African credit-led fintech Finclusion raises additional capital amid rebrand • TechCrunch

African credit-led neobank Finclusion Group has raised an additional $2 million in equity funding as it officially rebrands as Fin, the company said in a statement shared with TechCrunch.

The news follows an announcement in January that the fintech, which uses AI algorithms to provide financial services to African customers via a range of credit-centric products, raised $20 million in debt and equity before Series A funding. Fin also raised a $20 million debt facility from emerging markets debt provider Lendable in September 2021, bringing total capital secured in equity and debt to $42 million.

Per the statement, the new equity financing — led by existing investors Leonard Stiegeler, who also joins the company’s board along with Sudeep Ramnani and Jai Mahtani — will be used to adding new, fully integrated territories to its operations, as well as developing new offerings, especially in third-party support for microfinance banks that want to offer more financial services.

African customers are in dire need of credit. But from the long-term perspective of a company that only offers loans, it can be difficult to compete with other lenders that offer deposits and investments, financial services that any lender, backed with years of customer credit history, can effectively cross-sell.

Since 2018, Fin, taking a cue from other credit-first neobanks, has been building consumer-facing credit products to close the credit gap in the countries where it operates, including Tanzania, Namibia, South Africa, Eswatini and Kenya. Its offerings are also diversified. It is SmartAdvance, where Fin, via employer partnerships, offers solutions for employees’ financial well-being. Their payroll product provides payday loans and future payday loans where employees can take loans on the back of their paychecks, deduct them from payroll and lend through employer relationships. There’s an insurance product too, with savings products, cards and buy-now-pay-later deals via a merchant network still in the pipeline.

Fine

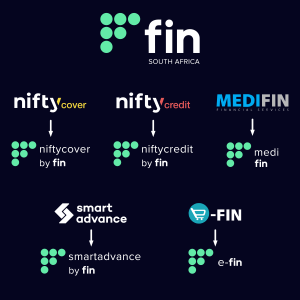

With this rebrand, subsidiaries across core markets have also been renamed: Fin Kenya (formerly TrustGro), Fin Tanzania (formerly Fikia Finance) and Fin South Africa (with their products now SmartAdvance by Fin, NiftyCredit by Fin, NiftyCover by Fin, MediFin and e-Fin). Fin’s plan is that the consolidation of its footprint across Africa under this identity will highlight its ambition to dominate the neobank space in East and Southern Africa, which has seen players such as TymeBank, Kwara, Koa and Fingo emerge in recent years.

“Our cross-selling experience was limited when we first launched,” co-founder and co-CEO Timothy Nuy told TechCrunch over a call. “So effectively through this integration everything becomes Fin. Someone will log into his Fin South Africa platform and effectively access all the financial services we offer in the country that they need, making it easier to drive repeat engagement and for to ensure that customers have full visibility of our offer, but also the financial products they have outstanding.”

In the last couple of months, Fin has improved his numbers. For example, the loan book has increased by 30% from last year, with over 40,000 unique customers, said Tonderai Mutesva, the startup’s co-founder and CEO. They pay interest of 24-42% APR depending on the product type and market. Default rates on loans still fall between 7-8%, but Mutesva said fintech is working to bring it down to around 3%.

What’s next for the brand? A planned expansion into new markets next year, and then offering services to microfinance banks that will improve their value proposition to customers; for example, better credit or savings tools. The technology behind this offering will be known as Fin Connect and is backed by Fin’s previous acquisition of microfinance technology service provider Awamo. Finally, Fin says it will continue to support adjacent businesses in the area through its venture portfolio, one of which is Kenyan insurtech platform m-Tek.

“The real goal is to reassess what we need to do in 2023, integrate all the brands and continue to just scale up our loan portfolio as well as bring more of these businesses to balance on an operating income basis,” Nuy said. “When it comes to raising capital, we will probably carry out a larger capital raising towards the end of 2023.”