The story of Pix and what US banks can learn

The US, particularly Silicon Valley, is known globally as a hub for innovation. Some of the biggest companies on earth have been founded here, and the technology created has fundamentally changed our lives. This reputation has perhaps led to a false sense of security regarding our position as a technological superpower. For over 60 years, the United States has led by example; introducing things like credit cards, ATMs and online banking. However, over the past decade, the APAC region has assumed global dominance through payment innovation, with other countries following suit.

Today, over 40 countries offer some form of instant payment, with the US falling behind many of them. Surprisingly, across the instant payments landscape, which represents a new frontier in fintech, no country has achieved the adoption rate of Pix system in Brazil. This system is intended to be three to five years ahead of what US banks have achieved.

Carlos Nettoco-founder and CEO of Materaa provider of instant payment and QR code technology for financial institutions, looks at how Pix has managed to position itself so far ahead.

Some perspective

In 2018, it was Central Bank of Brazil launched an aggressive plan to modernize the economy. Part of this initiative was to mandate that all banks offer instant payments. There was a strong need to provide a digital alternative to cash and outdated payment methods such as Boletosto create an ecosystem that would encourage more competition and provide a payment method that brought measurable benefits to merchants and their customers (who are often underbanked) efficiently.

Credit cards lacked the same appeal they had long had in the US, because merchant fees were high and funds were not available for up to 30 days. As such, many Brazilian merchants refused to take credit or debit payments. In 2019, 77 percent of retail transactions came from cash, which presents a huge opportunity to design a new payment system from scratch. In addition to converting traditional bank customers, a new system will also be able to invite in the nearly 30 percent of consumers who were unbanked.

Introducing Pix

Pix was officially announced in the summer of 2019 and accepted its first transaction on November 16, 2020. With Pix, payment is as easy as asking a consumer for their alias (e.g. phone number/email) or having them scan a QR code . Funds are then instantly transferred from one bank account to another. Money can be moved via Pix between two people, a consumer and a business, between two businesses and even between public entities and consumers.

Merchants and businesses have lower acceptance costs than credit cards because the Pix transaction framework has fewer intermediaries. It’s a clear win for everyone, and the proof is in the numbers.

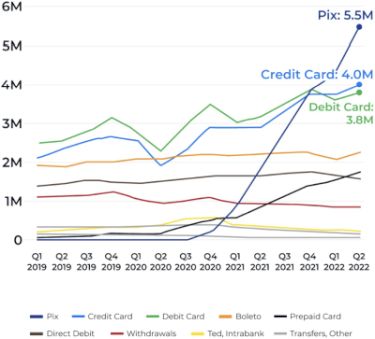

The total number of Pix transactions exceeded debit and credit transactions within one year of launch. Six months later, Pix had served nearly 120 million consumers. Remarkably, 70 percent of Brazil’s adult population had either made or received a Pix transaction, while 60 percent of all businesses used Pix. Today, Pix processes almost three billion transactions every month.

Instant payments in the US

The US has person-to-person payment solutions that appear to be instant, but they don’t move money from bank account to bank account instantly, and they’re nowhere near the scale and scope of Pix. Move money using services such as PayPal, Venmo and Cash App simply involves a general ledger entry that causes one account to go down and the other to go up. Another transaction is required to move from these services to a consumer’s bank account and often takes days to settle.

Cell enhanced that experience by making money instantly available in a consumer’s bank account, but it leverages ACH, debit or wire transfer and settles transactions in batches at the end of the day. “Zelle over RTP‘ creates an immediate end-to-end experience, but is only used in a small percentage of Zelle transactions. Despite success with younger demographics in this limited area, these services remain far below Pix adoption levels, even for person-to-person payments.

Payment rails in the USA

Two instant payment rails exist or are being built in the US, but use is low. Instant payment rail, RTP, which is operated by many of the largest banks in the US, was launched in 2017. Over 300 banks participate in RTP, but the monthly transaction volume is estimated at 15 million compared to 2.9 billion for Pix. FedNow is the second rail but is not operational yet. The launch is planned for mid-2023.

Among the reasons for America’s delay in moving forward with instant and QR code payments is a heavy reliance on credit cards. Unlike Brazil, Americans use cards, just as banks rely on their associated fees. In the second quarter of 2022 alone, Americans opened 233 million new credit accounts, the highest number since 2008 during the last recession, according to Federal Reserve Bank of New York. And the total number of credit cards increased to over 500 million for the first time last year.

But the tide is turning, as global markets have shown. This is also a fact that Jamie Dimonmanaging director i JPMorgan Chase & Co, easily recognized. Just last year, he tasked his corporate and investment bank, CIB, with working with JPMorgan’s consumer and community banking division, CCB, to create a new system that could compete with innovative fintechs and ensure the company’s long-term health. Dimon is not alone as US banks struggle to create the right pay-to-bank solution for instant payments.

What can US banks learn from Pix?

While the market and circumstances surrounding Pix’s incredible adoption are certainly different, there are lessons to be learned. For example:

Pix is an open system. Around 150 banks operate in Brazil, but more than 700 financial institutions participate in Pix. By embracing an integration model, 85 percent of Pix participants have been indirect (eg companies like PayPal), increasing participation while reducing technical burdens and costs. What this could mean for US instant payment adoption is that technology partners and integrations could be their best friends.

All consumers can use Pix. This has been decisive for adoption. More than 130 million Brazilians now use Pix. For around half of these people, it is the first digital payment tool they have ever used. In the United States, there are approximately 5.9 million unbanked adults, but there are an additional 18.7 million households that are considered underbanked. If an instant payment service network was established to meet their needs, it could change the lives of millions of financially disadvantaged people and improve the reputation of financial institutions.

The importance of good user experience

Pix has a great user experience. It is consistent, simple and fast. It is requirements for user interfaces that drive this. For example, the Pix button must be on the first screen of a bank’s mobile app. These are not characteristics typically associated with American banking systems, which often involve multiple steps, transaction delays, and a lot of merchant and consumer frustration. For instant payment offers to be successful, the experience must be exponentially better.

Not only does Pix provide an amazing consumer experience, but it’s also easy for businesses. With standardized API and QR code technology, banks and payment institutions connect seamlessly to POS software or online payment gateways. This makes it easy to switch from one payment provider to another – the API integration is the same. It also encourages competition. Again, it all comes back to ease. With FedNow and RTP there are attempts at standardization. But with two options instead of one, will sellers be forced to choose?

What NOT to do

It is also important to learn what NOT to do. Below are three examples of experiences and how they were dealt with.

- Fraud: In Pix’s early days, consumers were tricked into sending criminal money, and unlocked phones were stolen. Problems were mitigated by education, limits on how much could be sent via Pix, and the ability to claim fraud. Suspicious transactions may also be blocked.

- Error: From time to time money was sent between banks accidentally without recourse. The central bank created legislation that mandated a bank to return the money when requested by a bank that had made a mistake.

- POS solution vendors (eg NCR) were slow to integrate. In the beginning, some merchants did not know how to confirm payment from a QR code due to lack of integration. This created confusion, and in some cases fraud. Sellers learned that confirmation was essential to receiving payment.

Financial institutions in the US have been allowed to rest on their laurels and outdated systems for far too long. Nimble fintechs are coming, armed with knowledge from other international markets. As such, it is time for banks to “innovate or die” so to speak. They are not immune to interference, and the next move is theirs. Will they seize the opportunity?