2 trends to be seen in the investment scene for start-up of agri-fintech investments of 1.6 billion dollars

Niall Haughey is a co-founder of Graze, an agri-fintech studio dedicated to developing digital financial services for the food and agriculture sectors. He began writing the Agri Fintech newsletter in 2021 to highlight innovative projects globally and share stories from entrepreneurs. Prior to this, Haughey was a consultant for the financial industry in London, established and operated a payment business in the United Kingdom and Ireland, and worked throughout Africa to develop agricultural financing products for inputs, grain stocks receipts and equipment.

Haughey recently released a new report that revealed $ 1.6 billion in investments in agri-fintech startups in 2021 across 93 contracts, representing a 138% year-on-year growth in contract activity. Here he digs into two more trends from the research.

My recent report Agri Fintech in Numbers brought me two remarkable trends.

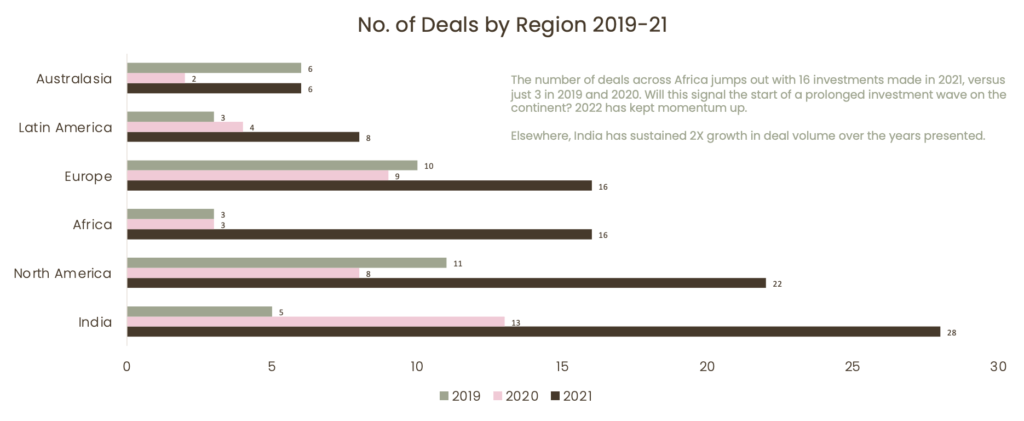

Investment in Europe by contractual activity and the dollar appears to be quite low, especially when you consider the total amount invested in fintech in the region. And just south, investing in African agri fintech models has become feverish, with a belated recognition that agriculture, technology and finance play a mutually beneficial role in solving some of the market’s challenges.

European investment is low, is there an opportunity?

European Agri Fintech raised $ 124 million in 2021, only 8% of the total funds raised in the data collected. This number actually shrinks when you remove Wefarm ($ 11 million) and Pula ($ 6 million) which operate in sub-Saharan Africa but are based in the UK and Switzerland respectively. However, European fintech raised about $ 30 billion, or 23% of the global total of $ 131 billion. Is it possible that agri fintech in Europe will not be a “thing”?

Let us first consider where the general fintech investment has gone in Europe. Neobanks has been a popular recipient of funds with N26 ($ 900 million), Monzo ($ 500 million) and Revolut ($ 800 million) raising astronomical investments. Klarna raised $ 1.6 billion over two rounds to run Buy Now Pay Later (BNPL), another popular topic.

I do not expect a similar increase in investment in agricultural neobanks, but Oxbury Bank is one example in the food and agriculture sector that has raised $ 21 million in 2021, offering a banking model in UK markets and a technology proposal in others – it is very neobank. Tarfin, which can be classified as a new lender, also raised a $ 8 million Series A to expand its credit footprint, with a recent expansion to Romania, one of the countries with the largest funding gap in agricultural finance, according to Fi-Compass, a European research platform .

In terms of BNPL, Agro.Club has taken an opportunistic approach by already launching financial products in several markets, including the US, Spain and currently has an appetite for launching in Brazil, according to this AFN article. I think the agricultural version of ‘BNPL’ will be ‘Buy now, pay seasonally’, with changed repayment terms beyond the typical three to four months that Klarna offers, for example, so this will be interesting to see.

Prioritization as opposed to underperformance

There have been a few bright lights. HeavyFinance looks like a real fintech-first company that sees an opportunity for equipment financing across Europe. It is easy to seize the opportunity of € 12.5 billion that Fi-Compass cites to fill financing needs and is actively launched in markets such as Poland or Portugal where economic gaps are acute. The management team in HeavyFinance enjoys momentum and has not ruled out entering markets such as Germany or France if the right opportunities arise.

In the same way, companies such as Stable and Concept Dairy in Europe offer opportunities for tailor-made risk management products. Personally, the innovation captured in this type of offer is more important than raising big rounds – although Stable did too, and raised credible $ 46.5 million Series A and $ 60 million Series B recently!

An African boom

African investment has had a resounding period. There have been 16 agreements in 2021, as many as in Europe, with total funds totaling $ 75 million from just $ 10 million. This year has refused to slow down with Apollo Agriculture also raising a $ 40 million Serie B bumper in March.

This flourishing of activity is welcome for two reasons. First, the emergence of these Agritech platforms has highlighted the opportunities available to investors willing to solve value chain problems in sub-Saharan markets. Second, this script changes from donor-related investments that have been the only willing investor in this sector for too long.

But what about the African outsiders?

In 2021 and recently in 2022, two major rounds have been completed by Twiga Foods and Apollo Agriculture. Will these set the standard for venture rounds on the continent ?. I feel that there is still a lot of work to be done to justify these figures, but it is not to criticize any of the companies, which of course already know this.

First, and ignoring the valuation, funds raised are on a par with other companies such as ProducePay ($ 43m) or Bushel in the United States ($ 47m). ProducePay targets the fresh produce market – it has “800 customers and has financed the production of more than $ 3 billion in fresh produce”. This is a large market, and it has already raised institutional debt of $ 200 million for financing lines. Similarly, Bushel offers a product in the giant North American grain market and aims to develop financial functionality around it.

Twiga raised funds to go upstream for integrated production, and last week announced a $ 10 million investment, including equity and debt, in commercial agriculture. This is a reminder to operators and investors that work with small producers is very difficult to scale. Twiga also wants to expand to five other markets such as Nigeria and Ghana, to expand its B2B offering and perhaps commercial farming is one means of securing supply in a platform market that becomes competitive.

Apollo Agriculture is a separate example. It has a tightly integrated platform that works with input retailers to provide credit to manufacturers, and has cited product financing as the key to achieving a 10-fold increase in sales. The offer is more unique, and it will be interesting to note the expansion plans when they are revealed – will it be across Africa or will they venture further afield?

Both examples are classic examples of embedded finance agritech style: markets, loans, intelligence, all wrapped up in one. I hope the ecosystem secures more investment in the market pull platforms offered by Vendease (targeted at restaurants) or AFEX, which targets processors, and also in the transaction infrastructure such as Nile.ag which streamlines paperwork.

By the way, it was also where the fintech investment on the continent went – infrastructure – with reportedly over $ 3 billion in VC investments that went to build the rails for future trade around payments, cross-border money transfers and lending solutions.

Briefly summarized; developed countries seek niches and work around existing infrastructure and value chains. While in developing countries, there is still everything to play for.