This post was originally published in FIN, the best fintech newsletter; subscribe here.

A debate that has swirled around for years is whether fintech’s innovation can really help minority and underbanked consumers, or whether fintech is largely a 21st-century costume for financial predators that have been around for decades. (This post deals primarily with the US experience, but it is a global issue, especially in Latin America and Africa).

A critical issue is access: given that the underbanked typically have lower access to broadband and mobile phones than the rest of the population, it is not obvious that cutting-edge technological solutions will reach them more effectively than traditional banks and legacy money transfer services (such as Western Union and MoneyGram). And, as has been covered extensively, banking services for black Americans have been shameful at best; it is little surprise that nearly half of black households remain unbanked or underbanked.

But the evidence is now overwhelming that fintech is reaching the underbanked and other populations marginalized by traditional banking.

The best measure of this is the Federal Deposit Insurance Corporation’s (FDIC) Survey of Household Use of Banking and Financial Services. The survey is conducted every two years, so unfortunately the most recent data, from 2019, is pre-COVID (the 2021 survey results should be released in a few weeks). But even then, the FDIC found that among households in general, P2P payment systems — such as PayPal and Zelle — were far more popular than other non-bank transactions — such as money orders and checking services. A whopping 31.1% of households reported using such P2P apps; the next highest product usage, as old-fashioned as it sounds, was money orders, at 11.9%.

As one might predict, the higher a household’s income, the more likely it is to have used a P2P payment service. Nevertheless, these services showed remarkable adoption in communities that traditional banks have had trouble reaching (to put it charitably). For example, 20.2% of Latin American households reported using international money transfer services, such as Western Union, while 24.3% reported using P2P payments. The FDIC also found that 27.7% of black households and 38% of Asian households had used a P2P payment system.

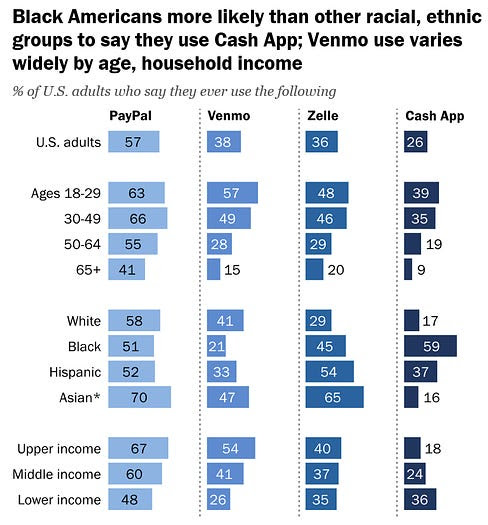

Again, this was all pre-COVID. This week, the Pew Research Center released its own survey on payment apps, based on questions asked in July, with startling results. Although Pew didn’t ask a general question about payment app usage, it found that it was astounding 57% of all US adults say they have used PayPal at least once. Among Americans between the ages of 30 and 49, 66% have used PayPal. Even 48% of lower-income Americans have used PayPal.

What is particularly striking about the Pew survey is that not only have payment apps penetrated minority American communities, but there is significant variation in which groups use which apps. This diagram is informative:

|

One number that really stands out is that 59% of black American adults say they have used the Cash App (which is part of Square/Block), more than three times the percentage of white Americans who have. Part of this reflects the enormous growth that Cash App experienced during the pandemic. People who have followed Square/Block for years may not have gotten used to how thoroughly the Cash App now dominates the company’s business. Starting in the second quarter of 2020—that is, when COVID became a global epidemic and lockdowns made contactless payments more desirable—Cash App revenue began to surpass that of Square’s traditional merchants. Growth has slowed somewhat, but the company still predicts that by 2023, Cash App will generate about $12 billion in revenuewhich is about 2/3 of the total revenue that Block had in all of 2021.

But the relationship between Cash App and Black Americans goes deeper and longer than lockdowns. Back in August 2019, Peter Rudegeair wrote in The Wall Street Journal on the surprising prevalence of Cash App mentions in rap music (see Iggy Azalea in “Kreme”: “Hit me on my Cash App, check it in the morning.”)

Rapper Travis Scott once gave away Cash App gifts to fans who quoted his lyrics on Twitter. IN Journal article, Square co-founder Jack Dorsey said he wasn’t aware of how the Cash App meme took off in hip-hop, though it’s hard to believe Square’s relationship with Jay-Z and TIDAL isn’t a factor. It’s less clear why Asian and Hispanic Americans are so much more likely than average to use Zelle.

However, getting unbanked or underbanked communities to use fintech apps is only part of the equation. One revealing area that Pew explored is the possibility of being scammed through these services; now the stories of fraud at Zelle are legendary. For those who don’t use these apps, especially older Americans, trust is an important reason. Even among those who use the services, a third say they have little or no confidence in the services’ ability to keep their money and data safe (presumably this is an acceptable trade-off for convenience). Also, black and Hispanic app users report being hacked or scammed more often than average.

Of course, the real fear for the underbanked is less that they will be defrauded by outsiders than that the financial services themselves – such as payroll companies, at least until recent crackdowns – are legal frauds. The good news is that the basic services offered by Venmo, Zelle and Cash App are free, reasonably regulated and hugely beneficial to consumers. As these companies strive to become “super apps,” with loans, crypto and buy-now-pay-later services, the risk of being ripped off increases, but for the larger public companies, it’s reasonable to expect regulators to stay on top of this. Whether the ability to make simple P2P payments via a mobile phone will actually change the economic status of underbanked communities remains to be seen. But the bigger question is why so little is written about the enormous success fintech companies have had in reaching tens of millions of Americans who have been excluded from banking for decades.