Crypto Lender Genesis Contagion Continues – Bitcoin Magazine

Below is an excerpt from a recent issue of Bitcoin Magazine Pro, Bitcoin Magazine premium market’s newsletter. To be among the first to receive this insight and other market analysis on the bitcoin chain straight to your inbox, Subscribe now.

Genesis is looking for liquidity injection

If you don’t know about Genesis Trading, maybe you should. They represent the backbone infrastructure of the institutional investor base in bitcoin and broader crypto markets. For lending, trading, hedging, stock returns and more, Genesis Trading was the brokerage to facilitate all of this activity in the space. Remember the juicy returns from BlockFi and Gemini Earn products in space? Genesis is the intermediary between these platforms and the hedge funds to generate that return.

Genesis held a short customer call to announce the suspension of redemptions, withdrawals and new loans. With exposure to FTX and Alameda Research, the company now needs a fresh infusion of liquidity after having nearly $175 million locked up in a trading account with FTX. As an initial response, parent company Digital Currency Group (DCG, the parent company of Grayscale), injected $140 million into the business to keep operations afloat. Nevertheless, Genesis is now trying to find more capital. That’s the reason Gemini Serve had to stop withdrawals.

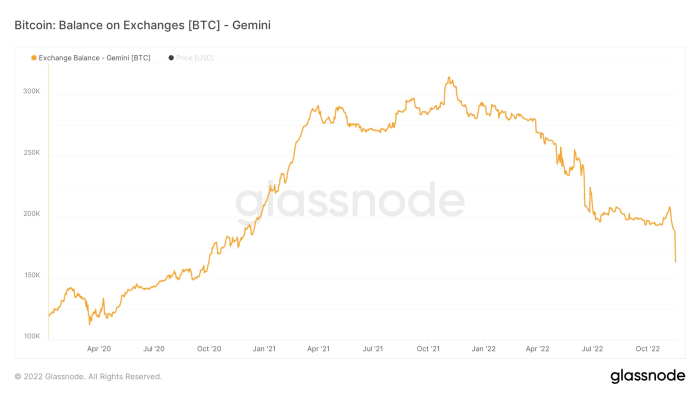

Although Gemini has stated that the rest of their business is operating normally, limiting the Gemini Earn product and having service outages on the platform seems to have triggered a small rush to get bitcoin out of the exchange: 13% of the total bitcoin balance has left within the last 24 hours. As we have highlighted before, exchanges are not the place for your bitcoin, especially when there is a high probability that there is another exchange (or even several) left to fall.

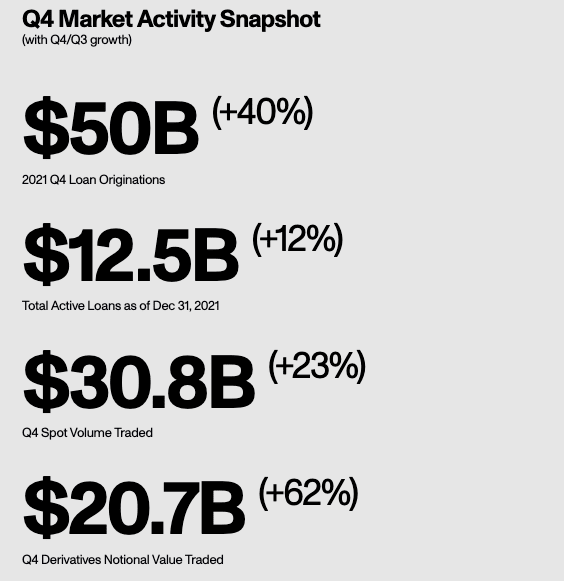

To give you an idea of size, Genesis had $50 billion in loan originations in one quarter and an active loan book of $12.5 billion at the top of the market back in 2021. Still, both loan originations and the active loan book took a hefty haircut , falling to $8.4 billion and $2.8 billion respectively in the third quarter of this year. Back in July, Genesis filed a $1.2 billion claim against Three Arrows Capital that was picked up by DCG to keep the hit off Genesis’ books. Loans were partially secured with shares of GBTC, ETHE, AVAX and NEAR tokens.

Source: Genesis Quarterly Report

We know from on-chain activity like Genesis had tons of interactions with Alameda, Gemini and BlockFi through their OTC trading desk; FTT was also a top token received and sent in that activity. Without Genesis sharing more details, we don’t know the extent of the exposure and capital needed to make the customers whole. Nevertheless, the fact that the parent company DCG has not already stepped in to provide a new injection of liquidity is a warning sign of where this could end up. News appeared as Genesis is seeking a $1 billion credit facility immediately. Not good.

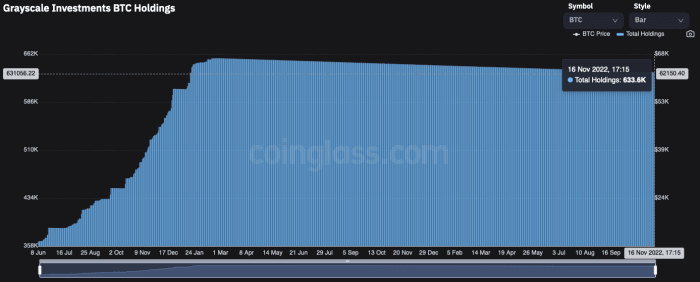

In the worst case scenario, the lack of funding provided by DCG may raise questions about available liquid assets. DCG and grayscale have dissolved trusts before and that option is not off the table. It’s an unlikely path, but certainly one to highlight as Grayscale is the largest holder of bitcoin via the Grayscale Bitcoin Trust, with nearly 633,600 bitcoin. This could easily be a regulatory issue or some other limitation (of which we do not know) where DCG cannot provide the capital to Genesis.

Source: Coinglass.com

Circle, the issuer of stablecoin USDC, also has ties to Genesis. Nevertheless, they highlight that their Circle Yield product amounts to only 2.6 million dollars in outstanding loans with collateral which, if true, is quite insignificant.

We will likely hear more about the state of Genesis in the coming days as they want/need the capital injection by Monday. This will be a massive hit to a laundry list of institutions in the industry whose withdrawals remain suspended and funds tied up. Genesis reflects the exact reason why the general contagion from the FTX and Alameda Research collapse has yet to play out. Defaults and insolvency come in waves, not all at once. It takes weeks and months to see where the biggest holes are and who has liquidity, counterparty and/or insolvency problems.

On top of that, almost all major players and market makers have sourced their cash from exchanges to strengthen their own balance sheets and reduce counterparty risk. Liquidity in the market is thin and the time is ripe for volatility. Although the market has appeared to find a temporary bottom amid all the negative news headlines over the past week, the unknown downside risk still far outweighs the upside potential in the short term.

Relevant previous articles: