Ethereum Leads as Crypto Outperforms Stocks, Bonds in Q3 (ETH-USD)

proxyminder/iStock not released via Getty Images

Bloomberg’s US edition published an interesting piece last week highlighting crypto’s remarkable third quarter outperformance. Cross Asset Markets editor Joanna Ossinger pointed out Bitcoin’s (BTC-USD) relative stability and Ethereum’s (ETH-USD) reversal compared to retreat in both MSCIs (ACWI) share index for all counties and Bloomberg’s global bond index with total return.

| Bitcoin | Ethereum | ACWI (all-country shares) |

LEGATRUU (global bonds) |

|

| Q3 Change | 3.7% | 32% | -7.0% | -7.0% |

Obtained from: Crypto remarkable quarterly performer with Bitcoin going higherbloomberg.com, 29/9/2022

Two takeaways from the article are the key role sovereign bonds play in the crypto space and how Ethereum is providing leadership to the sector. The article below elaborates on these two points with a view to the fourth quarter ahead.

Ethereum: Now The Surge and The Verge

Looking back, The Merge on the Ethereum platform was implemented frictionlessly. The merger took Ethereum from its energy-intensive proof-of-work consensus mechanism to an ESG-friendly proof-of-stake method of securing and spreading the blockchain. This change likely allows for additional institutional investment. Darius Sit of QCP Capital provided the following color to Bloomberg:

The Ethereum merger was a strong account for the third quarter of 2022… Although we saw a drop in prices after the merger, the success of this watershed event bodes well for the space.

Crypto remarkable quarterly performer with Bitcoin going higherbloomberg.com, 29/9/2022 (link above)

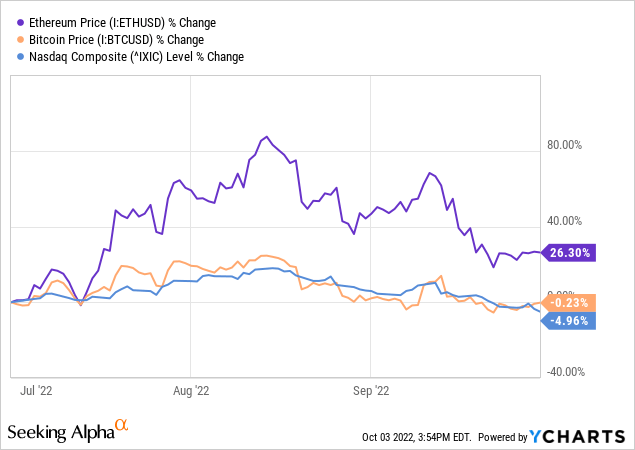

Consider Ethereum’s price movements over the third quarter in the graph below. They appear to be correlated to Bitcoin and the interest-sensitive Nasdaq Composite, but significantly more positive during the successful practice merges on the major test nets in July and August. Also note that the oft-predicted “sell news effect” of The Merge appeared to play out in mid-September.

But where from here? First, the importance of Ethereum’s move away from proof-of-work cannot be overstated from a regulatory standpoint. The last one White Houses mandated report on digital assets by executive agencies called for minimization of greenhouse gas emissions from cryptoassets. It went further and even proposed a ban on proof of work if actions through DOE efficiency requirements are not sufficient.

… the administration should explore executive action, and Congress may consider legislation, to limit or eliminate the use of high-energy-intensive consensus mechanisms for mining cryptoassets.

Climate and Energy Implications of Crypto Assets in the United Stateswhitehouse.gov, 9/2022

Consider how regulation could directly affect the two largest digital assets. Bitcoin has a small but differentiating advantage over Ethereum, as it is less directly attackable from securities regulation. This is because Bitcoin does not have well-known, central promoters who benefited from the initial distribution coins.

But Ethereum is much more resilient from an ESG perspective as its energy usage is minimal. Bitcoin mining is increasingly using renewable energy, providing stability to the grid and encouraging new wind and solar projects. But many US lawmakers and regulators have indicated that Bitcoin’s increasing energy use is more problematic and questioned the network’s relative societal benefit. And any regulatory action against the miners is likely to negatively affect the underlying coin price, as seen during the mining operation in China last year.

Ethereum can also benefit from the next step in its development. Over the next six months, the platform should see a cleanup upgrade that includes one of the last key elements of The Merge, which is the enabling of withdrawals from the newly implemented staking mechanism. Although there are workarounds and derivatives, currently staked Ethereum cannot be withdrawn from the mechanism until this date-uncertain upgrade is implemented.

Enabling withdrawals removes a current buzz about rivals such as Cardano (ADA-USD) having longer standing, fully functional staking protocols. But more importantly, enabling withdrawals should eventually lead to something of a betting renaissance. When the institutions are guaranteed liquidity conditions, there will be increased interest in Ethereum. The platform will then be somewhat regulatory fully entrenched and provide the opportunity to safely capture meaningful dividends through staking.

twitter.com/vitalikbuterin

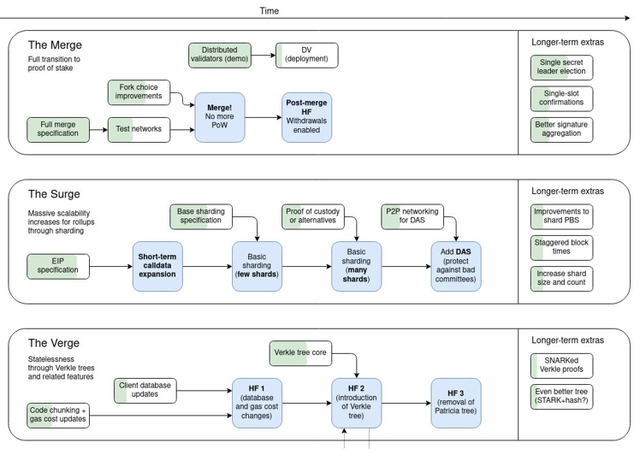

While the implementation of a merge on the various testnets was not without problems, The Merge on the Ethereum mainnet was initially without problems. This lends credence to the idea that the next two major milestones, The Surge and The Verge, can also be effectively implemented. This is not to say that the process will be quick, and there are some indications from developers that the process will be slow for both practical and technical reasons.

But every six months or so we could see a series of improvement proposals implemented that represented steps towards the milestones. The Surge is particularly important as it provides sharding, which increases the scalability of the platform and the capacity of transactions per second. The Verge will reduce the cumbersomeness of the proof-of-stake mechanism and will likely lead to increased decentralization, a pillar of digital asset value.

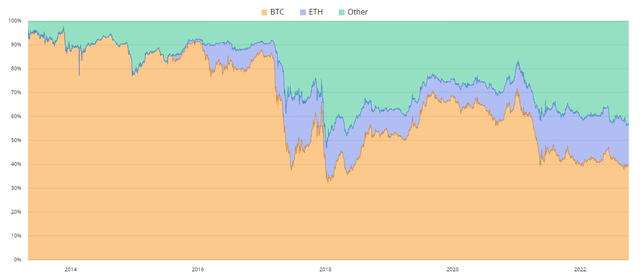

Bitcoin dominance over time (btctools.io)

The graphic above shows the percentage of the total market capitalization of the crypto space over time for Bitcoin (orange), Ethereum (blue) and altcoins combined (green). While not without volatility, Ethereum should continue to take shares and provide leadership for the sector. The paddle wheel with development upgrades and tests provides a constructive price environment in the next year. Cici Lu of Venn Link Partners Pte explained in the Bloomberg article:

While prices are depressed, the crypto ecosystem is actually booming… Developers are focusing on building the technologies.

Crypto remarkable quarterly performer with Bitcoin going higherbloomberg.com, 29/09/2022 (link above)

Interest rates: The Great Reset

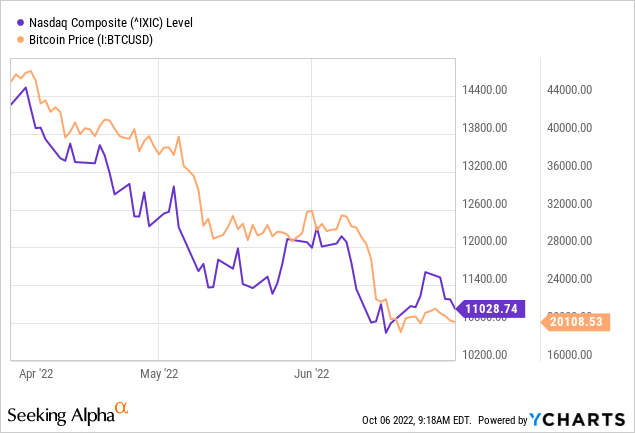

In contrast to these developments is interest rate and inflation focused US immediate policy tightening. This was particularly true in the second quarter of this year. And remember that higher prices make long-term bets less attractive and that the previously loose monetary policy supported asset pricing, including for the digital ones.

The biggest pain for the broader tech market and the crypto space came especially during the second quarter of this year as interest rate expectations were significantly reset. Consider the 3,000 point drop in the Nasdaq and Bitcoin’s drop to current levels from $44k over just three months.

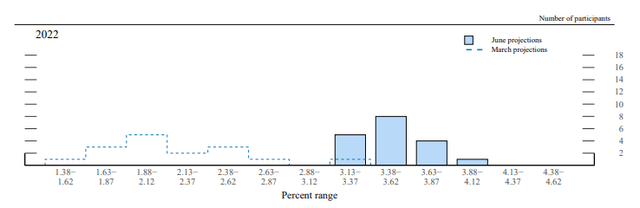

The largest portion of this year’s change in interest rate expectations can be seen in the FOMC’s summary of economic projections released with its June meeting. The median participant significantly adjusted its outlook from a target rate at the end of 2022 close to 2%, to one above 3.5%.

The dashed line below represents the estimates from the March meeting, and the shaded area is the estimates at the time of the June meeting; the scale on the right is the number of members making the projection in question, i.e. a map display of two meeting dot plots. Most importantly, during the quarter, the stock, bond and crypto markets observed, accepted and priced this new interest rate paradigm.

FOMC Participants’ Target Areas – Fed Funds (federalreserve.gov)

Digital assets in the future

Edward Moya of Oanda Corp. described the current short-term thinking on rates and cryptoassets in the Bloomberg piece.

It seems that Wall Street believes crypto is near the bottom and will become an attractive diversification strategy once the peak in Treasury yields is in place.

Crypto remarkable quarterly performer with Bitcoin going higherbloomberg.com, 29/09/2022 (link above)

A growing perception among market players is that the once flat-footed Fed has now caught up in the inflation battle. The FOMC’s historic actions at the last three meetings may now actually turn out to be far too hawkish, as there is some lag in policy effects. With the federal funds rate set to exceed 4% by the end of the year and well above the long-term neutral rate, the market has some hope that the worst increases have now been priced into risk assets. Put another way, the current and planned rate increases are considered to be sufficient to reduce demand throughout the economy and thus reverse the established price increase.

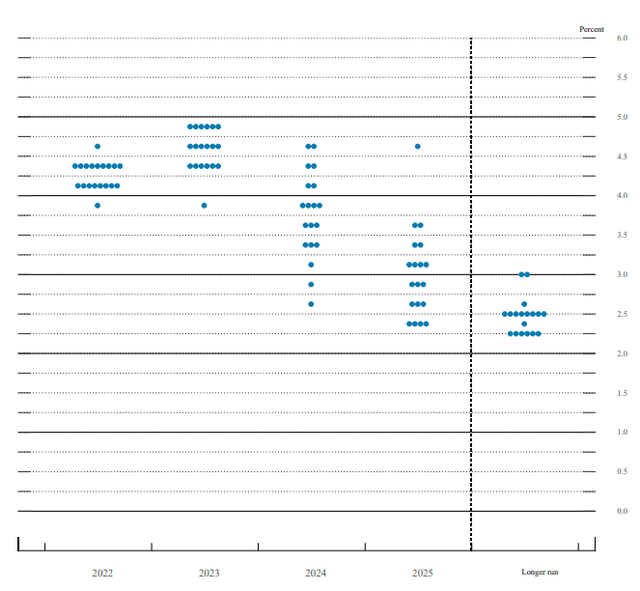

Note the topping of member expectations below 5% for the federal funds rate next year in their latest FOMC dot plot.

September Fed Funds Dot Plot (federalreserve.gov)

However, both recent CPI and PCE reports show high, entrenched energy prices, continued acceleration in food price growth and now surprisingly high core inflation. Falling US gas prices are likely to reverse with this week’s OPEC decision to cut production. And there is still great uncertainty about where energy prices will settle over the next six months given US policy on Russian natural gas and oil exports. A short but detailed piece from the International Energy Agency on projected tight 2023 natural gas supplies can be found here.

If inflation does not recede, continued negative real interest rates will likely force further tightening beyond what is currently expected, which could lead to another meaningful correction in tech and crypto assets. Furthermore, I have admittedly been wrong this year about inflation and surprised by the Fed’s powerful talk and repeated meaningful actions. All that being said, there’s a solid argument that we’ll soon be peaking in Treasury yields, as the Fed’s heavy dose of previous hikes is likely to reverse inflationary trends. Coupling this outlook with the exaggerated correction in the second quarter, I maintain my Buy rating on Bitcoin and Ethereum.

My new marketplace service is coming soon. Complete Crypto Analytics will launch in the near future and will have an in-depth analysis of Ethereum development process. Keep reading my articles here for updates so you can reserve your spot as a senior discount member. There will be a generous introductory price for early subscribers. Thank you for following my work.