as required by the Exchange Act—that the risk of fraud or manipulation in the spot bitcoin market (which directly affects the price of bitcoin futures) was sufficiently low that bitcoin futures ETPs can be approved without creating unacceptable risk for investors. But this risk is exactly the same for spot bitcoin ETPs as the one proposed by the Trust. It was completely arbitrary for the Commission to conclude that any such risk was no bar to approving bitcoin futures ETPs and then reverse course and find the same risk too great to allow spot bitcoin ETPs to be approved.

Grayscale v. SEC, Card from the complainant10/11/22, p. 24

Put differently and more succinctly, Grayscale has argued the following:

If the exchange’s monitoring sharing agreement with CME is sufficient to detect and deter fraudulent or manipulative activity in spotbitcoin markets, spotbitcoin ETPs and bitcoin futures ETPs are equally protected against such activity.

Grayscale v. SEC, Card from the complainant10/11/22, p. 32 (link above)

Greyscale’s argument above has received meaningful support from neutral legal pundits. In previous filings, however, the SEC has not directly, or at least at any length, addressed this “discrimination” idea. The commission’s first response letter to the court must now be delivered on 9 December. And it will be necessary for Trust investors to carefully examine and weigh any new and more direct language from the SEC on this central and likely crucial topic.

grayscale.com

But regardless, and regardless of the outcome of the lawsuit at this level, for long-term owners there are a couple of theoretical future scenarios that could drive a reversal of the discount, such as redemptions. And overtime there is a natural tendency for a financial product to trade at the price of its underlying holdings. So Grayscale Bitcoin Trust offers an interesting opportunity for time arbitrage with its current 43% discount on the holding value.

Greyscale: Genesis Connection

Digital Currency Group is a venture capital firm in the crypto sector and parent of both Grayscale and Genesis. Genesis is one of the largest OTC trading desks in the space and a significant institutional lender; in 2021, the company handed over $170 billion in trading volume and had $130 billion in lending.

On November 16, the lending arm of Genesis suspended redemptions and new loans. DCG CEO Barry Silbert explained the action in a letter to shareholders. The letter is via CNBC and can be found included here.

…market turmoil triggered unprecedented withdrawal requests. This is a question of liquidity and duration mismatch in the Genesis loan book.

Letter to DCG shareholders, Barry Silbert, November 2022 (link above)

In the days following the collapse of FTX, a general trend in the sector was characterized by investors taking their cryptos from trading platforms and removing them from return programs; put another way, the FTX collapse led to this cycle’s “not your keys, not your crypto” moment.

Note that Genesis is a lending partner for the Gemini exchange’s Earn program. So retail investors whose digital assets were engaged in the Earn program at Gemini cannot redeem their money.

So how are shades of gray involved in all of this? Although nuanced, Genesis is now a meaningful creditor of DCG.

….DCG has borrowed money from Genesis Global Capital as have hundreds of crypto investment companies. These loans were always structured at arm’s length and priced at current market interest rates. DCG currently has a commitment to Genesis Global Capital of ~$575 million due in May 2023.

…You may also recall that there is a $1.1 billion promissory note due in June 2032. As we shared in our previous shareholder letter in August 2022, DCG stepped in and assumed certain obligations of Genesis related to Three Arrows Capital’s default.

Letter to DCG shareholders, Barry Silbert, November 2022 (link above)

Note Three Arrows filed for bankruptcy in July as a result of the selloff in the crypto sector spurred by the collapse of LUNA (LUNC-USD) in May. So while DCG technically owes Genesis, the parent company took over the troubled Three Arrows assets from the subsidiary and is now in the creditors’ committee for the Three Arrows liquidation proceedings.

DCG and its subsidiaries reportedly own approximately $1 billion of Bitcoin Trust themselves. So there are fears in the market that shares could be liquidated to speed up repayments to Genesis and allow them to meet short-term obligations. The size of these sales will be significant enough to both move the Bitcoin price and extend the Trust’s discount.

But I think it is unlikely that DCG will be forced to sell its Trust holdings at a discount. DCG is a large, robust and long-standing member of the space. In addition to Genesis and Grayscale, other subsidiaries include Foundry, which operates one of the largest Bitcoin mining pools, as well as CoinDesk, a top media company in the crypto sector. DCG is also invested in over 200 companies and funds, an overview can be found here.

Interestingly, Gemini updated its Earn customers and explained how the situation can play out.

Liquidity problems can be solved in a number of ways, including raising capital, raising debt and/or restructuring existing debt. For example, raising capital may involve Genesis selling equity in exchange for cash. Debt restructuring may, for example, mean that DCG agrees to pay off its loans to Genesis earlier. All these possibilities can take time.

Gemini Earn updatesgemini.com, 12/6/22

Fears of large sales by DCG of their Greyscale Bitcoin Trust holdings may turn out to be overblown as Genesis and DCG have other means of obtaining liquidity.

Grayscale Bitcoin Trust Rating

The trust’s discount to NAV has grown since the SEC’s rejection order in July for the conversion to an ETF. Contagion from the FTX collapse has further accelerated this divergence.

But Grayscale’s current lawsuit against the SEC is a first bite at the reversal apple. And fears triggered by the FTX drama may show blow over. First, despite not providing a Merkle tree-style public proof, Grayscale’s digital assets are safe and secure with Coinbase Custody. Second, Genesis and DCG may successfully raise capital or debt rather than sell their holdings in the Trust at a discount for short-term liquidity.

I am moving my rating for Trust from hold to buy based on the now 43% discount to NAV. This assessment applies to those who have a long horizontal allocation to Bitcoin and who choose not to self-custody.